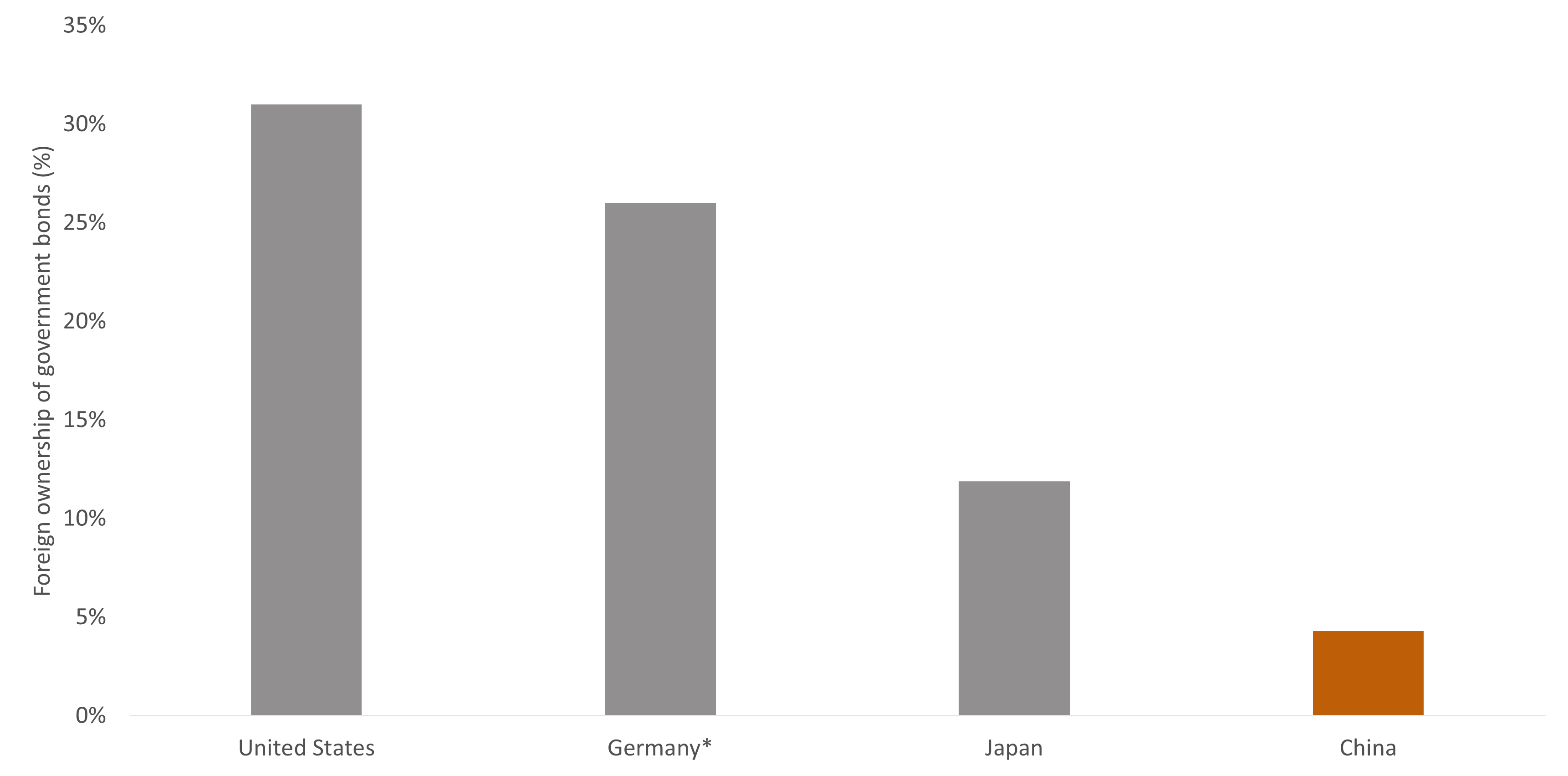

In recent weeks, China announced several significant steps to address the barriers that hold back adoption of the renminbi by global investors.

1. Chinese government bonds can now be quickly converted into cash - making them far more attractive to hold. Through a new repo facility, foreign investors will be able to use their Chinese government bond holdings as collateral to borrow short-term renminbi cash. This mirrors the US Federal Reserve’s repo facility, which lets foreign central banks swap US government bonds for dollars. Previously, Chinese government bonds were difficult to liquidate quickly, making them relatively unattractive to hold for global investors who need to be able to move in and out of positions.

2. Global investors can now protect themselves against losses on Chinese bond holdings - removing a key barrier to owning them. A new Hong Kong-based futures market for Chinese government bonds will allow global investors to hedge interest rate risk in their Chinese bond holdings without needing mainland China market access. The absence of such a hedging mechanism was a key reason for underweighting Chinese bonds in global investment portfolios.

3. More support for two-way capital flows - a necessary step in making the renminbi a currency global investors can comfortably hold. China has increased the quotas under its Qualified Domestic Institutional Investor program, allowing more Chinese capital to flow into foreign markets. Enabling outward capital flows is a classic step in the internationalization of a domestic currency because it creates a two-way market and reduces the perception of a one-way trap.

4. More support for the offshore renminbi, which is freely traded outside China - making it easier for global investors to transact in the currency. Six major state-owned banks have been authorized to conduct transactions in offshore renminbi - a currency market distinct from the onshore renminbi, freely traded in financial centers such as Hong Kong and Singapore - directly from the mainland. Previously, such transactions had to be routed through these offshore hubs. This is likely to increase the pool of freely traded renminbi in global markets.

Analysis of the internationalization of the renminbi should go further than reflecting on “de-dollarization” - although foreign demand for US dollars could indeed decline as the renminbi becomes a more credible alternative. More importantly, the internationalization of the renminbi is likely to begin in Asia, where central banks and sovereign wealth funds have the most to gain from diversifying into renminbi assets, something Chinese government statements in recent years have made explicit. The infrastructure to support that vision is now being put in place, and global investors would be unwise to ignore it.