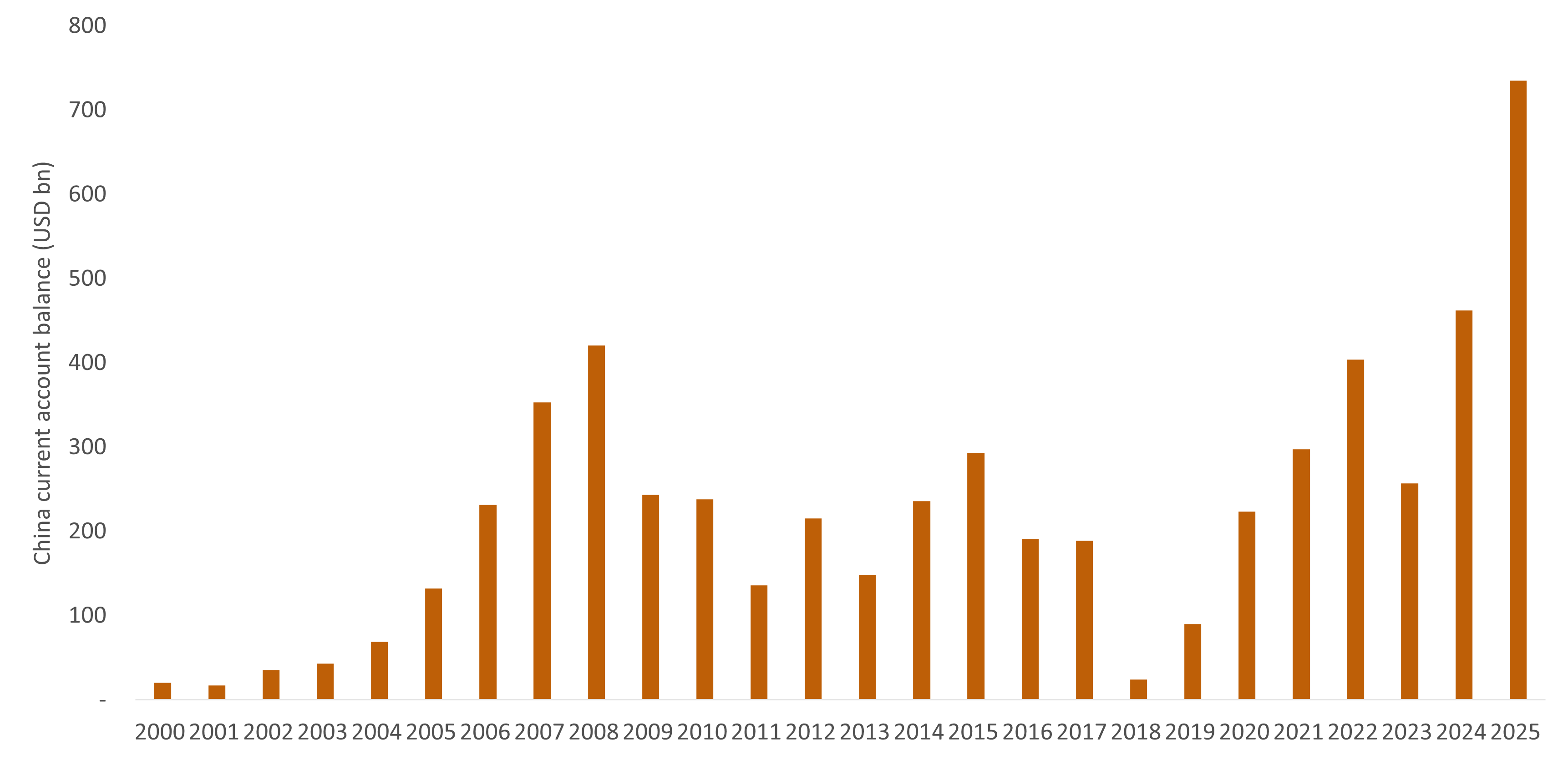

In 2025, China recorded the largest merchandise trade surplus in history – roughly $1.1 trillion more in exports than imports – based on Chinese manufacturers' global competitiveness. The alarm this has provoked in the United States and Europe over the fate of their own industries has dominated the debate. Far less attention has gone to another question: where is all this Chinese capital going? A trade surplus does not simply disappear. Every dollar China earns abroad and does not spend on imports must be reinvested abroad – the question is through which channel.

For two decades from the early 2000s, much of China's surplus was recycled into US Treasuries. But that has changed: Chinese capital no longer flows automatically to the US. The largest destination for China's capital in recent years has been Hong Kong – though much of it flows through the territory rather than settling there, using Hong Kong as a conduit to other foreign markets.

In the years ahead, more countries are likely to compete for access to Chinese capital rather than resist it. At the European level, this almost happened in December 2020 when the EU and China concluded the Comprehensive Agreement on Investment, which would have opened a return channel for Chinese surplus capital into Europe – including partnerships that would have shored up Europe's industrial competitiveness through a new energy system with lower energy costs. The deal was shelved at the last moment, but the logic that produced it has not gone away: Spain and Hungary are already building long-term national strategies that position Chinese capital as a funding engine for European reindustrialization, and others are likely to follow.