One way in which the 2026 war in Iran will be remembered – if the situation does not escalate further – is that the largest oil supply disruption in history triggered a far smaller oil crisis than expected. A key reason, besides the US withdrawing from the conflict without achieving its objectives, is China's oil reserves. When the war broke out, China stopped importing oil and began drawing on those reserves, which relieved pressure on global oil markets. This matters because it demonstrates that stockpiling and diversification of key commodities – a topic that has received intense attention since COVID – can be very effective.

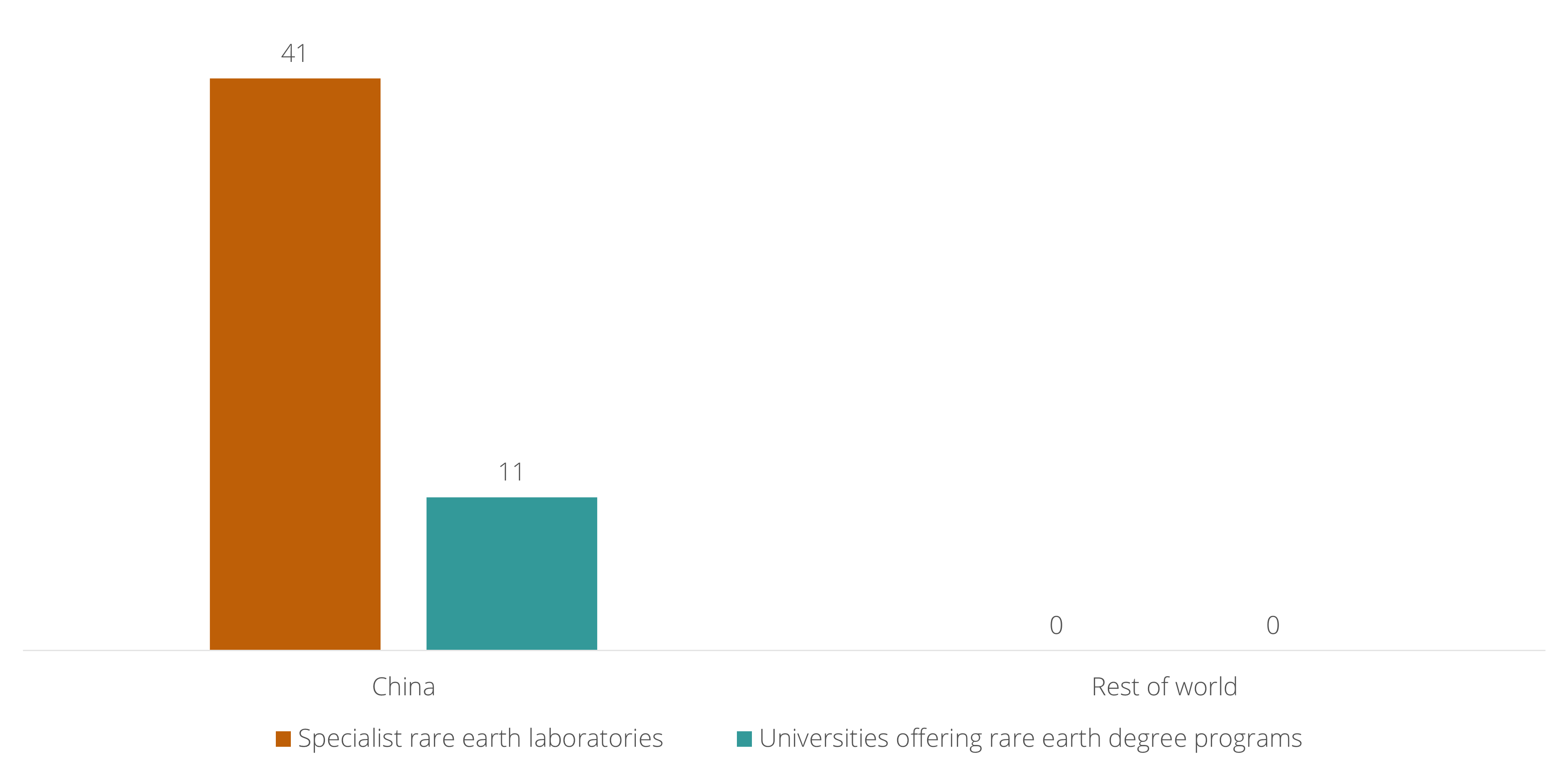

The EU has identified diversification of key commodities as a political goal, just like the US and China, but compared to them has the longest way to go. For its energy needs, Europe has infamously traded its dependency on Russian gas for a dependency on American liquefied natural gas – which is also more expensive, a cost that continues to weigh on European industry’s “existential” situation. This shows that the war in Ukraine did not produce any serious diversification in European energy supply. For its metals needs, the challenge is greater still. Last week, the G7 announced a 60% target to cap dependency on rare earth imports from any single source – meaning China, which holds a market share of up to 99% in some metals. But how the mining and processing of these materials will scale up, short of major investment projects spanning multiple decades, remains the central question. It is telling that Reuters recently reported on China's vast ecosystem of rare earth laboratories and university programs – and could not identify a single comparable education program outside China.