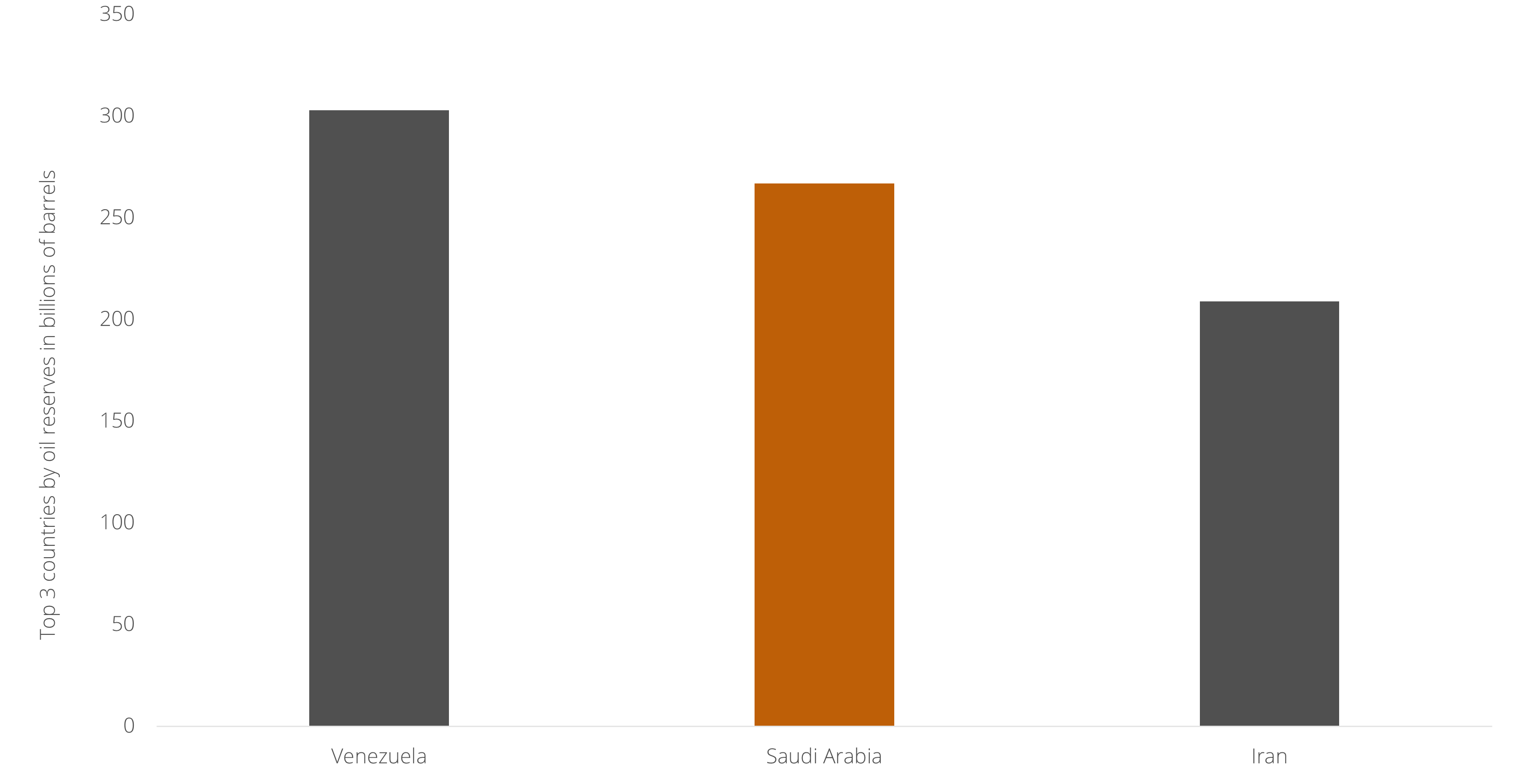

At the start of 2026, just as the United States’ confrontation with other countries threatens global stability, its withdrawal from other regions is also fueling conflict, particularly in the Middle East. The region’s dynamics have shifted fundamentally in the past few years: as the United States retreats, the most powerful country in the region, Iran, has been weakened by its war with Israel following the Hamas attack of October 7, 2023. The result is an open contest for control of the region among five countries: Israel, Turkey, Saudi Arabia, the United Arab Emirates, and Qatar. In April 2025, Israel bombed designated sites for three Turkish military bases in Syria, while Saudi Arabia and the United Arab Emirates - until recently longstanding allies - have engaged in proxy conflicts in Yemen, Sudan, Libya, and Somaliland. Looking ahead, it is Saudi Arabia that appears most at risk of triggering a destabilizing scenario, as its future is increasingly threatened by shifting dynamics in the global oil market on which it so heavily depends, driven by rising US production and the prospect of Venezuela, and possibly Iran, regaining access to global oil markets.

As the Western world awaits United States President Trump’s speech in Davos amid an escalating conflict between the US and Europe over the status of Greenland, the prime minister of Canada has returned from China after announcing a “new world order” in which Canada will deepen its relationship with Beijing. This Canadian vision is part of a broader shift across the West: in 2025, Spain joined Hungary in welcoming Chinese producers of batteries and electric vehicles to the European continent, and in the coming weeks the leaders of both the United Kingdom and Germany will visit China in what will likely crystallize into a shared narrative.

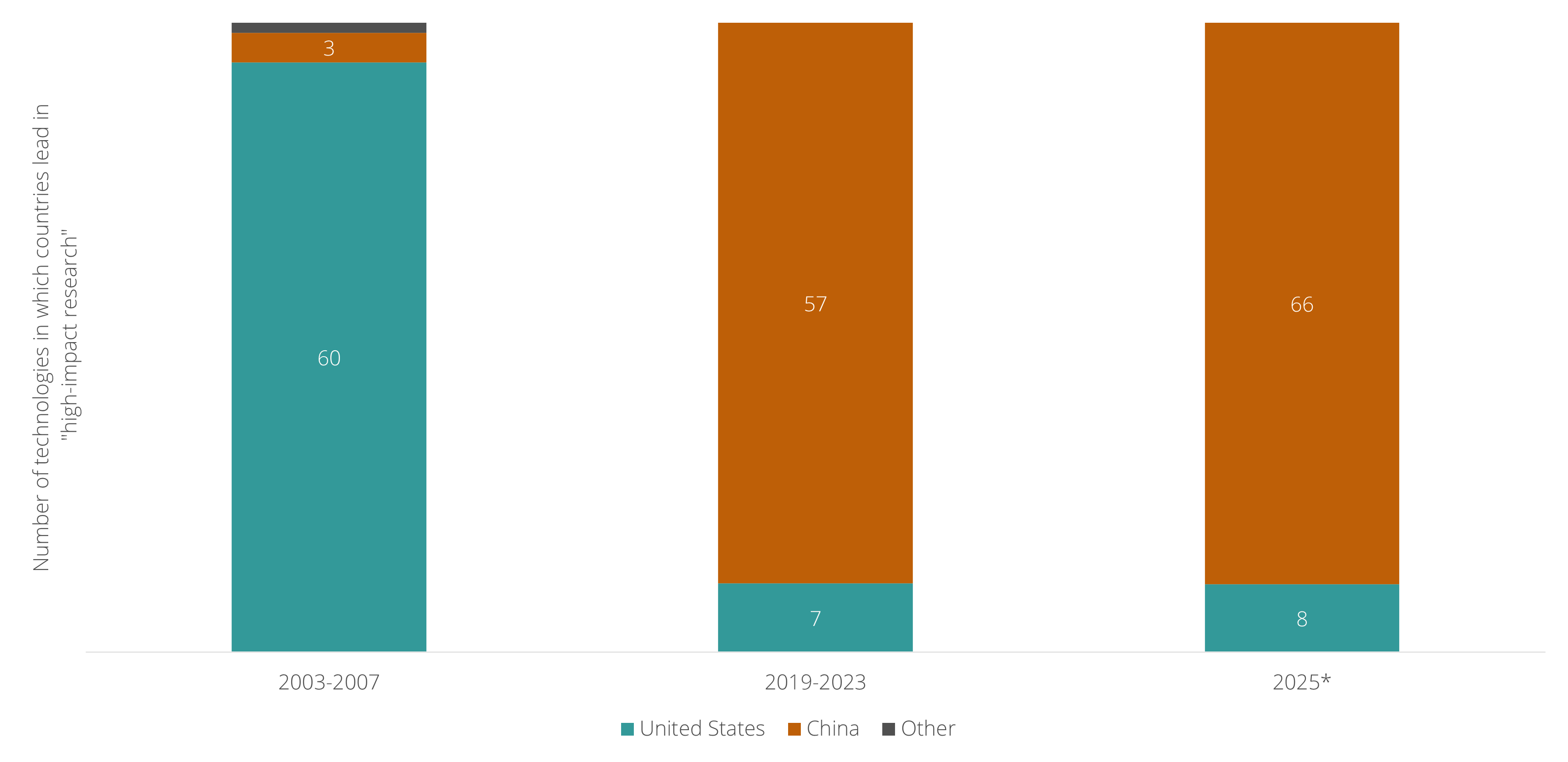

As China is increasingly seen as a more reliable partner than the United States by many nations, it is also overtaking the US in technological innovation. In the latest update of the Australian Strategic Policy Institute’s (ASPI) tracker of 74 “critical technologies,” the US leads in just 8, while China leads in 66. Notably, China has recently surpassed the US in the global share of downloads for open-source artificial intelligence models, which are released for free and can run on local cloud providers rather than US- or China-based ones. China’s growing lead in AI is underpinned by its massive advantage in electricity generation: by 2030, its surplus power is projected to be three times larger than the entire world’s electricity demand for data centers. This is also giving rise to entire industries that remain largely unknown in the Western world, such as the “low-altitude economy” (Chinese food-delivery firm Meituan has completed more than 600,000 orders via drones in China).

In 2026, this global shift could shock US financial markets, much as the launch of an AI model by the Chinese firm DeepSeek triggered a panic in January 2025.

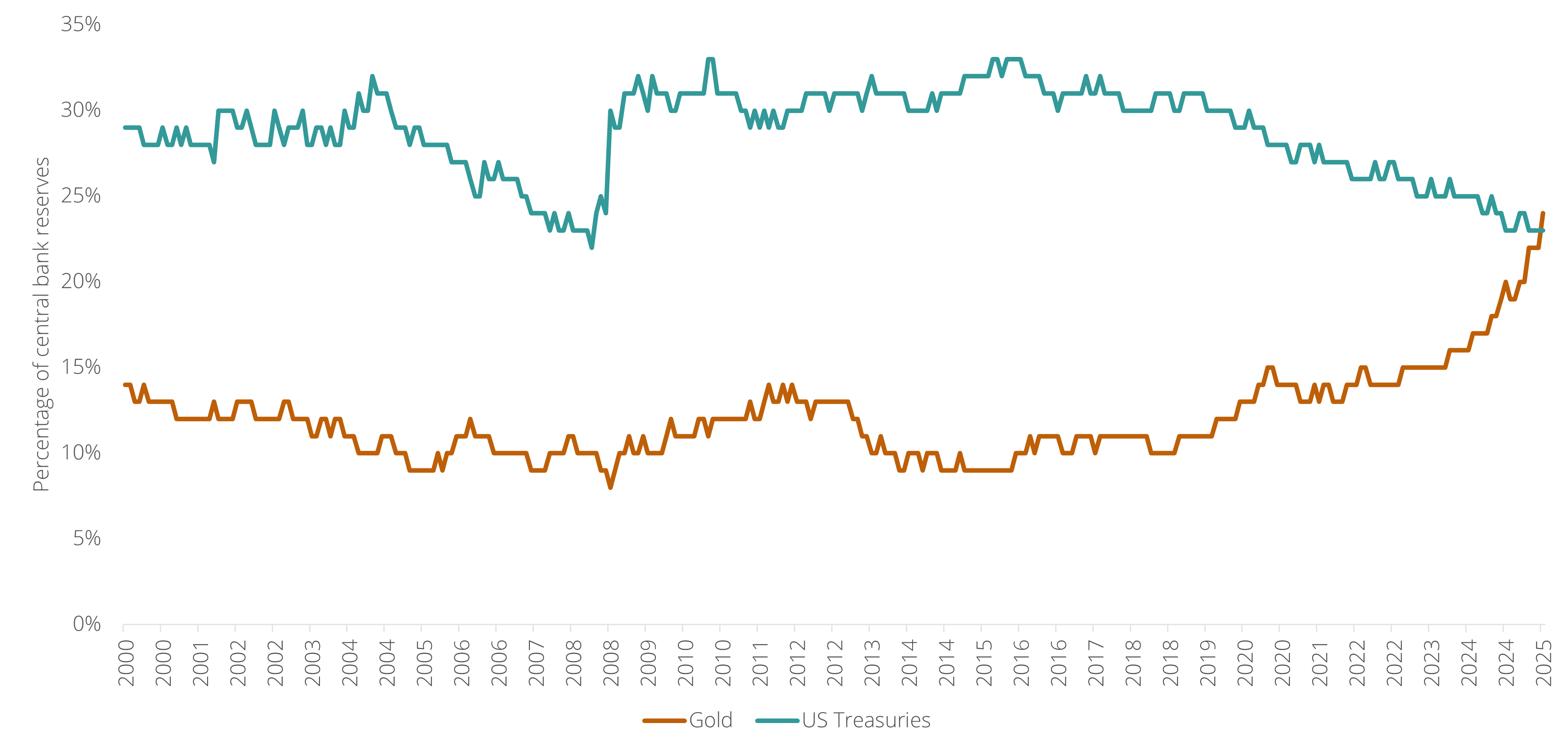

What is currently being underestimated is the likelihood that US president Trump, after several high-risk strategic successes (Iran, Venezuela), overplays his hand and makes a mistake similar to Putin’s invasion of Ukraine, which was intended as a quick operation but has turned into a four-year war. If the US were to force Denmark to relinquish control of Greenland, this could become the catalyst for what Europe is currently trying to talk into existence: a new European defense architecture that would effectively replace NATO. If the US were to target Canada, most likely by supporting a secessionist movement in provinces such as Alberta or Quebec, this could spark a nationalist movement to defend Canada, similar to Ukraine’s response to Russian aggression. Besides this, in both scenarios, pressure on the US dollar could intensify, as many Western investors would be incentivized to reduce their dollar holdings. Since 2020, the US dollar has already experienced declining exposure among central banks. If this trend were to accelerate, it could destabilize the US economy through upward pressure on interest rates.