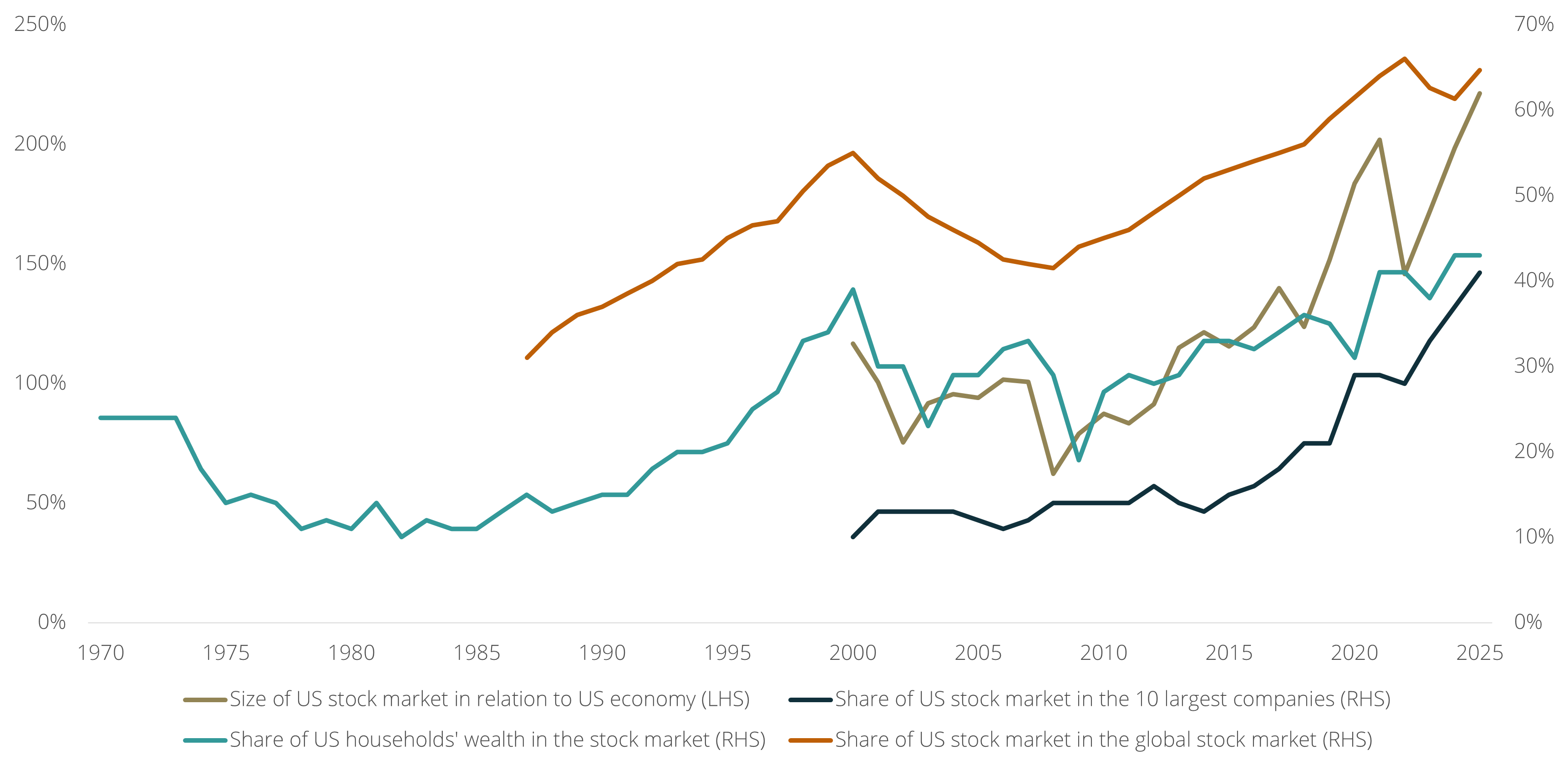

There has been a lot of discussion in recent weeks about the financial markets’ concentration in AI-related companies, with the question whether AI can fulfill its promise at the center of the debate. However, the concentration in AI is only one of five elements in a much bigger and more extreme concentration in the global financial system, reflecting how vulnerable the system has become in the past few years. First, the share of the US stock market as a percentage of the global stock market is at a record high (65%), making many investors, including pension funds, extremely sensitive to a correction in the US stock market. Second, the size of the US stock market relative to the size of the US economy is also at a record high (221%), suggesting that much of the recent growth is based on financial speculation rather than ‘real’ economic value. Third, the share of the top 10 companies in the US stock market is at a record high (41%), indicating that the rest of the economy is growing at a much slower pace (without investments by AI-related companies, the US economy was in recession in 2025). Fourth, US households have never been more invested in the stock market (43% of their wealth), implying that a correction would hit households’ finances relatively hard. Finally, the top 10% of US households (measured by income) own around 90% of the US stock market (a record high) and account for 34% of US consumption (also a record high), suggesting that a market downturn could slow consumer spending and trigger a recession—an unprecedented scenario, as historically it is usually the recession that triggers the market downturn, not the other way around.