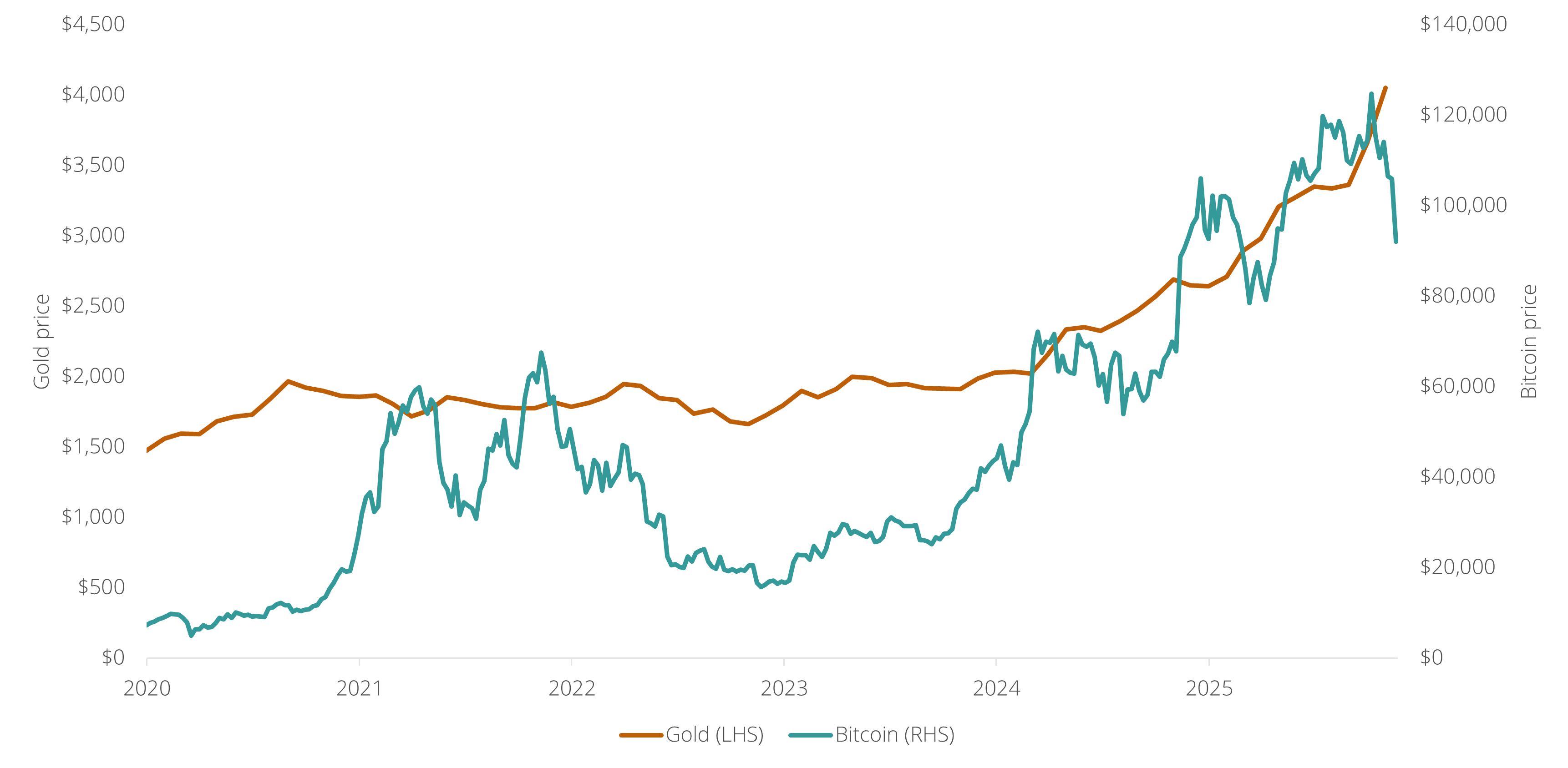

When Bitcoin launched in 2009, it was designed as a form of money that could not be devalued by governments through inflation – unlike dollars and euros that can be created by central banks. Gold has historically served a similar role as a hedge against the eroding value of government-backed currencies, which is why bitcoin enthusiasts have long called it "digital gold". Yet comparing the price development of gold and bitcoin shows a stark contrast: while gold's value is relatively stable, bitcoin has become an extremely volatile asset over the past 17 years, suggesting it does not function as originally intended. A new study indicates that bitcoin also plays a different role. For a growing number of people, cryptocurrency has become a lottery ticket to homeownership. The research shows that among homeowners, crypto ownership rises gradually with wealth, but among renters it is highest among those with the lowest wealth – pointing to a "gambling for redemption" motive: risk-taking as a last resort to become a homeowner.

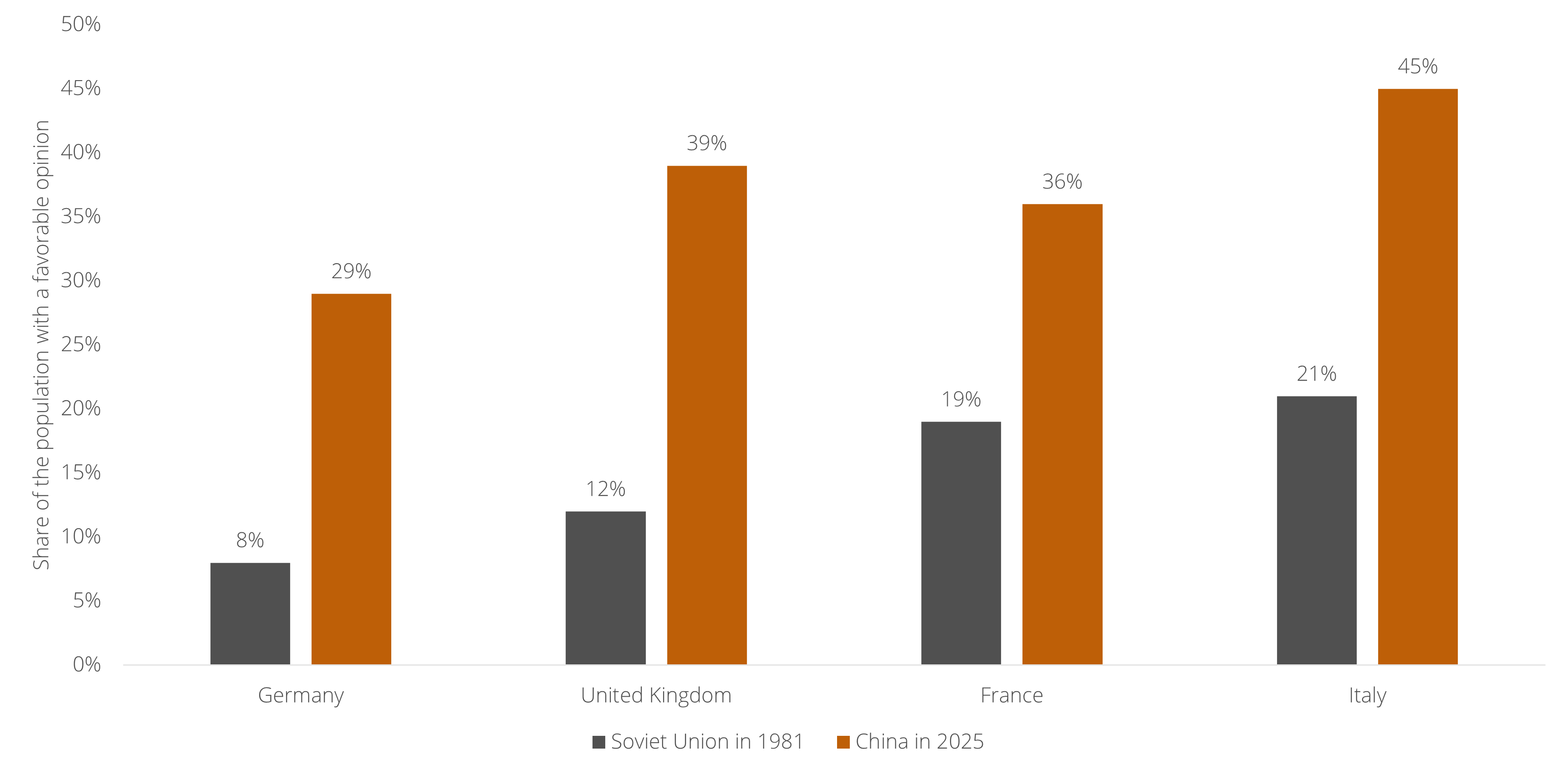

In today’s great-power conflict, many observers cast China as almost a mirror image of the Soviet Union, shaping the narrative that we are living through a “Second Cold War.” Yet one crucial difference between the Soviet Union then and China now is almost never acknowledged: China enjoys a far more favorable image among Western publics than the Soviet Union ever did. Throughout the Cold War, positive views of the USSR rarely exceeded 20% in Europe, whereas in 2025 favorability toward China in some European countries is approaching 50%. A shift is especially pronounced among younger generations, with major social media influencers such as Hasan Piker and IShowSpeed traveling to China in 2025 and telling a positive story about China to their tens of millions of followers – despite accusations of propaganda – focused on China's cutting-edge innovation in robotics and vehicles.

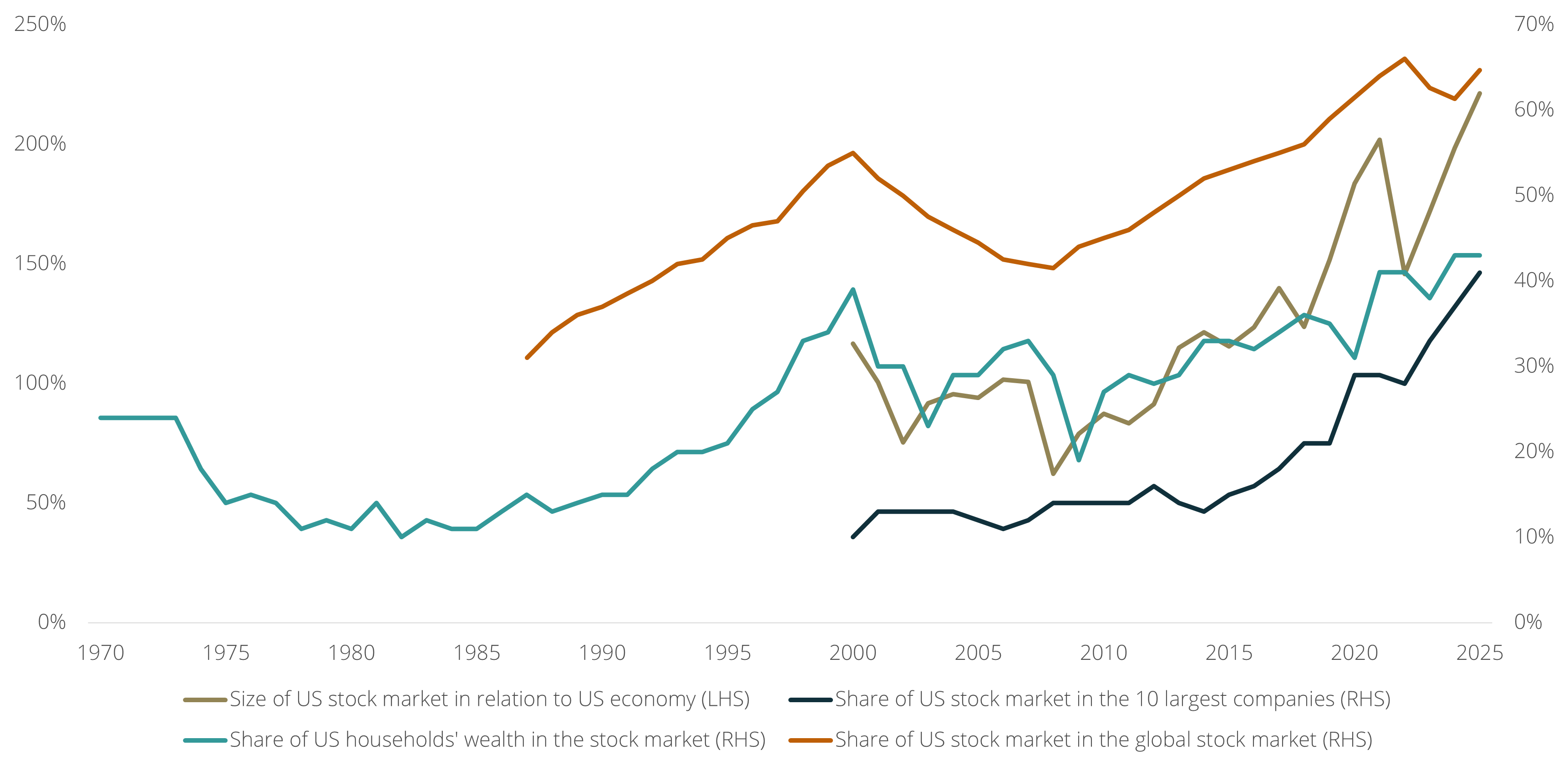

There has been a lot of discussion in recent weeks about the financial markets’ concentration in AI-related companies, with the question whether AI can fulfill its promise at the center of the debate. However, the concentration in AI is only one of five elements in a much bigger and more extreme concentration in the global financial system, reflecting how vulnerable the system has become in the past few years. First, the share of the US stock market as a percentage of the global stock market is at a record high (65%), making many investors, including pension funds, extremely sensitive to a correction in the US stock market. Second, the size of the US stock market relative to the size of the US economy is also at a record high (221%), suggesting that much of the recent growth is based on financial speculation rather than ‘real’ economic value. Third, the share of the top 10 companies in the US stock market is at a record high (41%), indicating that the rest of the economy is growing at a much slower pace (without investments by AI-related companies, the US economy was in recession in 2025). Fourth, US households have never been more invested in the stock market (43% of their wealth), implying that a correction would hit households’ finances relatively hard. Finally, the top 10% of US households (measured by income) own around 90% of the US stock market (a record high) and account for 34% of US consumption (also a record high), suggesting that a market downturn could slow consumer spending and trigger a recession—an unprecedented scenario, as historically it is usually the recession that triggers the market downturn, not the other way around.