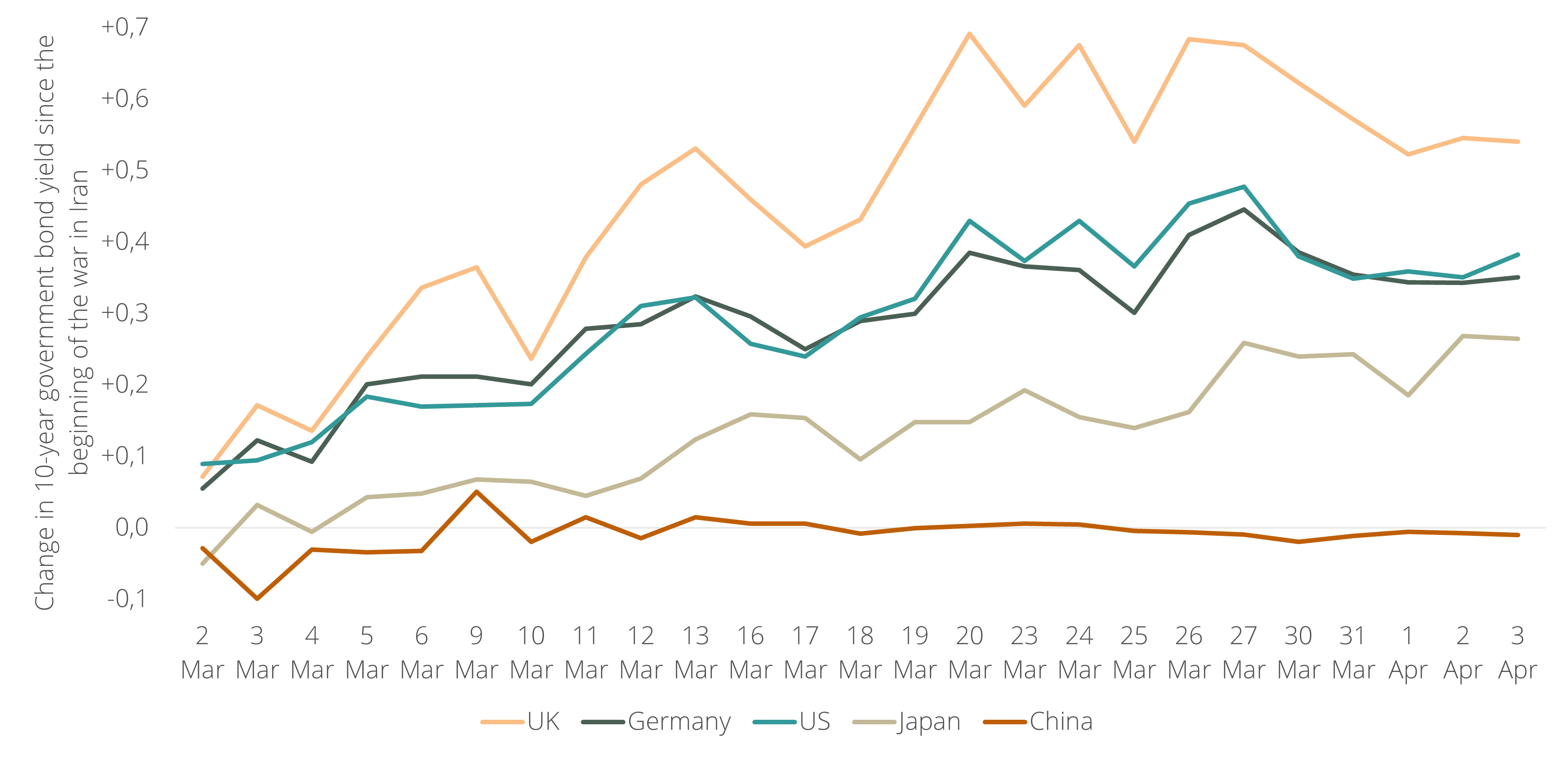

In every global crisis of our generation — the 2001 dot-com crash, the 2008 financial crisis, the 2020 COVID crisis — global investors sought safety in US Treasuries, placing capital in the 10-year US government bond. The 2026 war in Iran has broken that pattern. For the first time in a global crisis, China's government bonds are the only safe haven, holding their value while US Treasuries, other government bonds, and even gold have sold off. Meanwhile, equity markets in China have also lost less value than their counterparts in the US, Europe and Japan.

This is happening despite investors' well-documented reservations about Chinese assets — political risk, capital controls, and the difficulty of converting renminbi into dollars, euros, or yen. That is because, as we have written in the past year, China's safe haven status is part of a larger shift: trust in US stability is declining, while China is no longer seen as uninvestable, leads in technological innovation, sets global standards, has soft power and is better prepared for an era of prolonged global conflict.

Ironically, while the US is locked in a global struggle for influence with China, it is China that was better prepared for the war in Iran — the war the US itself started. China's energy system is more resilient against a prolonged conflict in the Middle East, its businesses are the main beneficiaries of the conflict, and the conflict is improving China's reputation as a more stable international partner for trade and investment than the US.

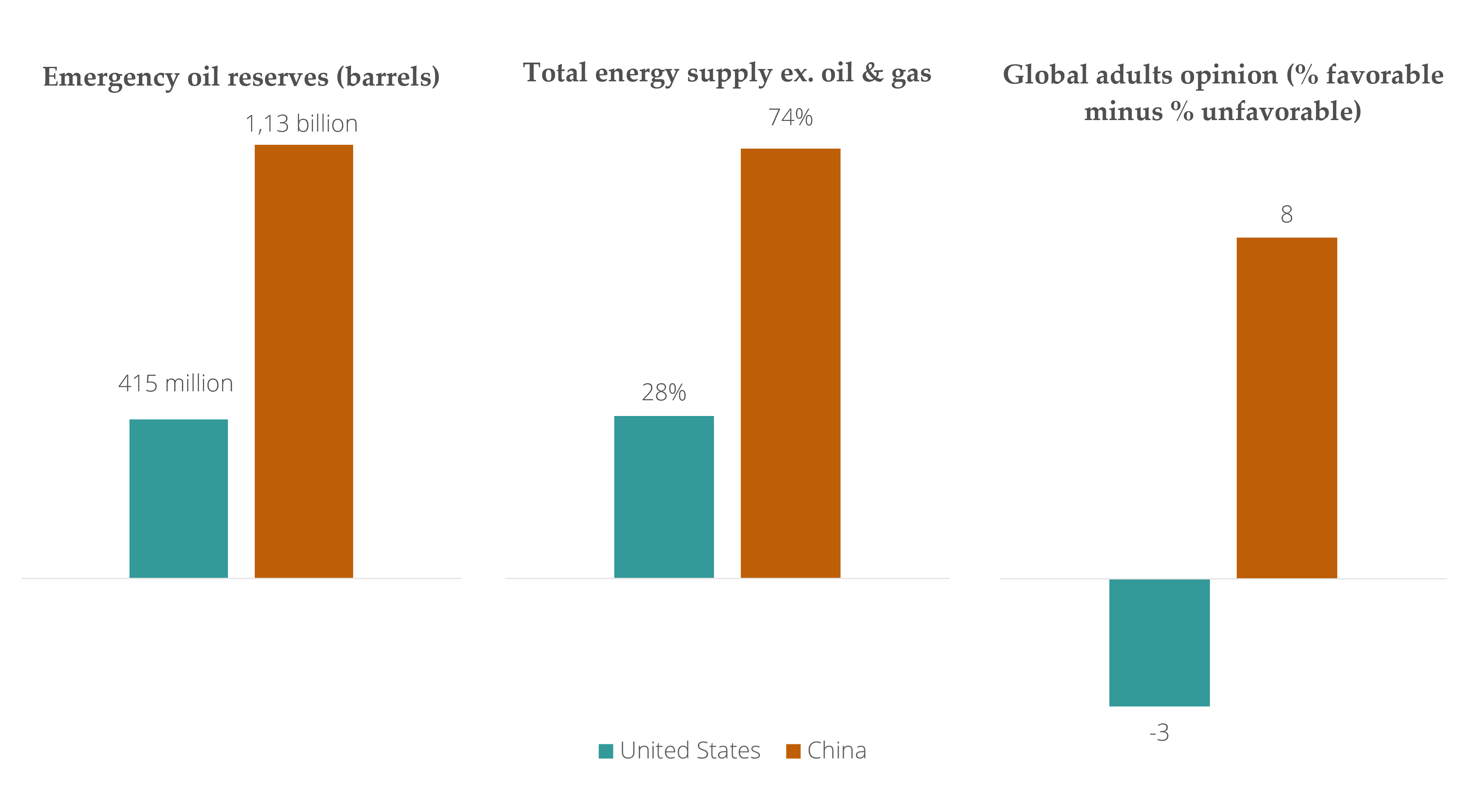

First, China's economy is more resilient to a prolonged conflict in the Middle East than any other major economy. The main reason is the structure of its energy system. As we wrote several weeks ago, China's vision of energy security — a mix of nuclear and renewables, with coal serving as a bridge — is more resilient than the US system, in which oil and gas account for 72% of total energy supply. China also reportedly holds twice as many emergency oil reserves: 1.13 billion barrels compared to 415 million for the US.

Second, China's businesses are the leading producers of the technologies that benefit most from this conflict. In many countries, yet another international conflict driving up oil and gas prices has sparked renewed demand for renewable energy technologies such as solar panels, heat pumps, and batteries — all industries in which China is the world leader. Electric vehicles, another area of Chinese dominance, are also gaining in popularity as a result.

Third, under the second Trump administration, China is rapidly becoming a more stable and predictable international partner than the US. European leaders were already working to improve relations with Beijing before this conflict began. Global investors, meanwhile, are increasingly viewing Chinese government bonds as a relatively stable safe haven. Notably, Iran is reportedly demanding payment in Chinese renminbi from ships seeking passage through the Strait of Hormuz.

Most importantly, even if the US manages to prevent a full economic collapse in the coming weeks — as we warned last week remains a real risk — the dynamic described above is unlikely to reverse. In all three dimensions, this conflict is likely to remain a positive force for China's long-term development.

The US president just announced a 5-day halt to strikes on Iran’s energy infrastructure. This most likely signals that Washington recognizes what further escalation of this conflict would cost. Everything now depends on the US finding a solution in just a few weeks – one that almost certainly means leaving the Iranian regime intact, despite regime change having been an explicit American objective from the start. It is urgent because the global economic pain is already materializing in at least three distinct but interconnected layers.

1. Energy, inflation and debt

Higher energy prices feed directly into inflation expectations – and therefore into the interest rates set by central banks and demanded by fixed-income investors. Recently, these higher interest rates have already exposed deep liquidity stress in private markets, which threatens to spill over into institutions who hold these assets – like pension funds. This alone could be a sufficient reason for the US to find a way to stop the conflict.

2. The AI boom's hidden supply chain

Less visible but equally significant is the threat to the inputs that power the artificial intelligence boom. Data centers and the computer chips that run them depend not only on cheap energy, but also on a set of industrial chemicals (like helium, sulphur and bromine) that are mainly sourced from the Middle East and are now caught in a disrupted supply chain. Since it was the AI boom that drove the majority of US stock market growth over the past three years, a sustained conflict puts that growth engine under direct threat.

3. The wealth effect and the American economy

The third layer is the large share of US consumer spending – the largest single driver of the US economy – that comes from high-income Americans, whose consumption is tied to the value of their investment portfolios. A sustained stock market decline, amplified by Gulf sovereign wealth funds pulling capital from US markets, could trigger a meaningful pullback in that spending, which could throw the American economy into a vicious downward spiral.

A narrow window for diplomacy

The current situation is straightforward: three simultaneous shocks – to energy prices, to critical technology supply chains, and to the wealth effect underpinning US consumption – arriving together would strain the global economy in ways that no single policy can easily offset. Without a genuine diplomatic breakthrough in the coming weeks, the world could be facing an economic crisis that rivals anything seen in a generation.