Over the past year, we have followed two contrarian China trends. In recent weeks, both have been confirmed.

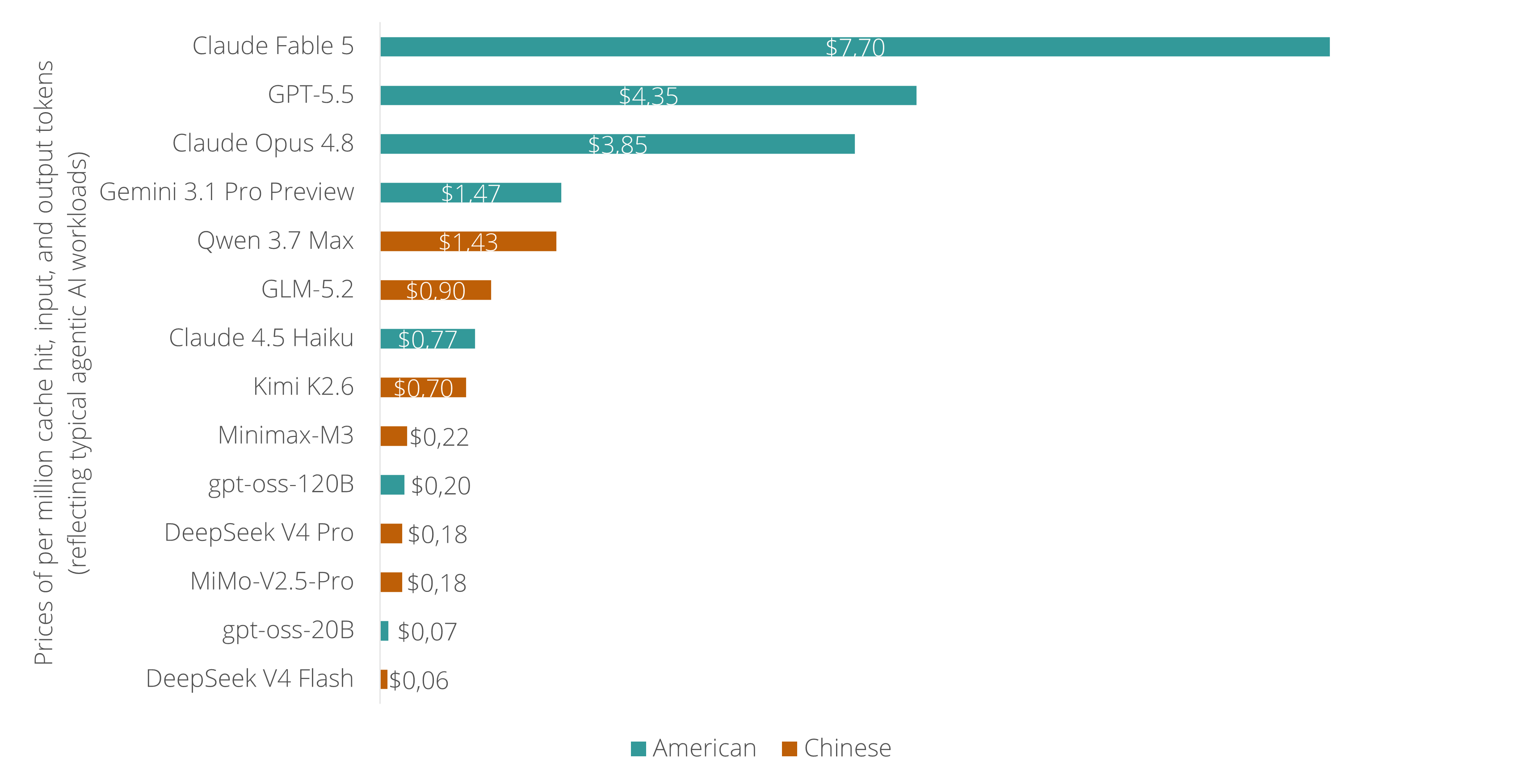

First: Chinese AI has reached the frontier at a fraction of the cost. We argued this in "In 2026, China Leads the United States in Both International Relations and Technological Innovation", "China Is Winning in Innovation Where It Counts: Markets, Not Just Research", and "China Has Closed the Gap With the United States in Artificial Intelligence". The evidence has now caught up: Apollo shows Chinese open-weight models trail the US frontier by just four months, while Moonshot's Kimi K3 recently outranked Anthropic's Opus 4.8 in blind testing. American developers are switching en masse to cheaper Chinese models like DeepSeek. This matters for investors because the AI boom is built on the assumption that US labs could charge premium prices and has driven significant US stock market gains in recent years.

Second: global opinion of China, in particular among young people, is improving, especially relative to the US. We wrote this in "China Already Has More Soft Power Than the Soviet Union Ever Did" and "A Majority of Singaporeans Now Prefer China to the US". This month, Pew confirmed it. Across 37 countries, 51% of the people have a favorable view of China, while 39% have an unfavorable view. Crucially, younger people in most countries have more favorable views of China than older people.

The conflict between Saudi Arabia and the UAE is showing new signs of escalating. If current trends continue, this could raise question marks around the $3 trillion managed by the sovereign wealth funds of both countries — much of which flows to western markets.

In January 2026, a month before the war between the US and Iran broke out, we warned that the conflict between Saudi Arabia and the UAE was likely to escalate during this year. As soon as the war began, we warned that it was likely to threaten the safe haven status of the Gulf states, as a significant amount of capital was likely to leave the region permanently. A few weeks later, we reaffirmed that the risk of a financial crisis in the Gulf was growing, as the UAE requested a currency swap line with the Fed. Next, the UAE took the extraordinary step of leaving the OPEC oil cartel, as it can afford a much lower oil price than OPEC leader Saudi Arabia. In recent weeks, new signs of stress have emerged, as Saudi Arabia has reportedly blocked financial flows to the UAE.

Looking ahead, a relevant analogy is the conflict between Qatar and Saudi Arabia (backed by the UAE), which led to a blockade of Qatar in 2017. It severely depressed foreign direct investment into the country for years — and a similar, but far larger, financial shock could follow if the conflict between Saudi Arabia and the UAE continues to escalate.

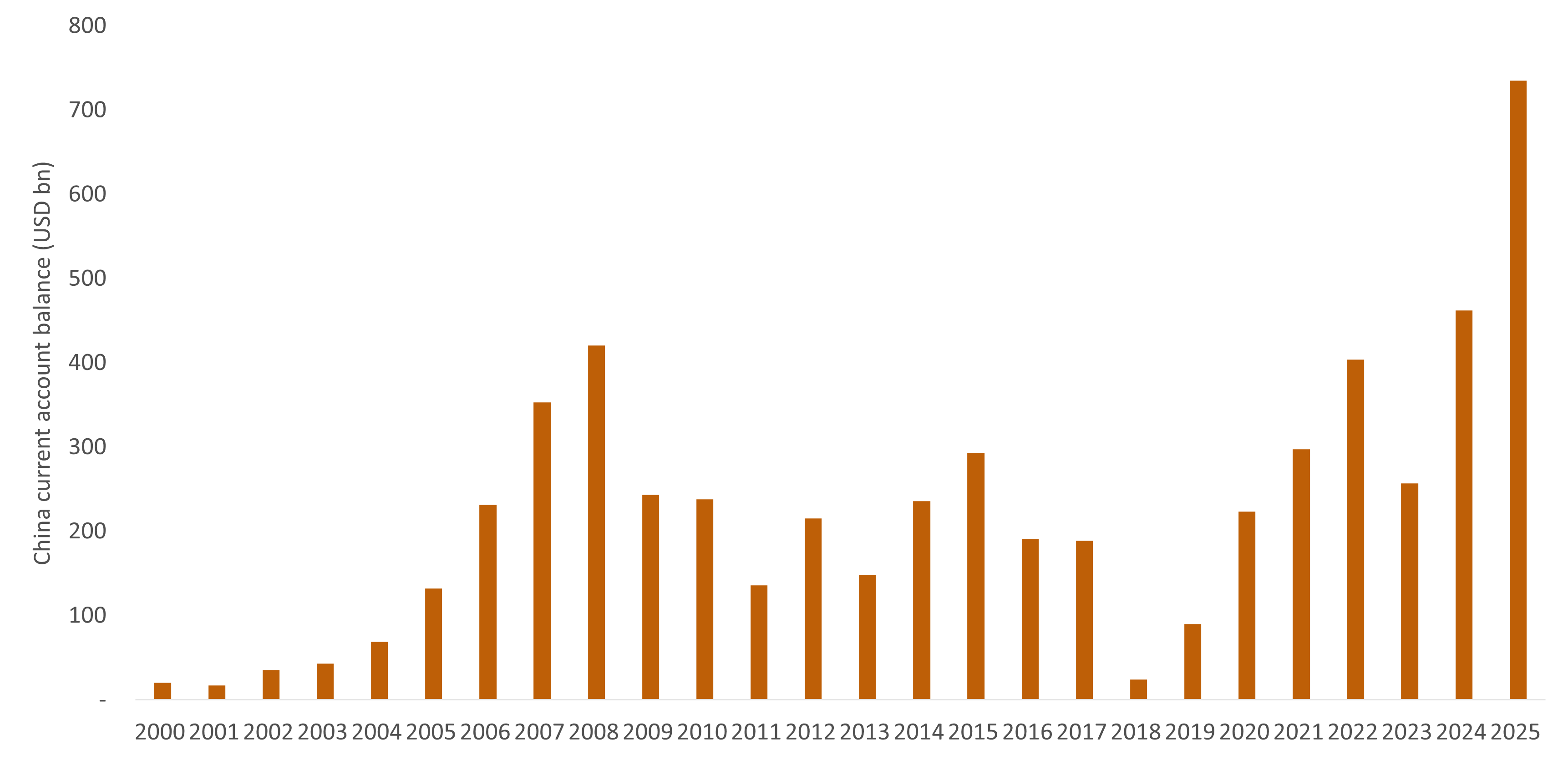

In 2025, China recorded the largest merchandise trade surplus in history – roughly $1.1 trillion more in exports than imports – based on Chinese manufacturers' global competitiveness. The alarm this has provoked in the United States and Europe over the fate of their own industries has dominated the debate. Far less attention has gone to another question: where is all this Chinese capital going? A trade surplus does not simply disappear. Every dollar China earns abroad and does not spend on imports must be reinvested abroad – the question is through which channel.

For two decades from the early 2000s, much of China's surplus was recycled into US Treasuries. But that has changed: Chinese capital no longer flows automatically to the US. The largest destination for China's capital in recent years has been Hong Kong – though much of it flows through the territory rather than settling there, using Hong Kong as a conduit to other foreign markets.

In the years ahead, more countries are likely to compete for access to Chinese capital rather than resist it. At the European level, this almost happened in December 2020 when the EU and China concluded the Comprehensive Agreement on Investment, which would have opened a return channel for Chinese surplus capital into Europe – including partnerships that would have shored up Europe's industrial competitiveness through a new energy system with lower energy costs. The deal was shelved at the last moment, but the logic that produced it has not gone away: Spain and Hungary are already building long-term national strategies that position Chinese capital as a funding engine for European reindustrialization, and others are likely to follow.

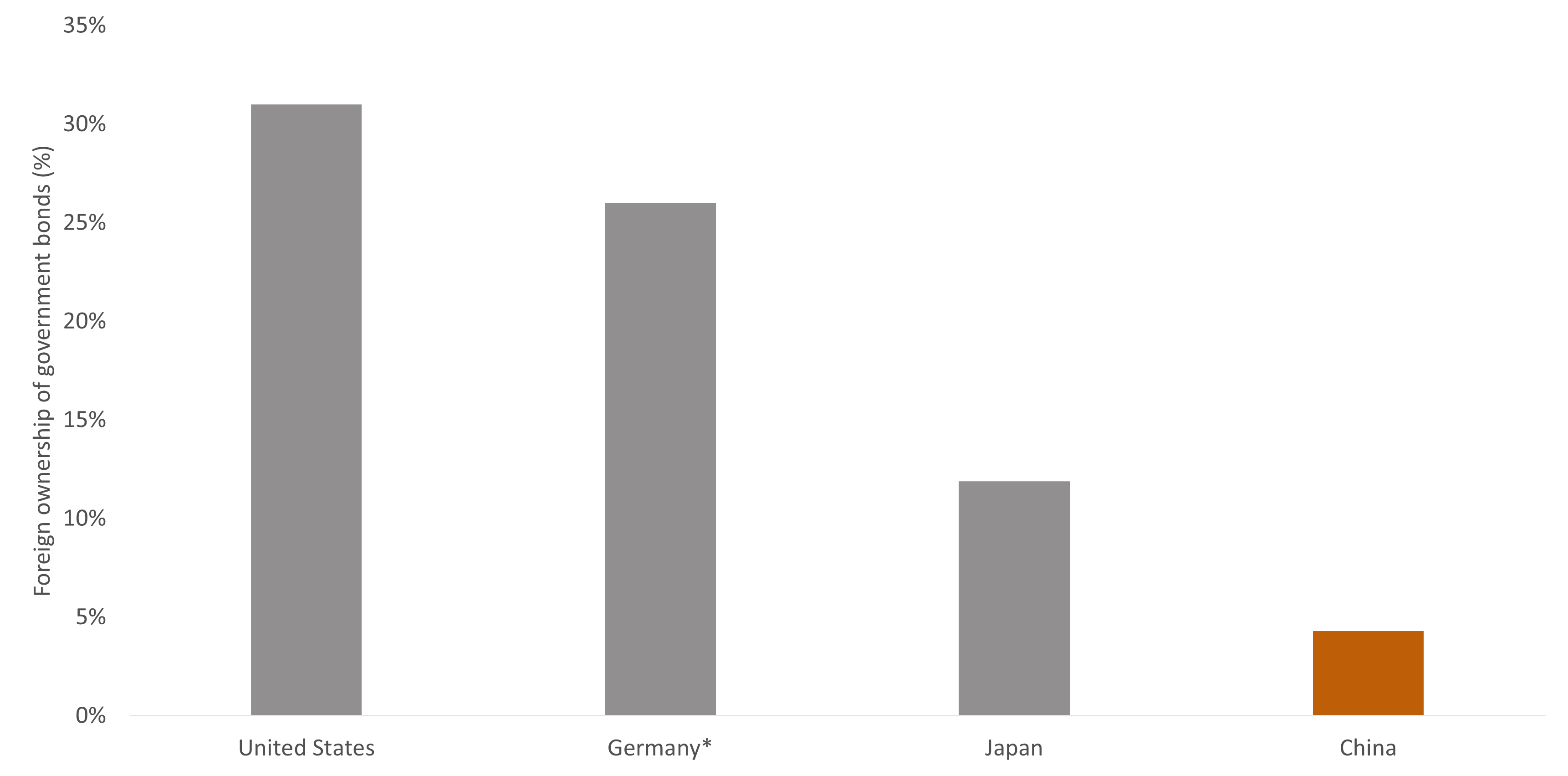

In recent weeks, China announced several significant steps to address the barriers that hold back adoption of the renminbi by global investors.

1. Chinese government bonds can now be quickly converted into cash - making them far more attractive to hold. Through a new repo facility, foreign investors will be able to use their Chinese government bond holdings as collateral to borrow short-term renminbi cash. This mirrors the US Federal Reserve’s repo facility, which lets foreign central banks swap US government bonds for dollars. Previously, Chinese government bonds were difficult to liquidate quickly, making them relatively unattractive to hold for global investors who need to be able to move in and out of positions.

2. Global investors can now protect themselves against losses on Chinese bond holdings - removing a key barrier to owning them. A new Hong Kong-based futures market for Chinese government bonds will allow global investors to hedge interest rate risk in their Chinese bond holdings without needing mainland China market access. The absence of such a hedging mechanism was a key reason for underweighting Chinese bonds in global investment portfolios.

3. More support for two-way capital flows - a necessary step in making the renminbi a currency global investors can comfortably hold. China has increased the quotas under its Qualified Domestic Institutional Investor program, allowing more Chinese capital to flow into foreign markets. Enabling outward capital flows is a classic step in the internationalization of a domestic currency because it creates a two-way market and reduces the perception of a one-way trap.

4. More support for the offshore renminbi, which is freely traded outside China - making it easier for global investors to transact in the currency. Six major state-owned banks have been authorized to conduct transactions in offshore renminbi - a currency market distinct from the onshore renminbi, freely traded in financial centers such as Hong Kong and Singapore - directly from the mainland. Previously, such transactions had to be routed through these offshore hubs. This is likely to increase the pool of freely traded renminbi in global markets.

Analysis of the internationalization of the renminbi should go further than reflecting on “de-dollarization” - although foreign demand for US dollars could indeed decline as the renminbi becomes a more credible alternative. More importantly, the internationalization of the renminbi is likely to begin in Asia, where central banks and sovereign wealth funds have the most to gain from diversifying into renminbi assets, something Chinese government statements in recent years have made explicit. The infrastructure to support that vision is now being put in place, and global investors would be unwise to ignore it.

One way in which the 2026 war in Iran will be remembered – if the situation does not escalate further – is that the largest oil supply disruption in history triggered a far smaller oil crisis than expected. A key reason, besides the US withdrawing from the conflict without achieving its objectives, is China's oil reserves. When the war broke out, China stopped importing oil and began drawing on those reserves, which relieved pressure on global oil markets. This matters because it demonstrates that stockpiling and diversification of key commodities – a topic that has received intense attention since COVID – can be very effective.

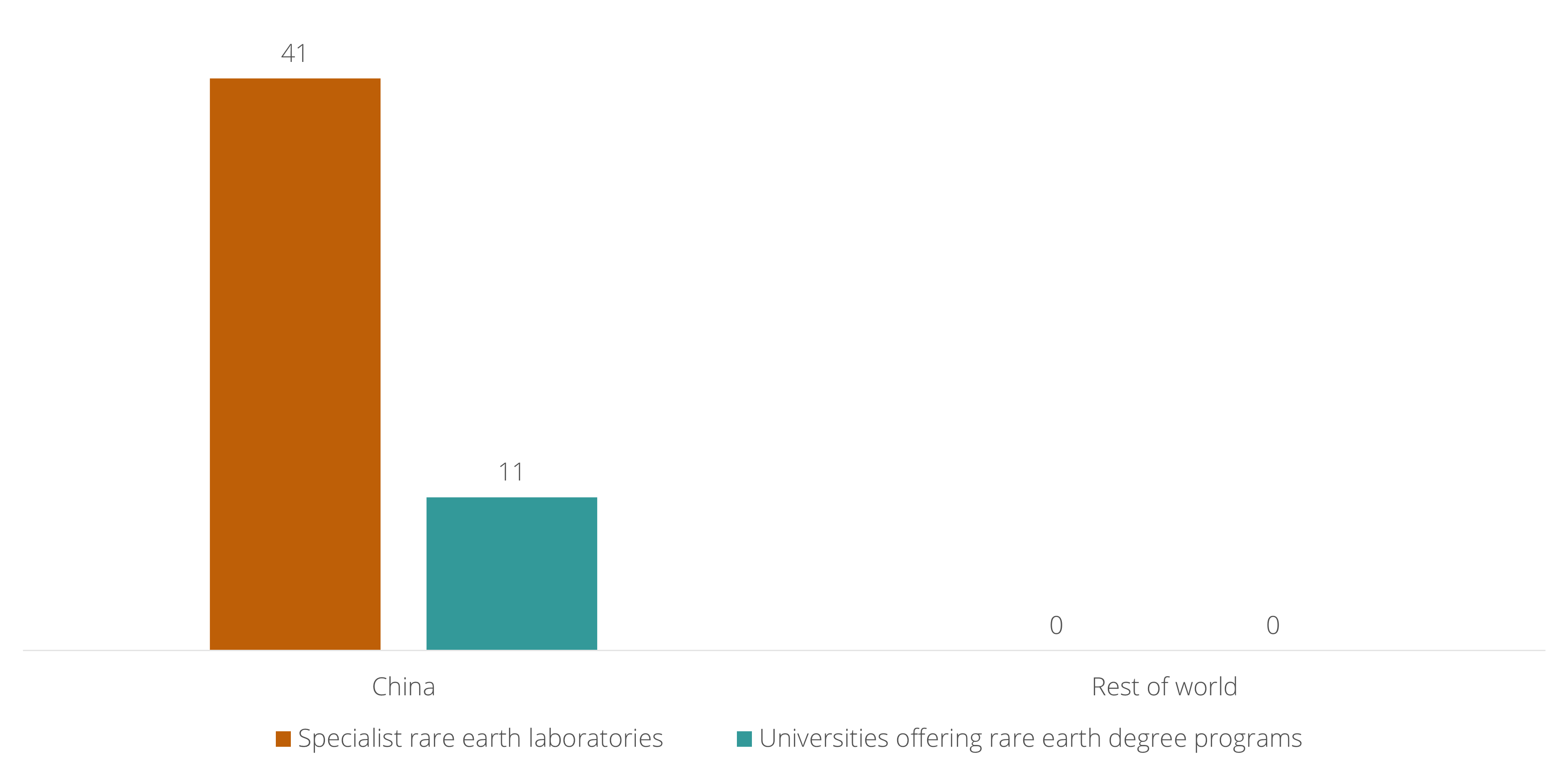

The EU has identified diversification of key commodities as a political goal, just like the US and China, but compared to them has the longest way to go. For its energy needs, Europe has infamously traded its dependency on Russian gas for a dependency on American liquefied natural gas – which is also more expensive, a cost that continues to weigh on European industry’s “existential” situation. This shows that the war in Ukraine did not produce any serious diversification in European energy supply. For its metals needs, the challenge is greater still. Last week, the G7 announced a 60% target to cap dependency on rare earth imports from any single source – meaning China, which holds a market share of up to 99% in some metals. But how the mining and processing of these materials will scale up, short of major investment projects spanning multiple decades, remains the central question. It is telling that Reuters recently reported on China's vast ecosystem of rare earth laboratories and university programs – and could not identify a single comparable education program outside China.

This week, Kevin Warsh begins his term as the US central bank's new chair. He was chosen by Trump for his belief in AI as a driver of lowering costs across the economy, which would open the possibility of cutting the short-term interest rate. However, there are several reasons why US interest rates – both short-term (set by the central bank, which raises them when inflation is too high) and long-term (set by the bond market, which raises them when inflation expectations are elevated or too much debt is being issued) – are likely to remain high and may go even higher.

First, there has been a global regime change in the past five years: interest rates have stopped declining for the first time in decades. There are several structural reasons for this – from massive government spending to international conflicts, all of which raise inflation and consequently interest rates – and such structural changes are unlikely to reverse without a clear cause, such as a meaningful reduction in debt or a resolution of major conflicts, neither of which seems likely anytime soon.

Second, the global shift towards higher interest rates is generating new mechanisms that reinforce the trend. Japan, for instance, may increasingly sell US assets to protect the value of its currency. If Japanese investors were to sell US government bonds at sufficient scale, it would add further upward pressure on US interest rates. A similar dynamic has emerged as a possibility from the troubled Gulf states – suggesting this is a structural feature of the new global economy, not something specific to Japan.

Third, the US economy has been running close to overheating for several years and still is, which calls for higher interest rates, not lower ones. US employment has been near maximum levels for 55 consecutive months, while the central bank has missed its inflation target for 63 months.

Fourth, while AI – Warsh's rationale for lowering interest rates – may create disinflation over the long term, its near-term effects have been more inflationary: demand for the metals, energy and chips needed to build data centers has driven up the costs of all three.

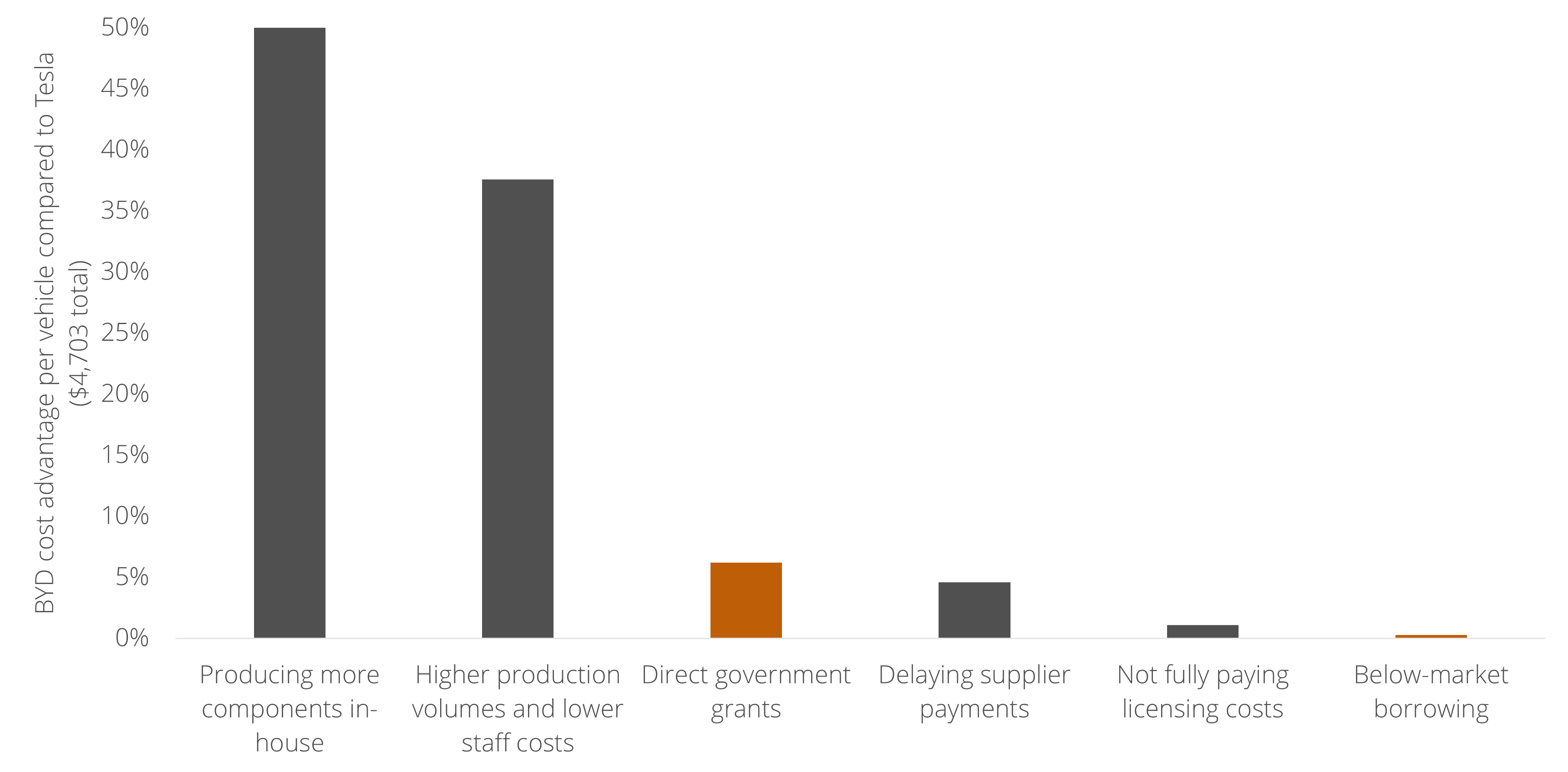

Last week, a new OECD report on industrial subsidies was picked up across western media, highlighting the finding that Chinese companies receive 3 to 8 times more government support than their western counterparts. However, a careful reading of the OECD report shows this figure is misleading – and that framing China's rise as mainly enabled by government subsidies will lead to the wrong response.

First, the OECD shows that higher subsidies for Chinese companies are entirely dependent on below-market borrowing – in other words, relatively low interest rates on loans from Chinese banks to Chinese companies. When it comes to direct grants and income-tax concessions, western governments subsidize their companies at comparable levels as China. This matters because China's below-market borrowing is, as experts like Michael Pettis have shown, a structural feature of its political-economic system: in China, capital is channeled to companies through state banks at below-market rates to keep the economy dependent on investment-led growth, effectively paid for by Chinese households, who receive artificially low returns on their savings. This is not a targeted subsidy program, but something far more deeply embedded in how the Chinese Communist Party chooses to develop the country - and therefore not something that will be overcome through responses like import tariffs or western subsidies.

Second, and this is what deserves closer attention, the OECD data shows significant variation between industries. The automotive industry is worth examining, because it is the sector that both the US and the EU have targeted with import tariffs, explicitly justified by claims of unfair Chinese subsidies. Research by the Rhodium Group shows that only 5% of the cost advantage of Chinese cars is based on government subsidies. The remaining 95% reflects genuine competitive strengths: the vertical integration of Chinese manufacturers – who produce their own batteries and other components or source them domestically, unlike western firms that rely on complex global supply chains – and higher levels of investment in research and development, supported by lower labor costs and a longer planning horizon.

The implication is that framing the rise of Chinese companies as primarily a subsidy story leads to the wrong response. For instance, since the EU raised import tariffs on Chinese cars in October 2024, the market share of Chinese cars in Europe has continued to grow, while some European manufacturers that produce their cars in China lost market share, as they found themselves penalized by their own governments' tariffs. Rather than focusing on penalizing China for its industrial model, western governments would be wise to address their own competitiveness – and to maintain access to world-class Chinese products in the meantime.

During the last week, the European Union took significant steps on three of the most important political issues on the continent: the asylum system, the capital markets union, and China. Together, they reveal a Europe in which a renewed sense of unity is driving progress in some areas, while deep divisions persist in others - and both forces are equally likely to shape Europe’s future.

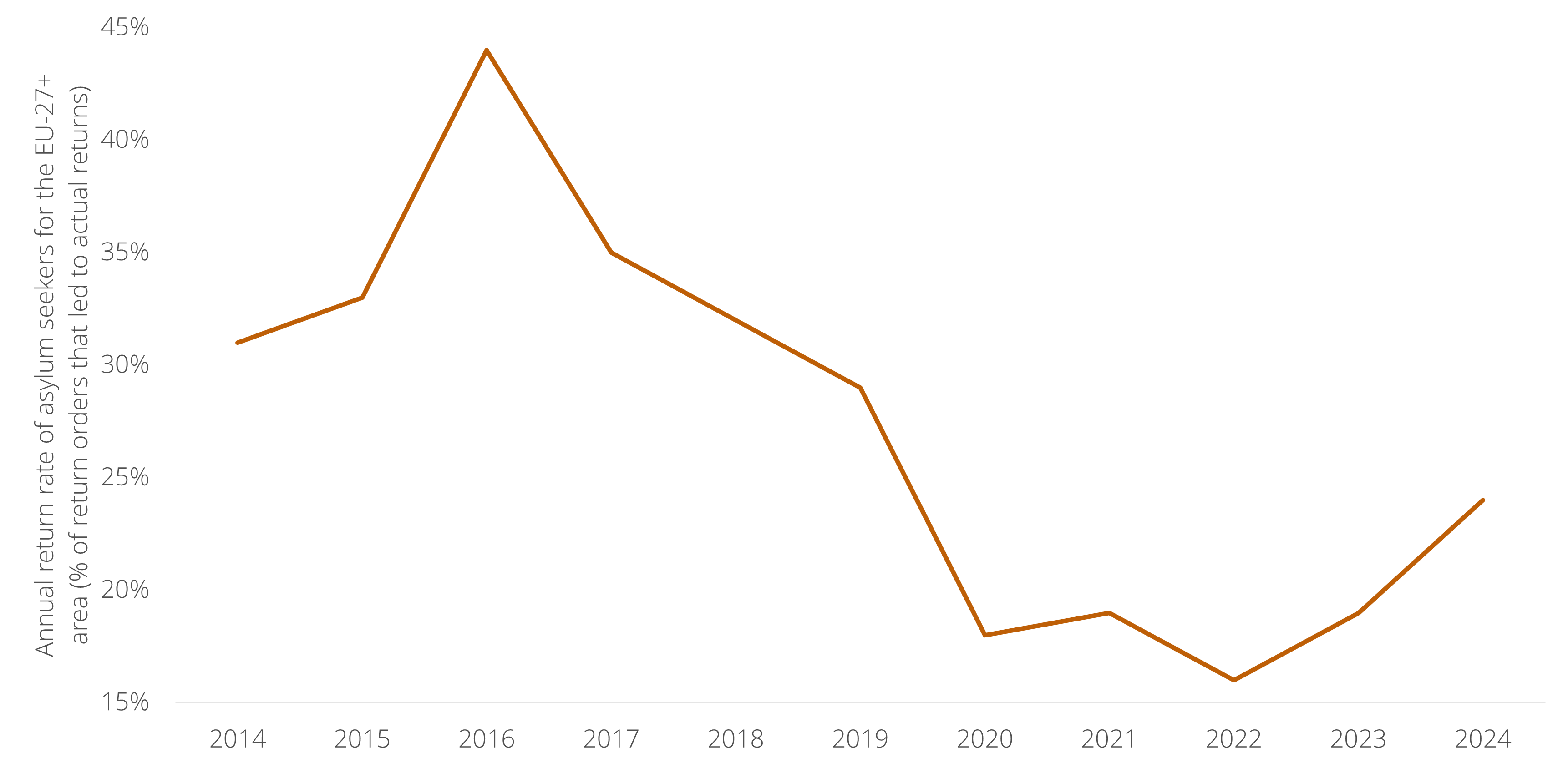

Asylum. The EU is moving forward with legislation to establish return hubs in non-EU countries for asylum seekers who have been denied entry and must be returned to their country of origin. Currently, more than 70% of those ordered to leave never actually do so. This could become the most significant asylum legislation in decades and reflects a new degree of political unity on the topic.

Capital markets union. The six largest EU economies have agreed on first principles for a capital markets union that would gradually replace national investment regimes with a single European framework. The plan is widely seen as capable of significantly improving conditions for doing business across Europe and attracting greater flows of global capital. The countries involved are pressing for urgency and want an actionable plan by the end of the year.

China. As a new trade conflict between the EU and China shows signs of escalating, Spain - known for its China-friendly approach, including welcoming Chinese investment in solar, batteries and electric vehicles - pulled back from a French-led initiative to develop European tools to restrict Chinese imports. Spain's minister for economy and trade stated that Europe should focus on engaging with Chinese authorities and remain open to Chinese investment, rather than pursuing legislation that further damages the trade relationship.

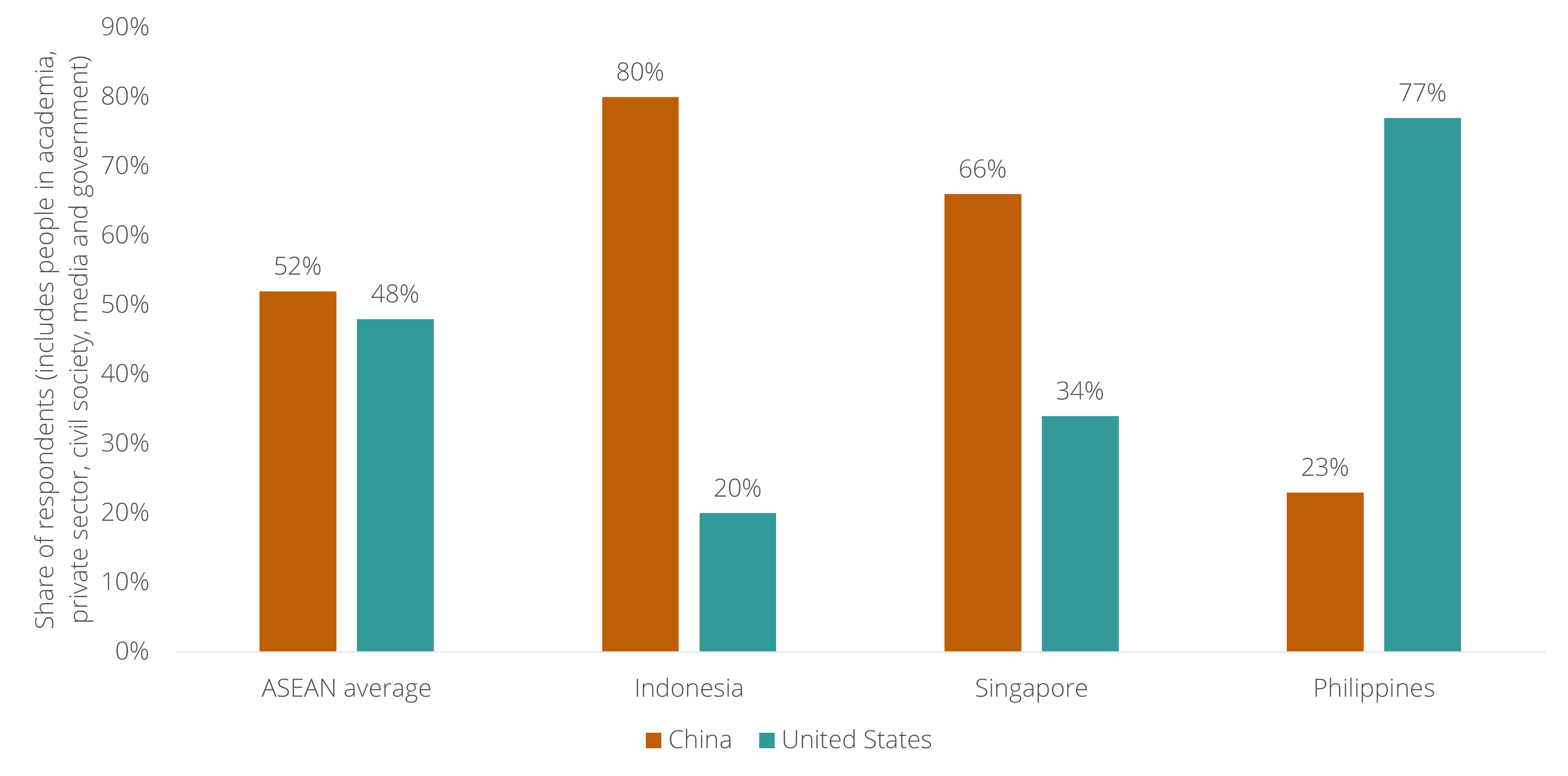

A Singaporean think-tank has found that 66% of Singaporean opinion leaders would side with China over the United States if forced to choose - a striking figure for one of Washington's closest partners in the region.

Europeans should resist filing this under "Asian story." Singapore (and ASEAN more broadly) sit in Europe's predicament: the US is their most important security partner and China is their most important trade partner – and they would rather not choose at all.

As news emerges of escalation in the trade conflict between Europe and China, it may seem naive to point to the opportunity of them working more closely together. However, we should not be surprised if that is exactly what happens in the coming years. Europe and China share a fundamental goal in the transition to clean energy, and to complete it, they need each other.

The transition to clean energy is a shared goal for Europe and China, albeit for different reasons. In China, clean energy is central to the country's economic reform plan, in which the economy transitions away from investing in real estate and infrastructure and towards high-tech manufacturing, including clean energy technologies. In Europe, besides climate targets, successive global crises have made its energy system expensive and vulnerable to disruption, necessitating a transition towards clean, local energy sources.

What is sometimes underappreciated is that, because of this shared goal, clean energy has already become a key driver of economic growth for both (see chart). In China, clean energy industries account for 25% of GDP growth; in Europe, more than 30%. In the US, the figure is just over 5%.

Most importantly, to complete the transition to clean energy, Europe and China need each other. Europe cannot achieve energy security without affordable Chinese technologies, and China cannot sustain its export model without reaching agreement with advanced economies like Europe on the rules for market access.

The key question is how exactly Europe and China will be able to cooperate amid conflict – driven mainly by Europe's concerns about overreliance on Chinese products – especially at a time when tensions are still escalating. The answer lies in the current energy crisis. Europe will increasingly discover that the greatest value from clean energy lies not in manufacturing these technologies (solar panels, wind turbines, heat pumps) but in deploying and integrating them with the local energy system, as this is what unlocks the potential of the broader economy. The Netherlands is a case in point: its congested electricity grid is already preventing new business formation even outside industrial production.

The main bottleneck for cooperation between Europe and China is therefore not economic competition but strategic security: Europe does not want to become overly reliant on a single country for its energy needs again. This will drive European policy towards a logic of diversification – as seen this week in the area of chemicals – rather than punishment (like the US approach of import tariffs on Chinese goods). This European approach could, like the Western quota policies on Japanese imports in the 1980s, provide the basis for diplomatic agreement.