Over the past year, we have followed two contrarian China trends. In recent weeks, both have been confirmed.

First: Chinese AI has reached the frontier at a fraction of the cost. We argued this in "In 2026, China Leads the United States in Both International Relations and Technological Innovation", "China Is Winning in Innovation Where It Counts: Markets, Not Just Research", and "China Has Closed the Gap With the United States in Artificial Intelligence". The evidence has now caught up: Apollo shows Chinese open-weight models trail the US frontier by just four months, while Moonshot's Kimi K3 recently outranked Anthropic's Opus 4.8 in blind testing. American developers are switching en masse to cheaper Chinese models like DeepSeek. This matters for investors because the AI boom is built on the assumption that US labs could charge premium prices and has driven significant US stock market gains in recent years.

Second: global opinion of China, in particular among young people, is improving, especially relative to the US. We wrote this in "China Already Has More Soft Power Than the Soviet Union Ever Did" and "A Majority of Singaporeans Now Prefer China to the US". This month, Pew confirmed it. Across 37 countries, 51% of the people have a favorable view of China, while 39% have an unfavorable view. Crucially, younger people in most countries have more favorable views of China than older people.

The conflict between Saudi Arabia and the UAE is showing new signs of escalating. If current trends continue, this could raise question marks around the $3 trillion managed by the sovereign wealth funds of both countries — much of which flows to western markets.

In January 2026, a month before the war between the US and Iran broke out, we warned that the conflict between Saudi Arabia and the UAE was likely to escalate during this year. As soon as the war began, we warned that it was likely to threaten the safe haven status of the Gulf states, as a significant amount of capital was likely to leave the region permanently. A few weeks later, we reaffirmed that the risk of a financial crisis in the Gulf was growing, as the UAE requested a currency swap line with the Fed. Next, the UAE took the extraordinary step of leaving the OPEC oil cartel, as it can afford a much lower oil price than OPEC leader Saudi Arabia. In recent weeks, new signs of stress have emerged, as Saudi Arabia has reportedly blocked financial flows to the UAE.

Looking ahead, a relevant analogy is the conflict between Qatar and Saudi Arabia (backed by the UAE), which led to a blockade of Qatar in 2017. It severely depressed foreign direct investment into the country for years — and a similar, but far larger, financial shock could follow if the conflict between Saudi Arabia and the UAE continues to escalate.

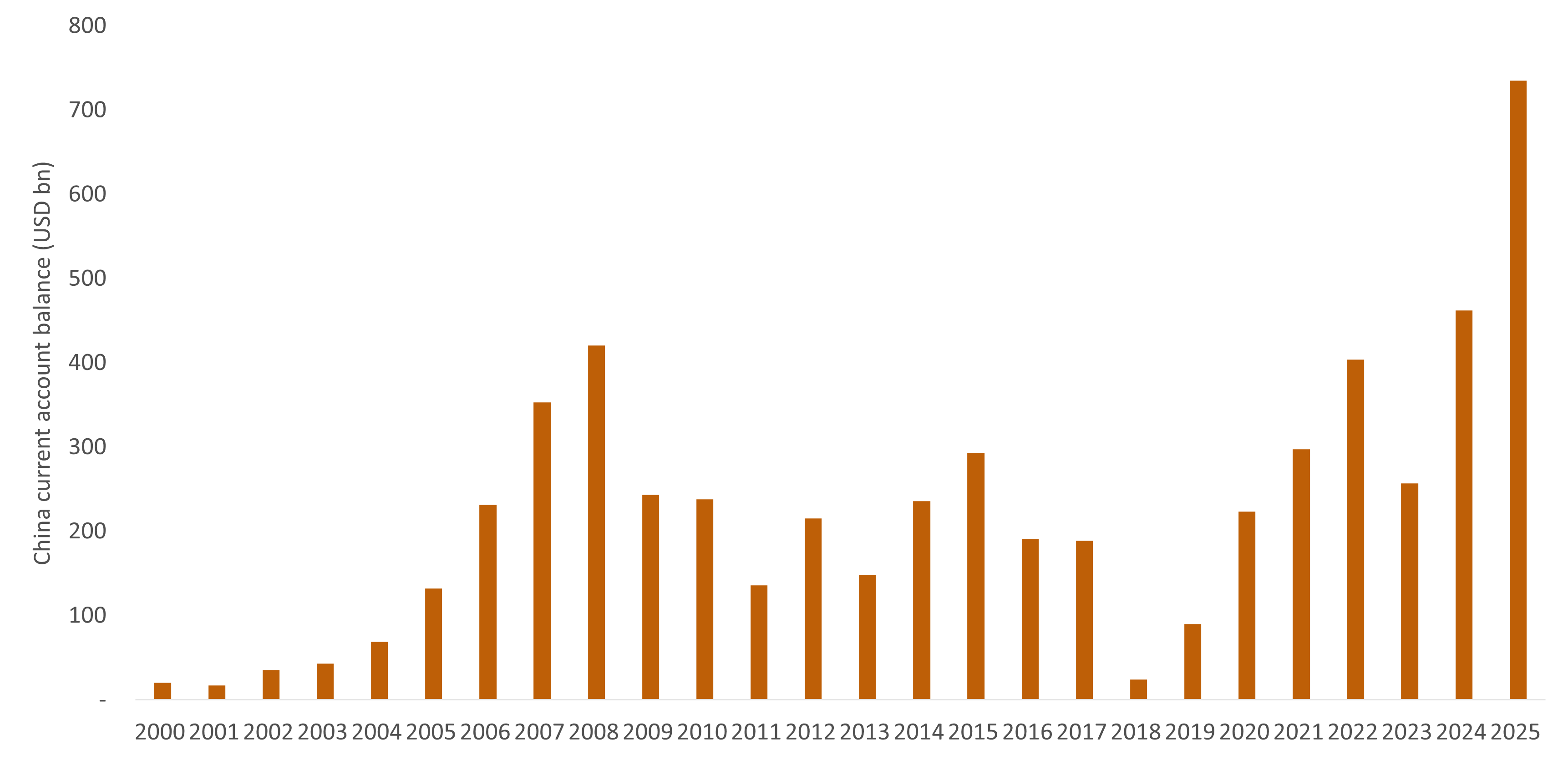

In 2025, China recorded the largest merchandise trade surplus in history – roughly $1.1 trillion more in exports than imports – based on Chinese manufacturers' global competitiveness. The alarm this has provoked in the United States and Europe over the fate of their own industries has dominated the debate. Far less attention has gone to another question: where is all this Chinese capital going? A trade surplus does not simply disappear. Every dollar China earns abroad and does not spend on imports must be reinvested abroad – the question is through which channel.

For two decades from the early 2000s, much of China's surplus was recycled into US Treasuries. But that has changed: Chinese capital no longer flows automatically to the US. The largest destination for China's capital in recent years has been Hong Kong – though much of it flows through the territory rather than settling there, using Hong Kong as a conduit to other foreign markets.

In the years ahead, more countries are likely to compete for access to Chinese capital rather than resist it. At the European level, this almost happened in December 2020 when the EU and China concluded the Comprehensive Agreement on Investment, which would have opened a return channel for Chinese surplus capital into Europe – including partnerships that would have shored up Europe's industrial competitiveness through a new energy system with lower energy costs. The deal was shelved at the last moment, but the logic that produced it has not gone away: Spain and Hungary are already building long-term national strategies that position Chinese capital as a funding engine for European reindustrialization, and others are likely to follow.

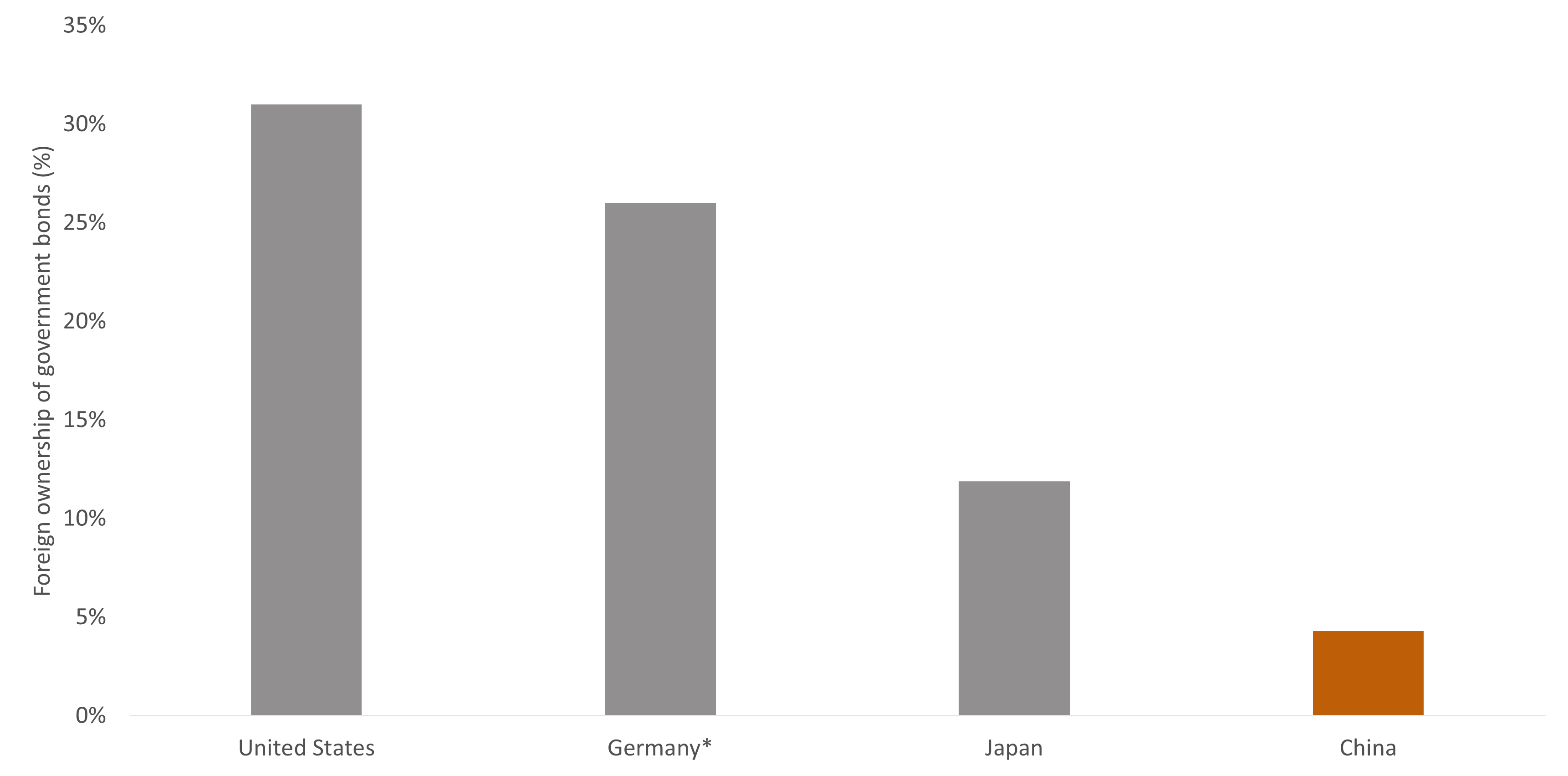

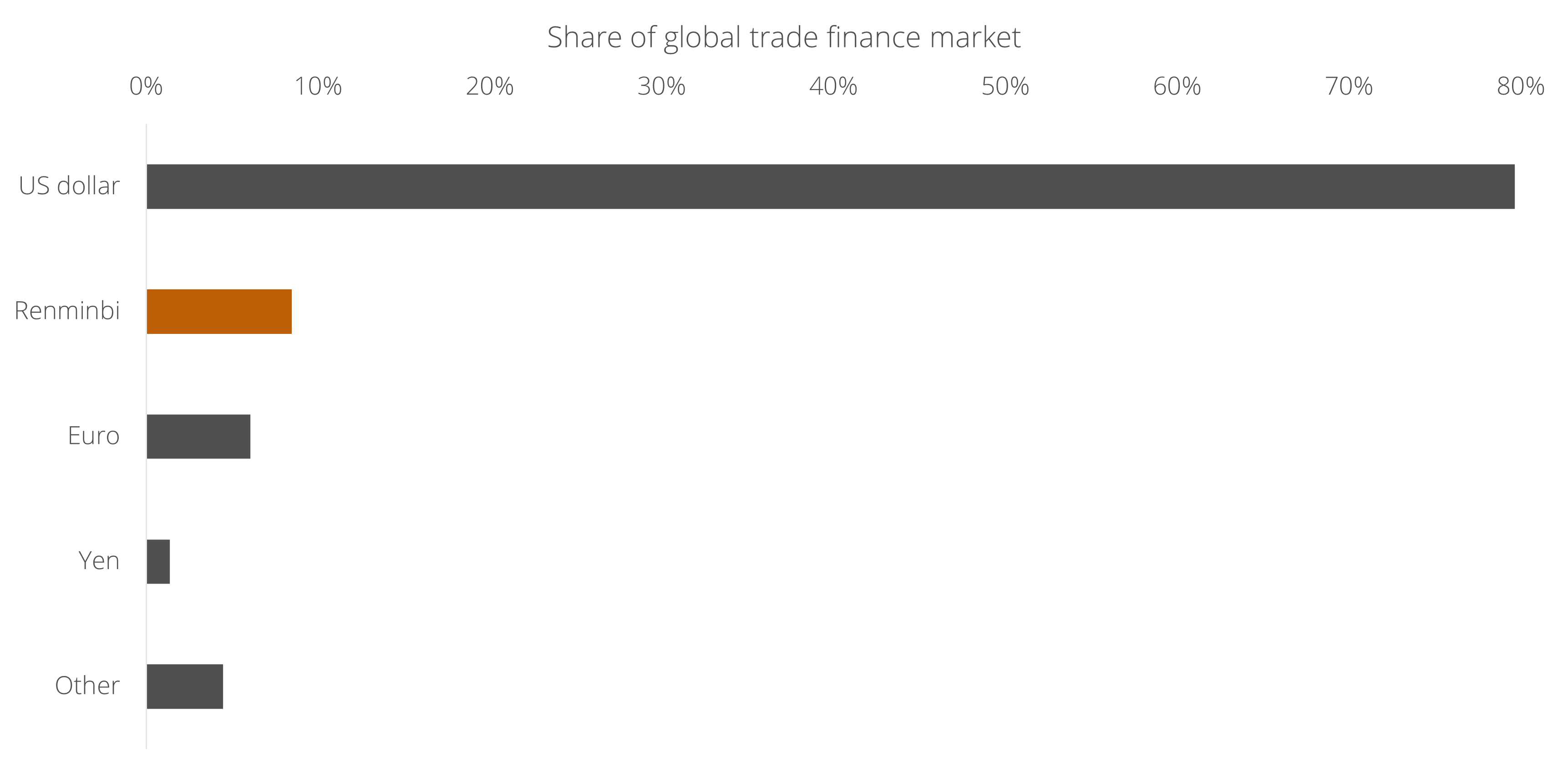

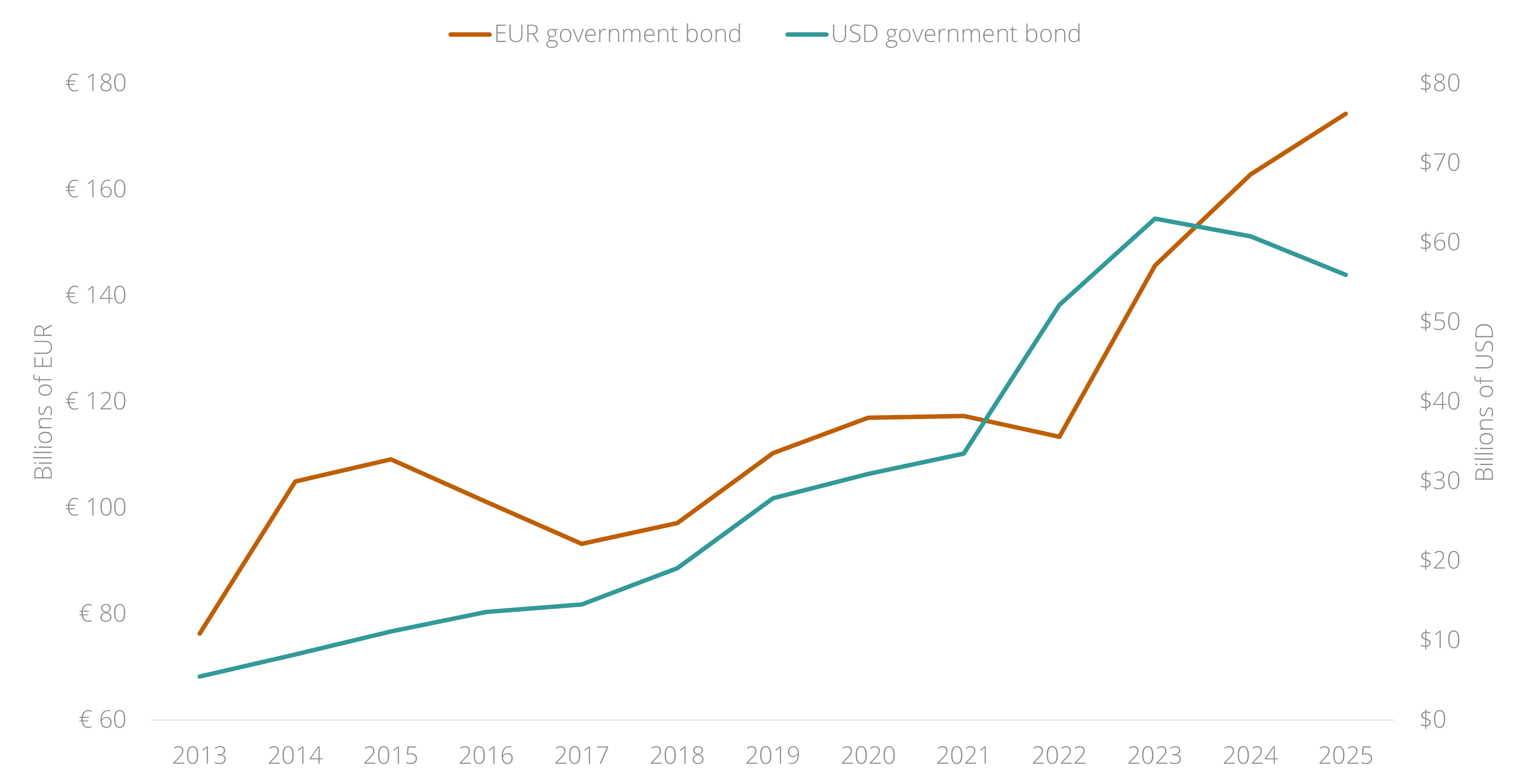

In recent weeks, China announced several significant steps to address the barriers that hold back adoption of the renminbi by global investors.

1. Chinese government bonds can now be quickly converted into cash - making them far more attractive to hold. Through a new repo facility, foreign investors will be able to use their Chinese government bond holdings as collateral to borrow short-term renminbi cash. This mirrors the US Federal Reserve’s repo facility, which lets foreign central banks swap US government bonds for dollars. Previously, Chinese government bonds were difficult to liquidate quickly, making them relatively unattractive to hold for global investors who need to be able to move in and out of positions.

2. Global investors can now protect themselves against losses on Chinese bond holdings - removing a key barrier to owning them. A new Hong Kong-based futures market for Chinese government bonds will allow global investors to hedge interest rate risk in their Chinese bond holdings without needing mainland China market access. The absence of such a hedging mechanism was a key reason for underweighting Chinese bonds in global investment portfolios.

3. More support for two-way capital flows - a necessary step in making the renminbi a currency global investors can comfortably hold. China has increased the quotas under its Qualified Domestic Institutional Investor program, allowing more Chinese capital to flow into foreign markets. Enabling outward capital flows is a classic step in the internationalization of a domestic currency because it creates a two-way market and reduces the perception of a one-way trap.

4. More support for the offshore renminbi, which is freely traded outside China - making it easier for global investors to transact in the currency. Six major state-owned banks have been authorized to conduct transactions in offshore renminbi - a currency market distinct from the onshore renminbi, freely traded in financial centers such as Hong Kong and Singapore - directly from the mainland. Previously, such transactions had to be routed through these offshore hubs. This is likely to increase the pool of freely traded renminbi in global markets.

Analysis of the internationalization of the renminbi should go further than reflecting on “de-dollarization” - although foreign demand for US dollars could indeed decline as the renminbi becomes a more credible alternative. More importantly, the internationalization of the renminbi is likely to begin in Asia, where central banks and sovereign wealth funds have the most to gain from diversifying into renminbi assets, something Chinese government statements in recent years have made explicit. The infrastructure to support that vision is now being put in place, and global investors would be unwise to ignore it.

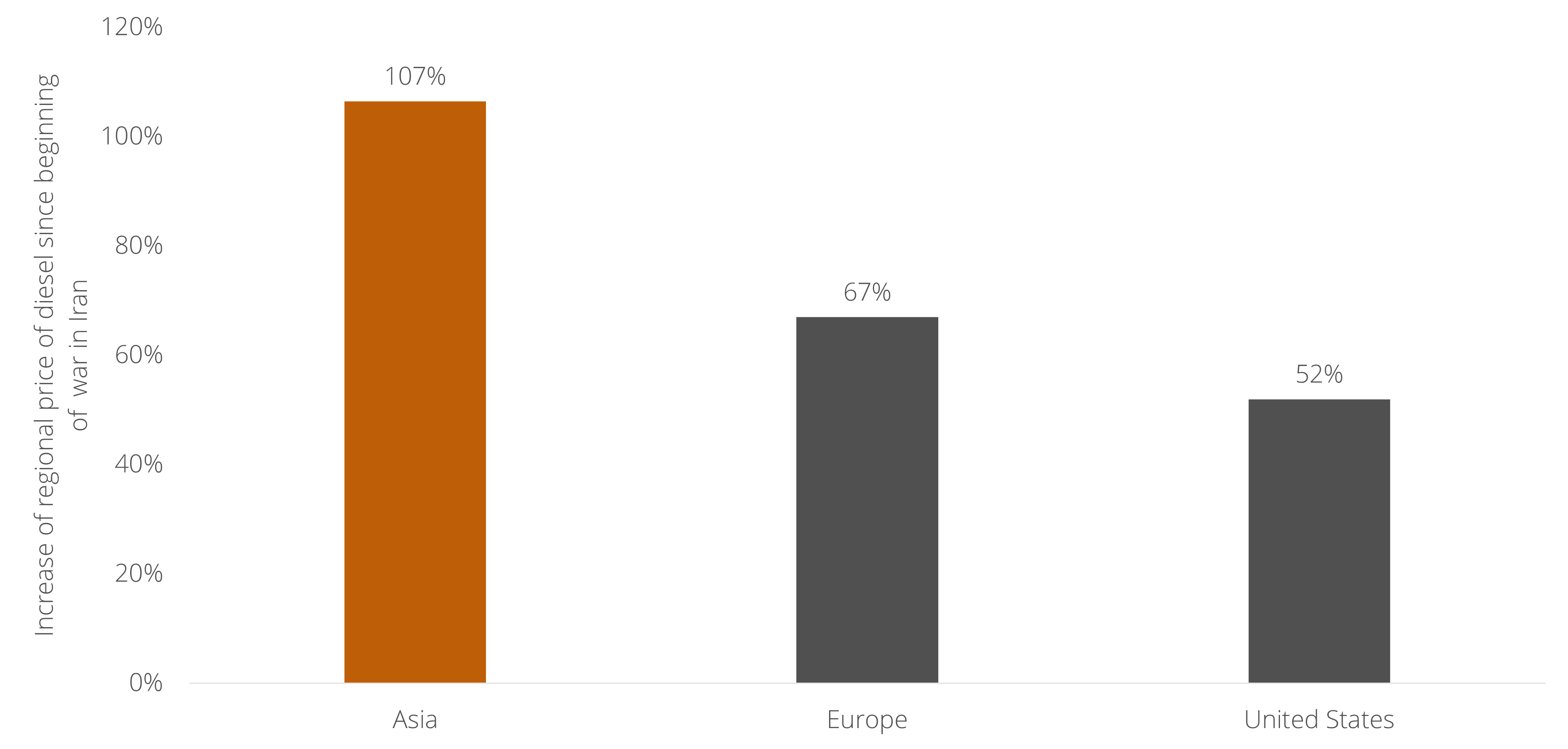

One way in which the 2026 war in Iran will be remembered – if the situation does not escalate further – is that the largest oil supply disruption in history triggered a far smaller oil crisis than expected. A key reason, besides the US withdrawing from the conflict without achieving its objectives, is China's oil reserves. When the war broke out, China stopped importing oil and began drawing on those reserves, which relieved pressure on global oil markets. This matters because it demonstrates that stockpiling and diversification of key commodities – a topic that has received intense attention since COVID – can be very effective.

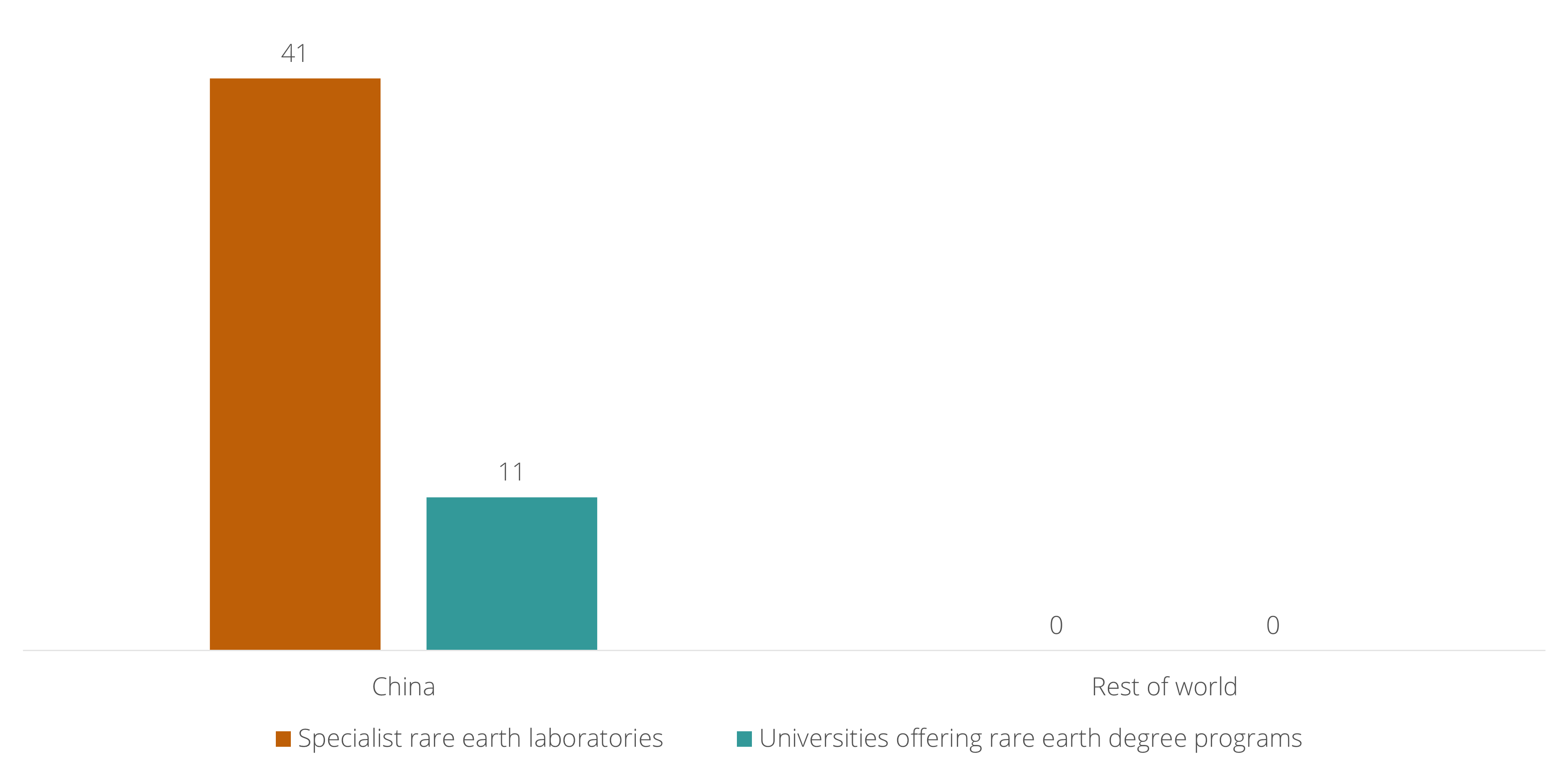

The EU has identified diversification of key commodities as a political goal, just like the US and China, but compared to them has the longest way to go. For its energy needs, Europe has infamously traded its dependency on Russian gas for a dependency on American liquefied natural gas – which is also more expensive, a cost that continues to weigh on European industry’s “existential” situation. This shows that the war in Ukraine did not produce any serious diversification in European energy supply. For its metals needs, the challenge is greater still. Last week, the G7 announced a 60% target to cap dependency on rare earth imports from any single source – meaning China, which holds a market share of up to 99% in some metals. But how the mining and processing of these materials will scale up, short of major investment projects spanning multiple decades, remains the central question. It is telling that Reuters recently reported on China's vast ecosystem of rare earth laboratories and university programs – and could not identify a single comparable education program outside China.

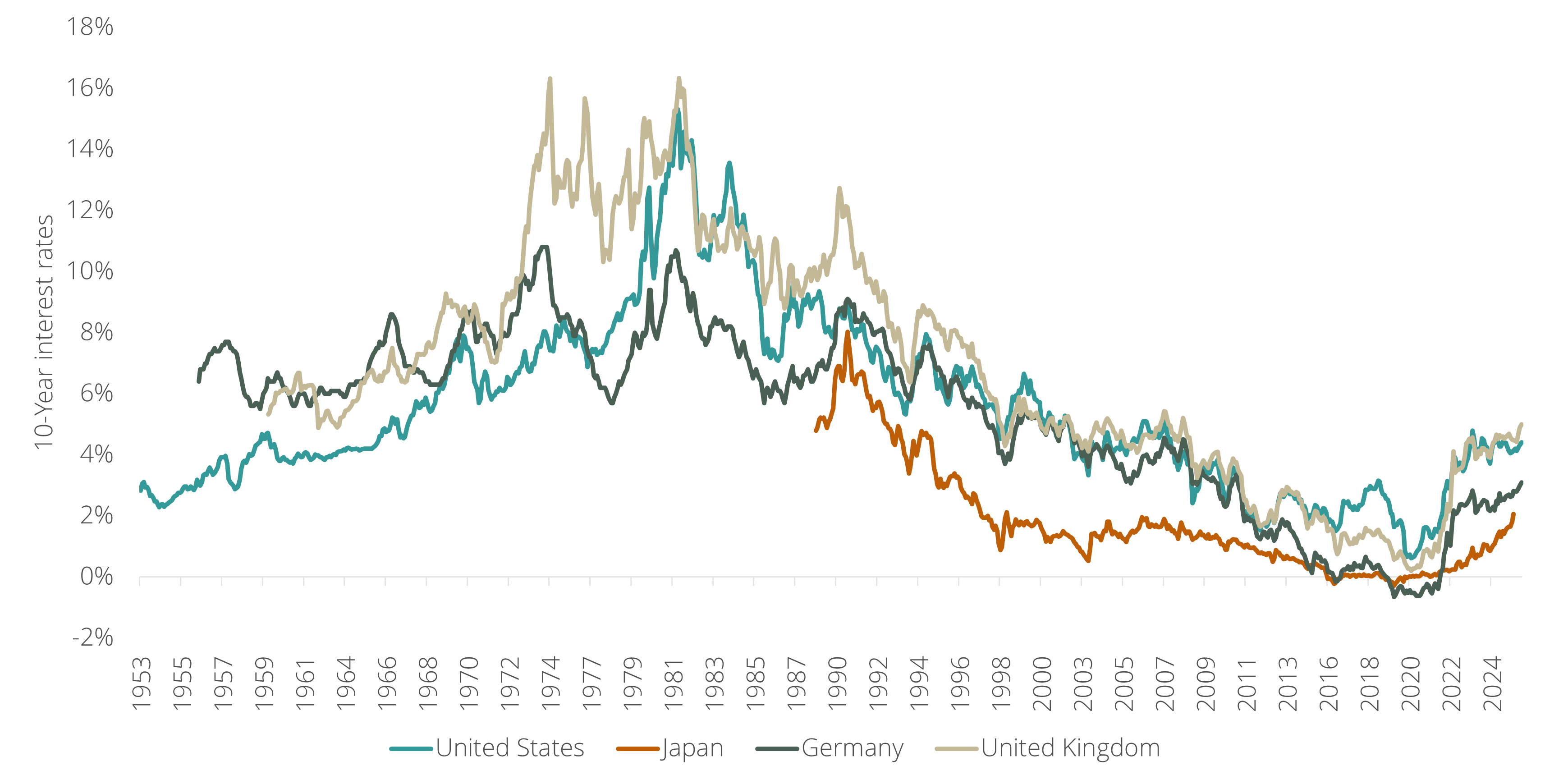

This week, Kevin Warsh begins his term as the US central bank's new chair. He was chosen by Trump for his belief in AI as a driver of lowering costs across the economy, which would open the possibility of cutting the short-term interest rate. However, there are several reasons why US interest rates – both short-term (set by the central bank, which raises them when inflation is too high) and long-term (set by the bond market, which raises them when inflation expectations are elevated or too much debt is being issued) – are likely to remain high and may go even higher.

First, there has been a global regime change in the past five years: interest rates have stopped declining for the first time in decades. There are several structural reasons for this – from massive government spending to international conflicts, all of which raise inflation and consequently interest rates – and such structural changes are unlikely to reverse without a clear cause, such as a meaningful reduction in debt or a resolution of major conflicts, neither of which seems likely anytime soon.

Second, the global shift towards higher interest rates is generating new mechanisms that reinforce the trend. Japan, for instance, may increasingly sell US assets to protect the value of its currency. If Japanese investors were to sell US government bonds at sufficient scale, it would add further upward pressure on US interest rates. A similar dynamic has emerged as a possibility from the troubled Gulf states – suggesting this is a structural feature of the new global economy, not something specific to Japan.

Third, the US economy has been running close to overheating for several years and still is, which calls for higher interest rates, not lower ones. US employment has been near maximum levels for 55 consecutive months, while the central bank has missed its inflation target for 63 months.

Fourth, while AI – Warsh's rationale for lowering interest rates – may create disinflation over the long term, its near-term effects have been more inflationary: demand for the metals, energy and chips needed to build data centers has driven up the costs of all three.

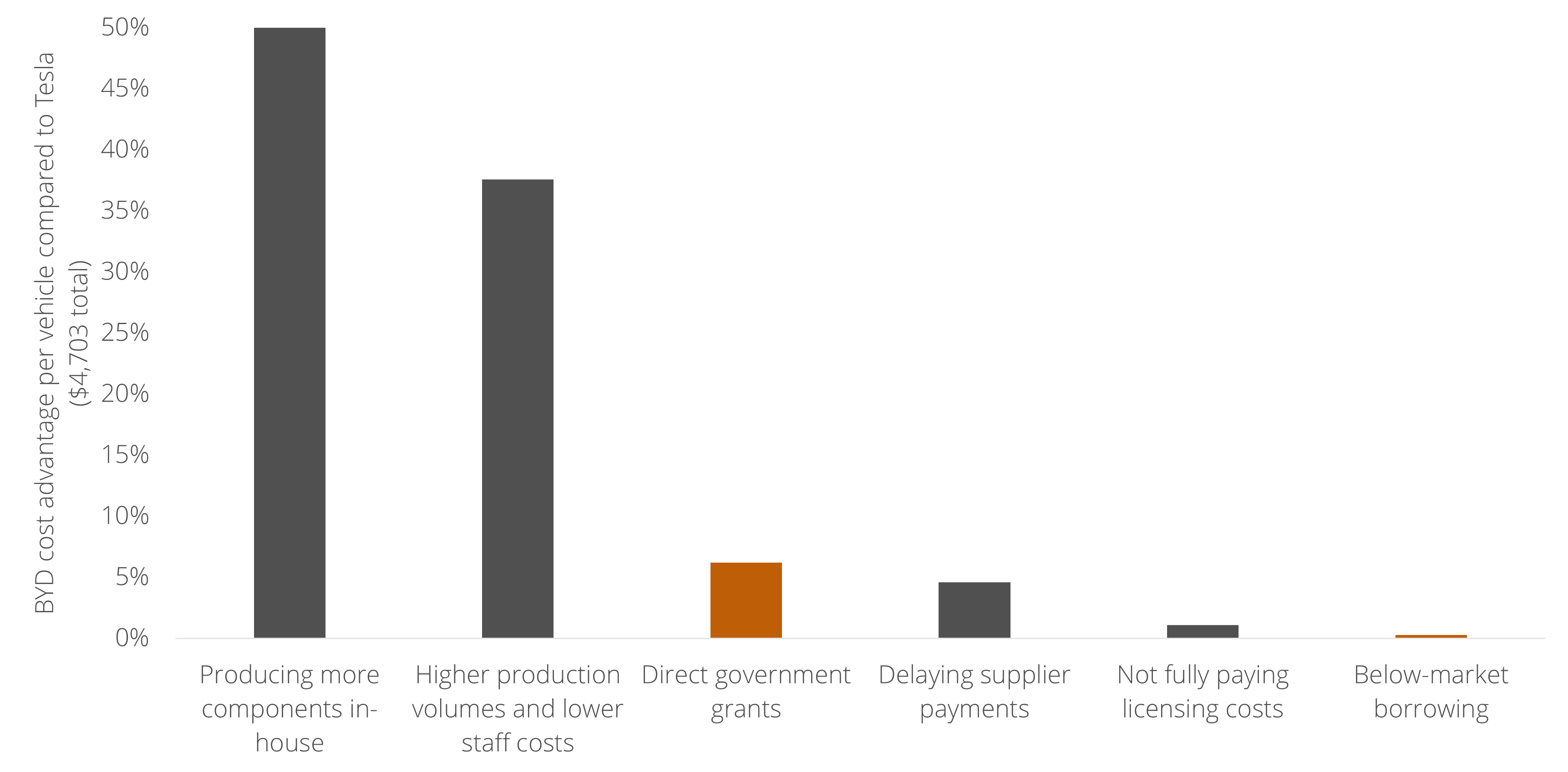

Last week, a new OECD report on industrial subsidies was picked up across western media, highlighting the finding that Chinese companies receive 3 to 8 times more government support than their western counterparts. However, a careful reading of the OECD report shows this figure is misleading – and that framing China's rise as mainly enabled by government subsidies will lead to the wrong response.

First, the OECD shows that higher subsidies for Chinese companies are entirely dependent on below-market borrowing – in other words, relatively low interest rates on loans from Chinese banks to Chinese companies. When it comes to direct grants and income-tax concessions, western governments subsidize their companies at comparable levels as China. This matters because China's below-market borrowing is, as experts like Michael Pettis have shown, a structural feature of its political-economic system: in China, capital is channeled to companies through state banks at below-market rates to keep the economy dependent on investment-led growth, effectively paid for by Chinese households, who receive artificially low returns on their savings. This is not a targeted subsidy program, but something far more deeply embedded in how the Chinese Communist Party chooses to develop the country - and therefore not something that will be overcome through responses like import tariffs or western subsidies.

Second, and this is what deserves closer attention, the OECD data shows significant variation between industries. The automotive industry is worth examining, because it is the sector that both the US and the EU have targeted with import tariffs, explicitly justified by claims of unfair Chinese subsidies. Research by the Rhodium Group shows that only 5% of the cost advantage of Chinese cars is based on government subsidies. The remaining 95% reflects genuine competitive strengths: the vertical integration of Chinese manufacturers – who produce their own batteries and other components or source them domestically, unlike western firms that rely on complex global supply chains – and higher levels of investment in research and development, supported by lower labor costs and a longer planning horizon.

The implication is that framing the rise of Chinese companies as primarily a subsidy story leads to the wrong response. For instance, since the EU raised import tariffs on Chinese cars in October 2024, the market share of Chinese cars in Europe has continued to grow, while some European manufacturers that produce their cars in China lost market share, as they found themselves penalized by their own governments' tariffs. Rather than focusing on penalizing China for its industrial model, western governments would be wise to address their own competitiveness – and to maintain access to world-class Chinese products in the meantime.

During the last week, the European Union took significant steps on three of the most important political issues on the continent: the asylum system, the capital markets union, and China. Together, they reveal a Europe in which a renewed sense of unity is driving progress in some areas, while deep divisions persist in others - and both forces are equally likely to shape Europe’s future.

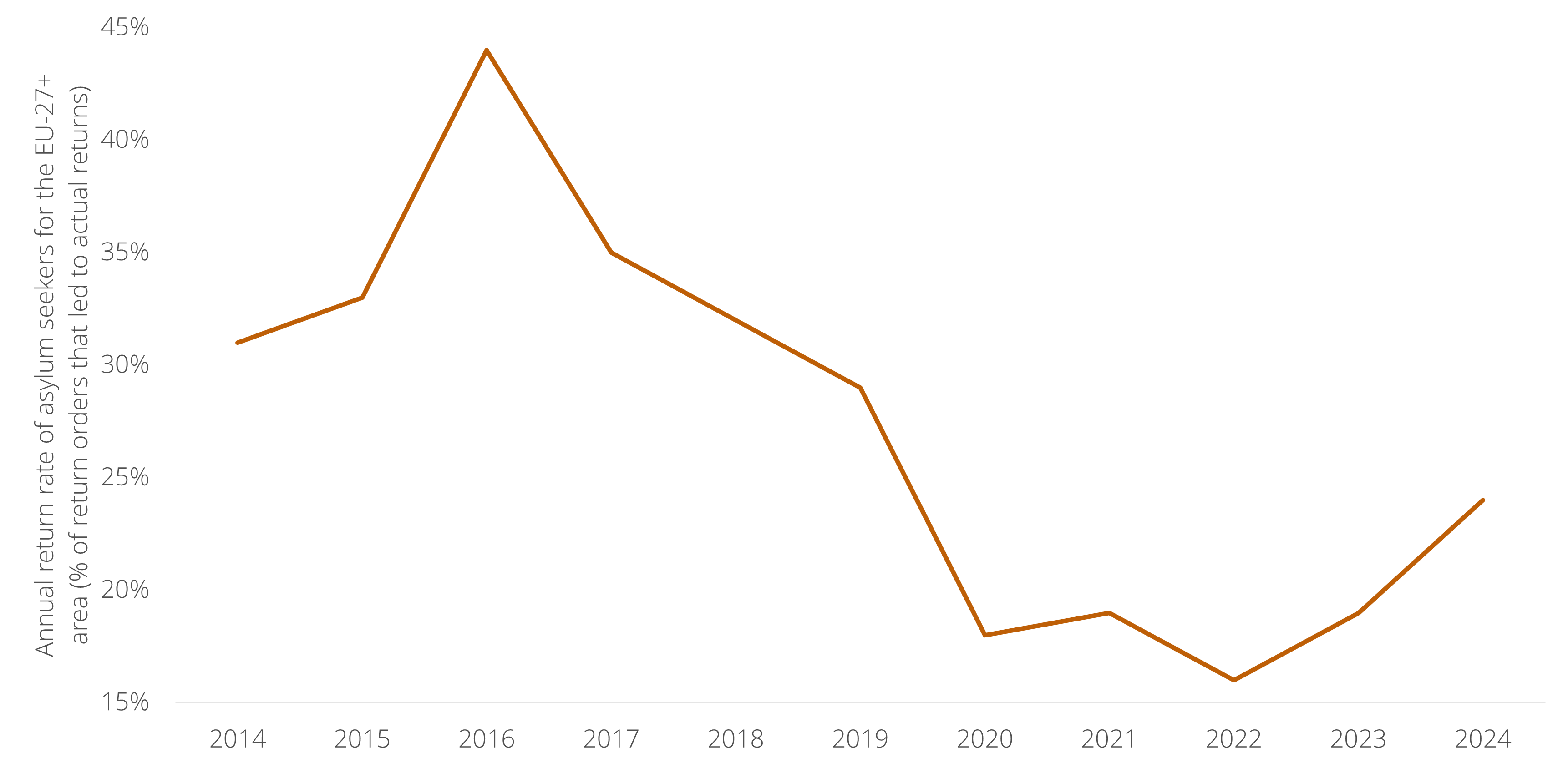

Asylum. The EU is moving forward with legislation to establish return hubs in non-EU countries for asylum seekers who have been denied entry and must be returned to their country of origin. Currently, more than 70% of those ordered to leave never actually do so. This could become the most significant asylum legislation in decades and reflects a new degree of political unity on the topic.

Capital markets union. The six largest EU economies have agreed on first principles for a capital markets union that would gradually replace national investment regimes with a single European framework. The plan is widely seen as capable of significantly improving conditions for doing business across Europe and attracting greater flows of global capital. The countries involved are pressing for urgency and want an actionable plan by the end of the year.

China. As a new trade conflict between the EU and China shows signs of escalating, Spain - known for its China-friendly approach, including welcoming Chinese investment in solar, batteries and electric vehicles - pulled back from a French-led initiative to develop European tools to restrict Chinese imports. Spain's minister for economy and trade stated that Europe should focus on engaging with Chinese authorities and remain open to Chinese investment, rather than pursuing legislation that further damages the trade relationship.

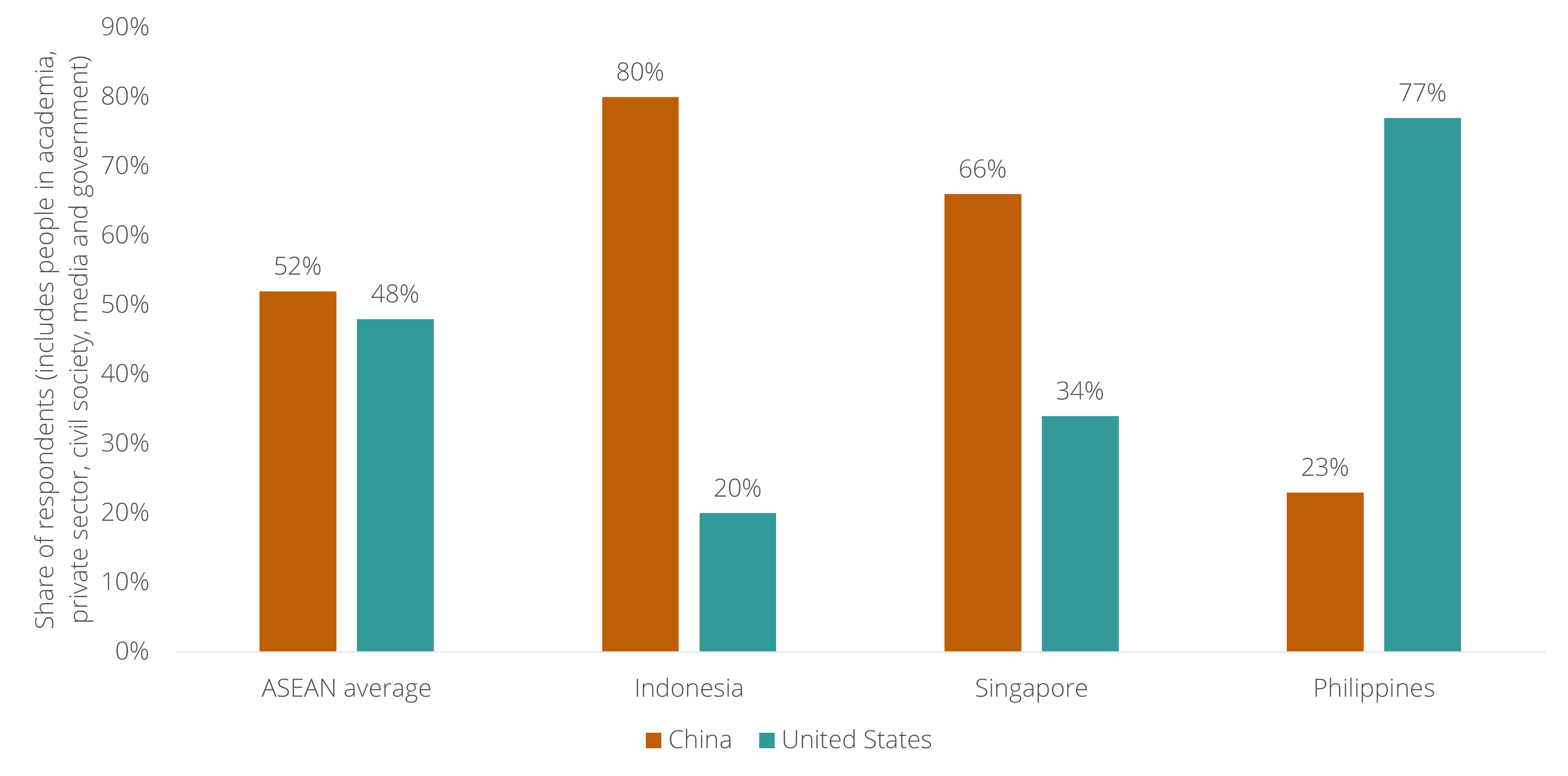

A Singaporean think-tank has found that 66% of Singaporean opinion leaders would side with China over the United States if forced to choose - a striking figure for one of Washington's closest partners in the region.

Europeans should resist filing this under "Asian story." Singapore (and ASEAN more broadly) sit in Europe's predicament: the US is their most important security partner and China is their most important trade partner – and they would rather not choose at all.

As news emerges of escalation in the trade conflict between Europe and China, it may seem naive to point to the opportunity of them working more closely together. However, we should not be surprised if that is exactly what happens in the coming years. Europe and China share a fundamental goal in the transition to clean energy, and to complete it, they need each other.

The transition to clean energy is a shared goal for Europe and China, albeit for different reasons. In China, clean energy is central to the country's economic reform plan, in which the economy transitions away from investing in real estate and infrastructure and towards high-tech manufacturing, including clean energy technologies. In Europe, besides climate targets, successive global crises have made its energy system expensive and vulnerable to disruption, necessitating a transition towards clean, local energy sources.

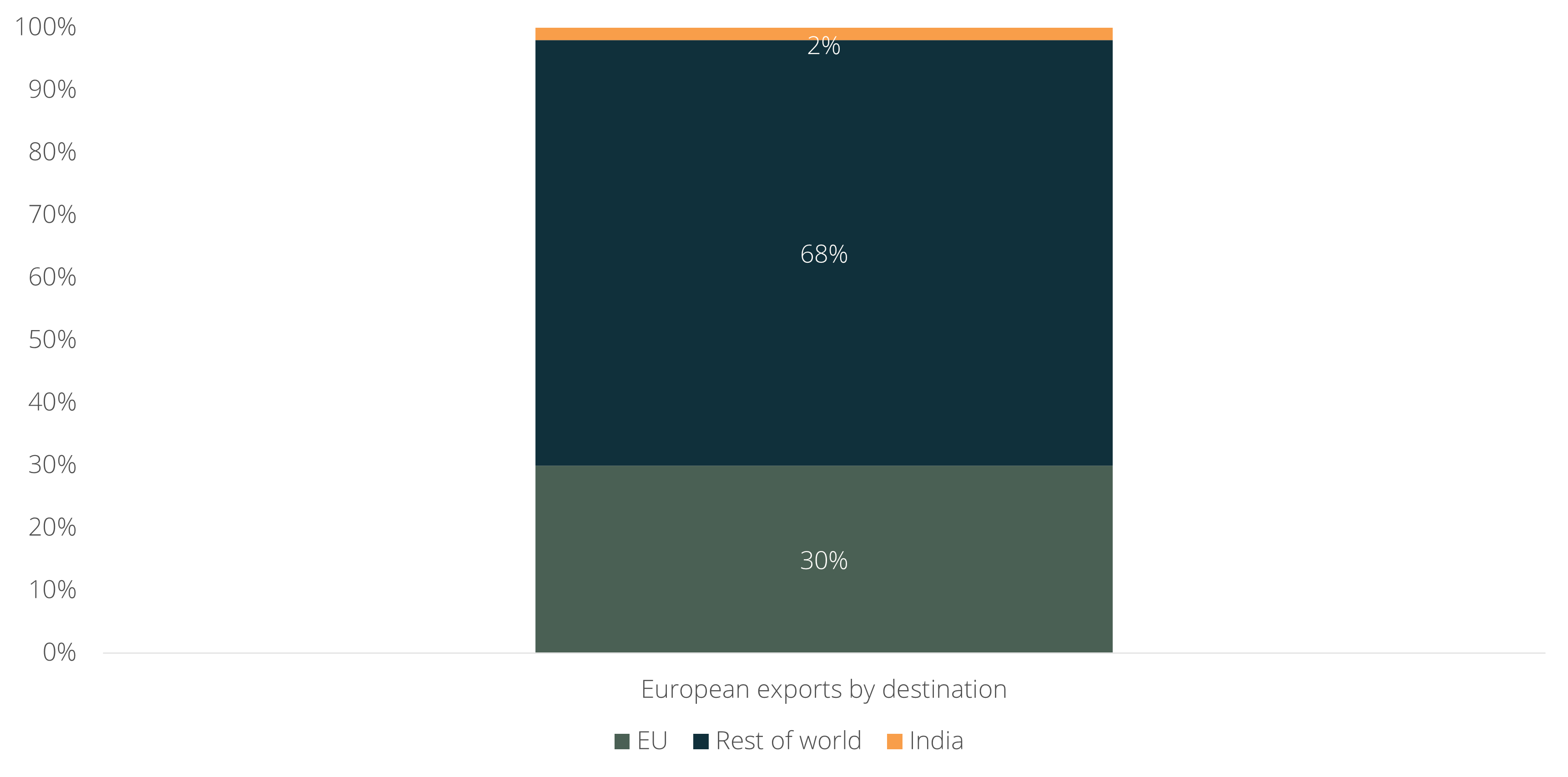

What is sometimes underappreciated is that, because of this shared goal, clean energy has already become a key driver of economic growth for both (see chart). In China, clean energy industries account for 25% of GDP growth; in Europe, more than 30%. In the US, the figure is just over 5%.

Most importantly, to complete the transition to clean energy, Europe and China need each other. Europe cannot achieve energy security without affordable Chinese technologies, and China cannot sustain its export model without reaching agreement with advanced economies like Europe on the rules for market access.

The key question is how exactly Europe and China will be able to cooperate amid conflict – driven mainly by Europe's concerns about overreliance on Chinese products – especially at a time when tensions are still escalating. The answer lies in the current energy crisis. Europe will increasingly discover that the greatest value from clean energy lies not in manufacturing these technologies (solar panels, wind turbines, heat pumps) but in deploying and integrating them with the local energy system, as this is what unlocks the potential of the broader economy. The Netherlands is a case in point: its congested electricity grid is already preventing new business formation even outside industrial production.

The main bottleneck for cooperation between Europe and China is therefore not economic competition but strategic security: Europe does not want to become overly reliant on a single country for its energy needs again. This will drive European policy towards a logic of diversification – as seen this week in the area of chemicals – rather than punishment (like the US approach of import tariffs on Chinese goods). This European approach could, like the Western quota policies on Japanese imports in the 1980s, provide the basis for diplomatic agreement.

Last month, Stanford University published research that contradicts the dominant narrative on US-China artificial intelligence (AI) competition. According to millions of human voters, the performance gap between the top US and top Chinese AI models has effectively closed (see chart).

Most importantly, Chinese firms are generating frontier AI capability at a fraction of the costs of US firms. According to Stanford, a 23-to-1 spending gap between US and Chinese private firms is producing a 2.7% performance gap. This has direct implications for US-based AI companies whose valuations rest on the assumption of a structural advantage. It also suggests the DeepSeek shock of January 2025 – when the launch of a single Chinese model briefly erased a trillion dollars from US tech stocks – was not an anomaly, but the first sign of a convergence that had been underway for several years and has continued since.

A key question in the coming years will be how Western investors can profit from China's AI capabilities. On April 27, the Chinese government cancelled Meta's $2 billion acquisition of Manus, a Singapore-based AI startup founded by Chinese engineers. Beijing is signaling that frontier AI capability is now treated as strategic territory in the same category as rare earths and semiconductors – and is therefore closing the offshore "Singapore-washing" route that Chinese tech firms have used for years to reach Western investors.

Since COVID, western societies have grown deeply dependent on government financial support during times of global crisis. The COVID response from 2020 onwards was unprecedented: the US launched the largest infrastructure investment packages in its history, while EU countries agreed for the first time to issue joint debt. The energy support packages that followed the war in Ukraine in 2022 were also significant, reaching up to 5% of GDP in some European countries. In 2026, however, as the economic impact of the war in Iran threatens to become severe, the capacity for a similar response is largely gone.

The main reason is the worsening state of government finances. Since COVID, the yields investors demand on government debt are substantially higher than six years ago. In simple terms, governments can no longer afford large-scale financial support without triggering a further rise in the yields on their debt. And rising yields, for countries already carrying high debt-to-GDP ratios, risk setting off a vicious cycle: higher borrowing costs force spending cuts, which slow growth, which worsens the debt burden, which pushes yields even higher - and so on.

A key implication is that western governments, without the ability to soften the blow of a global crisis, are losing control over the way economic pain will drive change. The early signs are already visible. In the US, the adoption of renewable energy is accelerating despite the Trump administration's efforts to protect fossil fuels, because businesses and households are discovering that renewable technology – including the Chinese-made products the administration has sought to block – offers greater price stability than oil and gas. In Europe, calls for a more stable relationship with China are growing for the same reason.

In the coming years, alternative protein (plant- and cell-based protein as a substitute for animal-based food) is likely to follow the same pattern as renewable energy technology over the past twenty years: driven by Chinese innovation, the cost falls so far that the case for transition shifts from a divisive moral ideal into a shared economic necessity.

Twenty years ago, the Chinese government made renewable energy technology a top priority for the first time in its 11th Five Year Plan (2006–2010). Today, China is the global leader in solar panels, batteries and electric vehicles. Over that period, several global crises that drove up the price of energy (the war in Ukraine, the war in the Middle East) turned renewable energy into a shared economic necessity: a more reliable energy supply at a lower cost. Something similar is now likely to happen in food, whose global prices are high and rising because of the war in the Middle East.

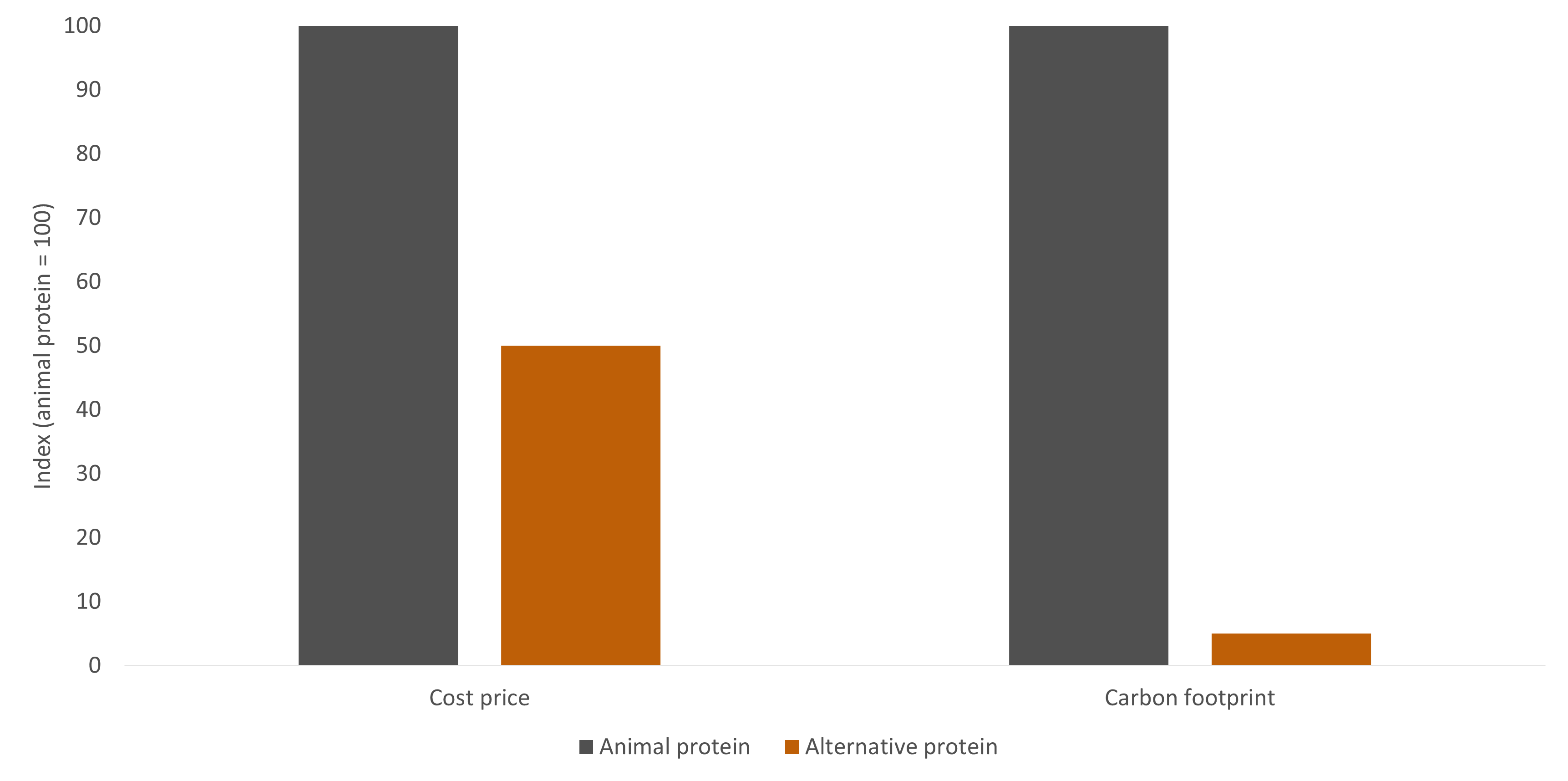

In its 15th Five Year Plan (2026–2030), the Chinese government has made alternative protein a top priority. China is already the world's largest funder of agricultural R&D, spending twice as much as the United States. The city of Shanghai has made the industrial scaling of alternative protein a key strategic objective. In November 2025, one Chinese company opened a factory the size of 75 football fields capable of producing alternative protein at 50% of the cost of animal-based protein - and with 95% lower carbon emissions.

A significant signal of financial stress in the Gulf has emerged: according to the Wall Street Journal, the governor of the UAE's central bank has opened talks with the United States about a currency swap arrangement. The stability of the UAE's currency, the dirham, depends on its peg to the US dollar, which is maintained through large dollar reserves accumulated via the UAE's trade and financial networks. Those reserves are now under pressure from two directions: maritime trade disruption and capital flight – particularly in real estate, where luxury property discounts of over 50% are being reported. Together, these forces threaten a structural decline in dollar income. This is the mechanism that triggered the 1997 Asian financial crisis: when dollar reserves backing a pegged currency erode faster than they can be replenished, a currency crisis becomes self-fulfilling.

The Gulf states are therefore in urgent need of regional stability – but looking at both the US and Iran, that appears unlikely. The US is caught between three bad options: tacitly admitting defeat and watching the Iranian regime it tried to destroy consolidate into a regional power with global influence through its control of the Strait of Hormuz; muddling through while the global economy absorbs severe shocks across multiple supply chains; or risking the consequences of further military escalation. Meanwhile, according to reporting by The New Yorker, those who now govern Iran are considerably more hardline than is widely assumed – and less inclined than their predecessors to accept a diplomatic settlement favorable to the US and Israel.

All of this carries a long-term risk for the US in its rivalry with China. In their talks with Washington, UAE officials explicitly warned that the Chinese renminbi is a serious alternative to the US dollar. This warning is credible because the Gulf states have already been building the infrastructure for such a shift. The mBridge project – a digital currency platform backed by the central banks of China, Saudi Arabia and the UAE – processed $56 billion in transactions in 2025, a 2,500-fold increase from 2022. Although mBridge operates at the level of financial transactions rather than central bank reserve holdings, this is how the dollar's network effects would weaken first in a long-term shift.

As the Hormuz crisis continues, we would be wise to remember a lesson from the COVID crisis: local shortages of specific resources can cascade into larger global problems that are difficult to predict. Global attention is currently focused on energy (rising oil and gas prices), food (higher fertilizer costs) and helium (critical for computer chip production), but a closer look reveals at least three additional supply chain disruptions that could spiral into something larger.

First, shortages of naphtha — refined from oil and used in the production of plastics, chips and cars — have triggered an industrial state of emergency across Asia. Both Japan and South Korea are attempting to calm markets, but supply chains are already being disrupted. In Japan, the prime minister intervened to quell online rumors of an imminent shortage after several plastic producers announced production cuts affecting sectors as diverse as food and healthcare. South Korea has banned naphtha exports to protect domestic medical procedures and has reluctantly begun sourcing the material from Russia.

Second, Australia — heavily dependent on diesel — faces rising prices and emerging shortages that threaten to shut down both farming and mining operations. As an emergency measure, several tankers carrying diesel have been sent from the US, a journey that takes up to three months, underscoring the severity of the situation. This matters globally: Australia is one of the world's largest producers of minerals like iron ore, lithium and nickel.

Third, Europe is on course to run out of kerosene within three weeks. While an aviation disruption may appear less urgent than food or mining, it would indirectly affect a wide range of businesses and economies through the collapse of tourism.

Each of these shortages may seem secondary to the broader disruption of energy, food and chip production. But together they threaten industries as diverse as healthcare, mining and tourism — and could push the global economy into territory that is difficult to predict.

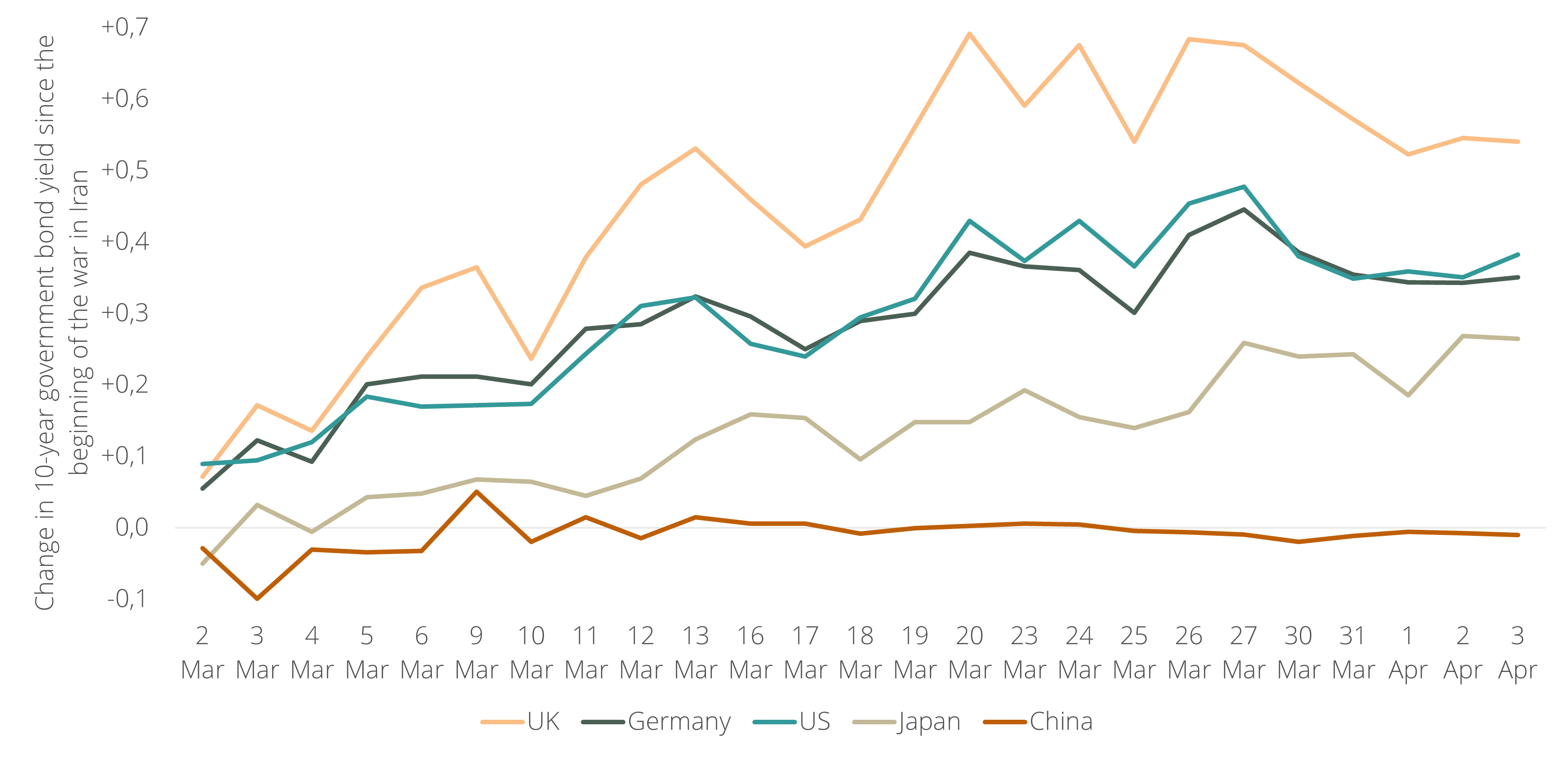

In every global crisis of our generation — the 2001 dot-com crash, the 2008 financial crisis, the 2020 COVID crisis — global investors sought safety in US Treasuries, placing capital in the 10-year US government bond. The 2026 war in Iran has broken that pattern. For the first time in a global crisis, China's government bonds are the only safe haven, holding their value while US Treasuries, other government bonds, and even gold have sold off. Meanwhile, equity markets in China have also lost less value than their counterparts in the US, Europe and Japan.

This is happening despite investors' well-documented reservations about Chinese assets — political risk, capital controls, and the difficulty of converting renminbi into dollars, euros, or yen. That is because, as we have written in the past year, China's safe haven status is part of a larger shift: trust in US stability is declining, while China is no longer seen as uninvestable, leads in technological innovation, sets global standards, has soft power and is better prepared for an era of prolonged global conflict.

Ironically, while the US is locked in a global struggle for influence with China, it is China that was better prepared for the war in Iran — the war the US itself started. China's energy system is more resilient against a prolonged conflict in the Middle East, its businesses are the main beneficiaries of the conflict, and the conflict is improving China's reputation as a more stable international partner for trade and investment than the US.

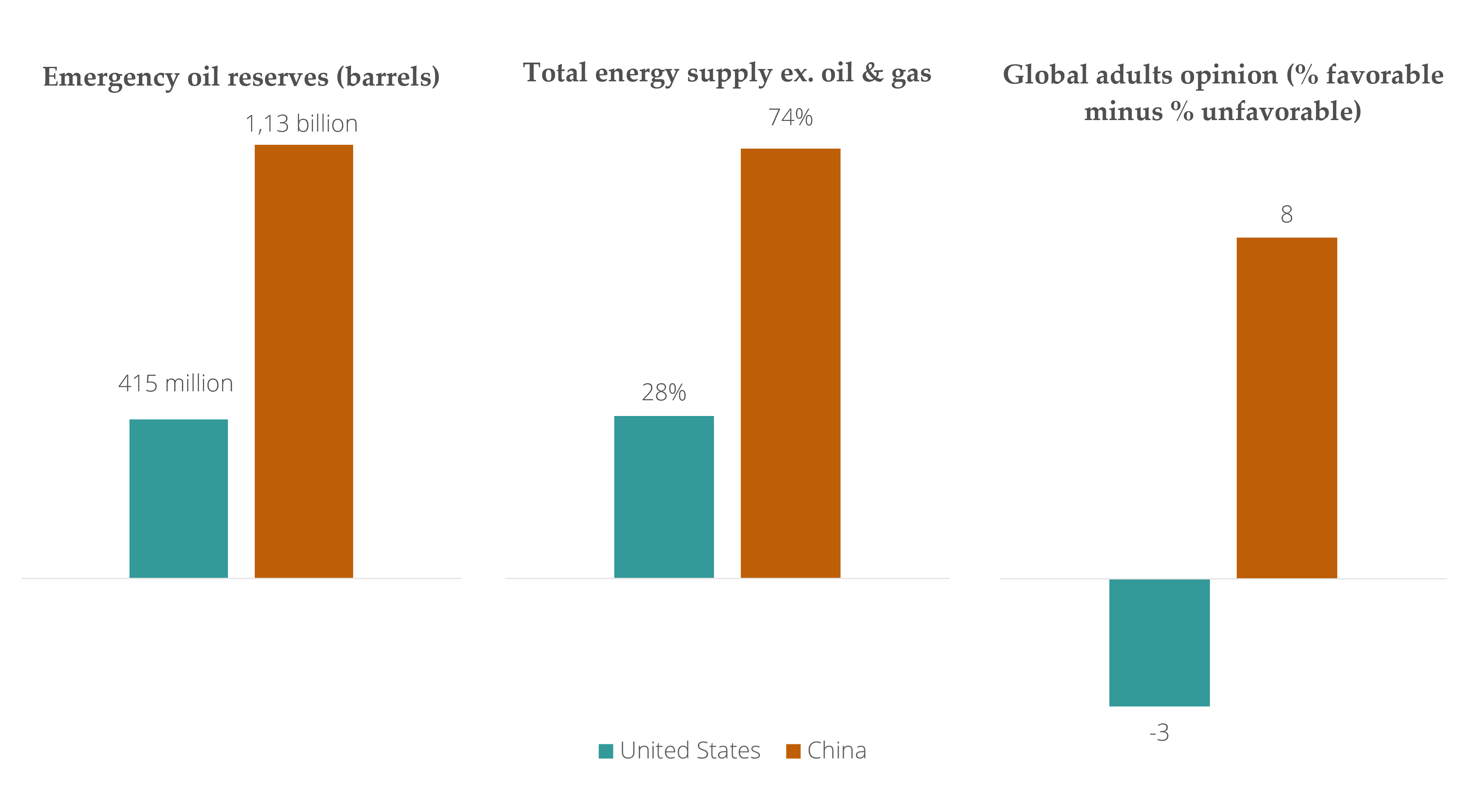

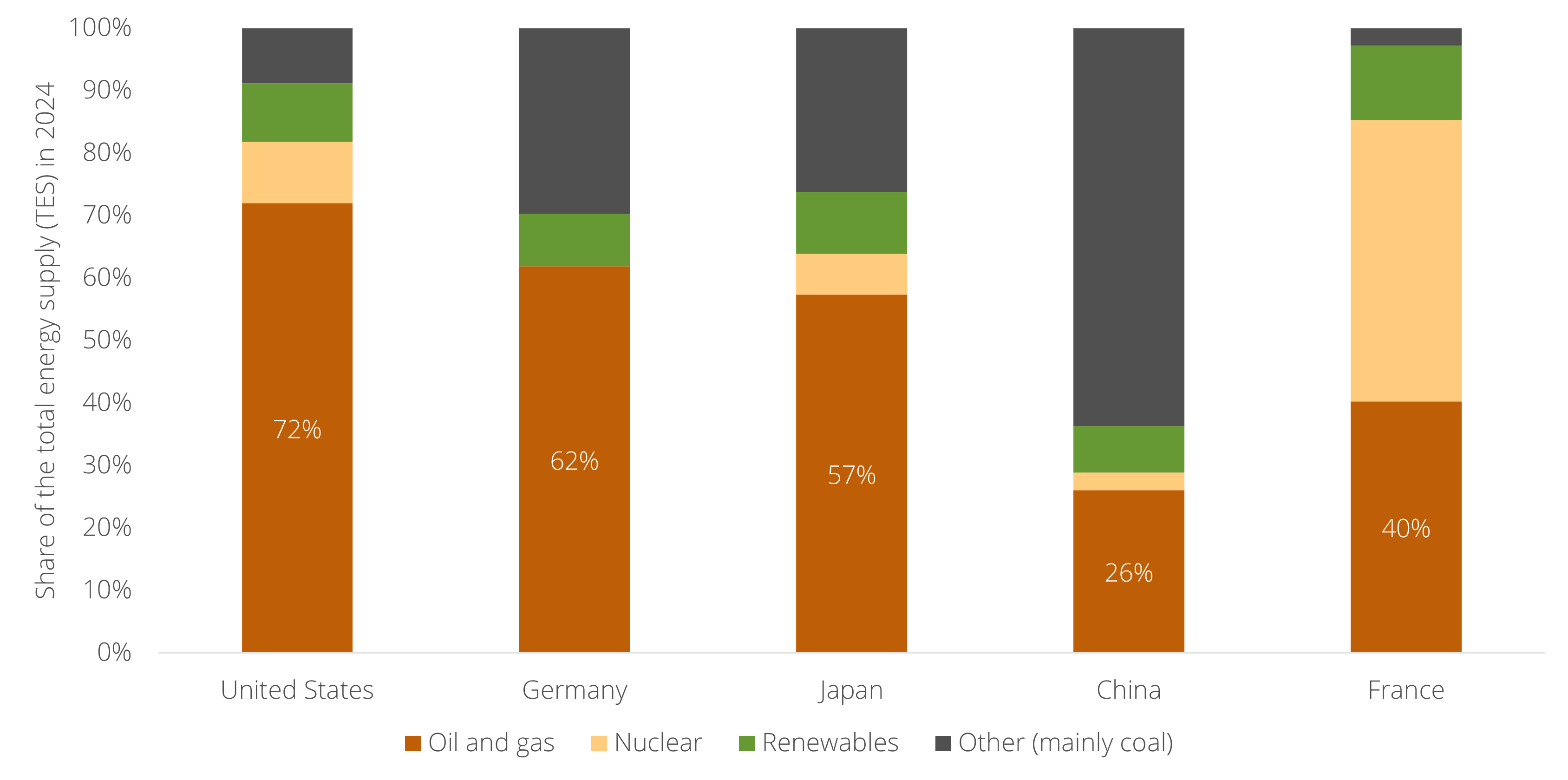

First, China's economy is more resilient to a prolonged conflict in the Middle East than any other major economy. The main reason is the structure of its energy system. As we wrote several weeks ago, China's vision of energy security — a mix of nuclear and renewables, with coal serving as a bridge — is more resilient than the US system, in which oil and gas account for 72% of total energy supply. China also reportedly holds twice as many emergency oil reserves: 1.13 billion barrels compared to 415 million for the US.

Second, China's businesses are the leading producers of the technologies that benefit most from this conflict. In many countries, yet another international conflict driving up oil and gas prices has sparked renewed demand for renewable energy technologies such as solar panels, heat pumps, and batteries — all industries in which China is the world leader. Electric vehicles, another area of Chinese dominance, are also gaining in popularity as a result.

Third, under the second Trump administration, China is rapidly becoming a more stable and predictable international partner than the US. European leaders were already working to improve relations with Beijing before this conflict began. Global investors, meanwhile, are increasingly viewing Chinese government bonds as a relatively stable safe haven. Notably, Iran is reportedly demanding payment in Chinese renminbi from ships seeking passage through the Strait of Hormuz.

Most importantly, even if the US manages to prevent a full economic collapse in the coming weeks — as we warned last week remains a real risk — the dynamic described above is unlikely to reverse. In all three dimensions, this conflict is likely to remain a positive force for China's long-term development.

The US president just announced a 5-day halt to strikes on Iran’s energy infrastructure. This most likely signals that Washington recognizes what further escalation of this conflict would cost. Everything now depends on the US finding a solution in just a few weeks – one that almost certainly means leaving the Iranian regime intact, despite regime change having been an explicit American objective from the start. It is urgent because the global economic pain is already materializing in at least three distinct but interconnected layers.

1. Energy, inflation and debt

Higher energy prices feed directly into inflation expectations – and therefore into the interest rates set by central banks and demanded by fixed-income investors. Recently, these higher interest rates have already exposed deep liquidity stress in private markets, which threatens to spill over into institutions who hold these assets – like pension funds. This alone could be a sufficient reason for the US to find a way to stop the conflict.

2. The AI boom's hidden supply chain

Less visible but equally significant is the threat to the inputs that power the artificial intelligence boom. Data centers and the computer chips that run them depend not only on cheap energy, but also on a set of industrial chemicals (like helium, sulphur and bromine) that are mainly sourced from the Middle East and are now caught in a disrupted supply chain. Since it was the AI boom that drove the majority of US stock market growth over the past three years, a sustained conflict puts that growth engine under direct threat.

3. The wealth effect and the American economy

The third layer is the large share of US consumer spending – the largest single driver of the US economy – that comes from high-income Americans, whose consumption is tied to the value of their investment portfolios. A sustained stock market decline, amplified by Gulf sovereign wealth funds pulling capital from US markets, could trigger a meaningful pullback in that spending, which could throw the American economy into a vicious downward spiral.

A narrow window for diplomacy

The current situation is straightforward: three simultaneous shocks – to energy prices, to critical technology supply chains, and to the wealth effect underpinning US consumption – arriving together would strain the global economy in ways that no single policy can easily offset. Without a genuine diplomatic breakthrough in the coming weeks, the world could be facing an economic crisis that rivals anything seen in a generation.

If we zoom out beyond the immediate crisis in the Strait of Hormuz, a larger pattern becomes visible that has been building for years: global capital is increasingly looking beyond the United States.

In the past few years, global investors have repeatedly confronted a question that once seemed unthinkable: whether US government bonds still deserve their status as the world's safest asset. It began in 2020–22, when pandemic-era government spending in the US pushed its budget deficit to a record high. The inflation that followed drove up interest rates and pushed down US government bond values – the assets that global investors relied on to protect their portfolios when other markets fall. In 2024–25, President Trump's attacks on central bank independence and his extreme import tariffs reinforced the same dynamic. In 2026, US military escalations against Iran, Venezuela and Greenland have brought some foreign investors to the point of considering shedding US assets altogether.

Two signals have emerged in 2026 that confirm this narrative.

The first comes from the Gulf. Against the background of Iranian officials stating that any institution buying US government bonds is financing the war, Gulf sovereign wealth funds, which hold trillions in US assets, have reportedly been in dialogue about cutting back their investment commitments to the United States, to bring capital back home.

The second comes from Europe. Since the Greenland crisis, more institutional investors are actively choosing European government bonds over American ones. This is not a rotation driven by the expectation of higher returns. It is a repricing of trust: a slow but accelerating loss of confidence in the reliability of the United States that has been building for many years.

As the war in the Middle East continues to push up prices for oil and gas, two countries find themselves relatively well positioned – because they have been preparing for this scenario for decades: France and China. Both have pursued energy security through a mix centered on nuclear power and renewables, reducing their structural dependence on imported oil and gas.

For France, the vision dates to the 1973 oil crisis. Before it, France imported around 75% of its energy and had almost no domestic fossil fuel resources of its own. The response was the Messmer Plan of 1974 – a state-directed mobilization to build out nuclear capacity at a scale that remains unmatched in the Western world. Fifty years later, that bet is paying off.

In China, decades of industrial policy have been shaped by a refusal to become dependent on imported oil and gas – a vulnerability that Chinese planners call the "Malacca Dilemma": the risk that foreign powers could strangle Chinese energy supply by blocking maritime routes (like the Strait of Malacca, or currently, the Strait of Hormuz). Coal, despite its pollution, remains China's dominant energy source today, but explicitly as a bridge, not a destination. The destination is a mix of nuclear and renewables on a scale the world has never seen: more than half of all nuclear reactors currently under construction are in China, and China installs more solar capacity each year than the rest of the world combined.

The irony is that two very different political systems arrived at the same conclusion through the same logic: that the energy mix of nuclear and renewables is not merely relatively good for the environment, but offers energy security for the nation.

Most people expect the war in Iran to end within days or weeks - much like the predictions surrounding Ukraine in February 2022. But a weak regime does not guarantee a short war. It merely means a more unpredictable outcome.

As we wrote in January, the weakening of the Iranian regime has opened a contest for control of the region. Israel, Turkey, Saudi Arabia, the United Arab Emirates, and Qatar are all vying for influence - and none of them want the same outcome in this war. Israel and Turkey were already at odds: former Prime Minister Naftali Bennett publicly framed Turkey as a threat on par with Iran. Now Israel is at odds with the Gulf states, whose entire economic model depends on the war ending immediately.

For decades, the Gulf states built their global standing on a single promise: whatever happens in the Middle East, the Gulf remains stable. That promise has now been broken. Missiles have struck Dubai's airport and hotels and killed civilians in Abu Dhabi. Thousands of travelers are stranded across the region - unable to fly home or forced to pay a massive premium to flee via Riyadh. Within days, the Gulf's reputation as a safe haven is already in serious doubt.

The most common critique of China’s innovation goes like this:

"Sure, China leads in solar panels and batteries – but those were invented elsewhere. And research dominance doesn't mean commercial success.“

It seems like a reasonable critique, but the data doesn't support it.

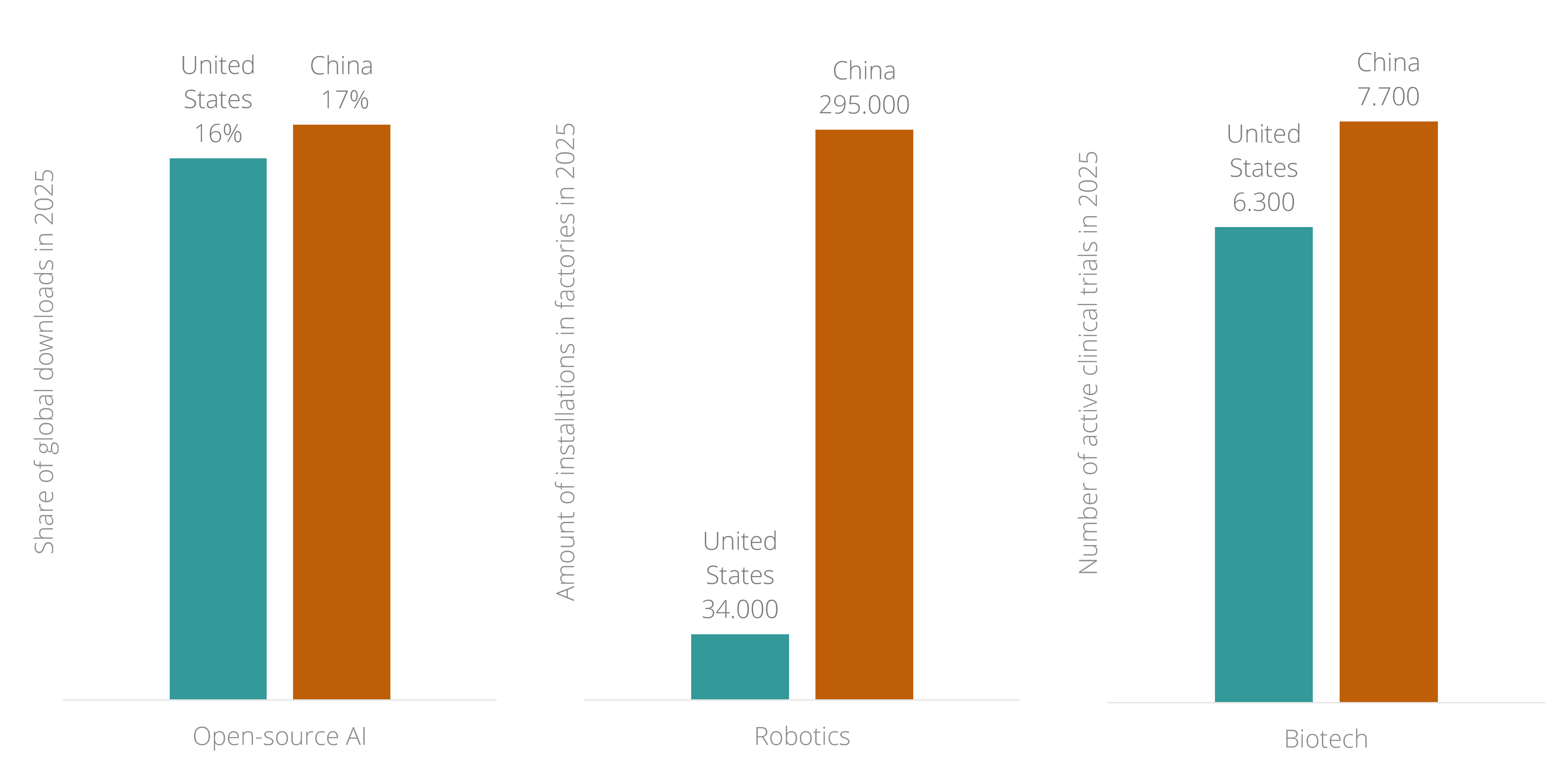

China now leads the US in open-source AI downloads (17% vs 16% globally). It has 8x more industrial robots installed in factories. And it's running more active clinical trials in biotech than the US.

These aren't legacy industries or lab metrics. They're consumer products, factory floors, and drug pipelines.

The question is not whether China is catching up, but whether the West has a good plan for a world where China is leading.

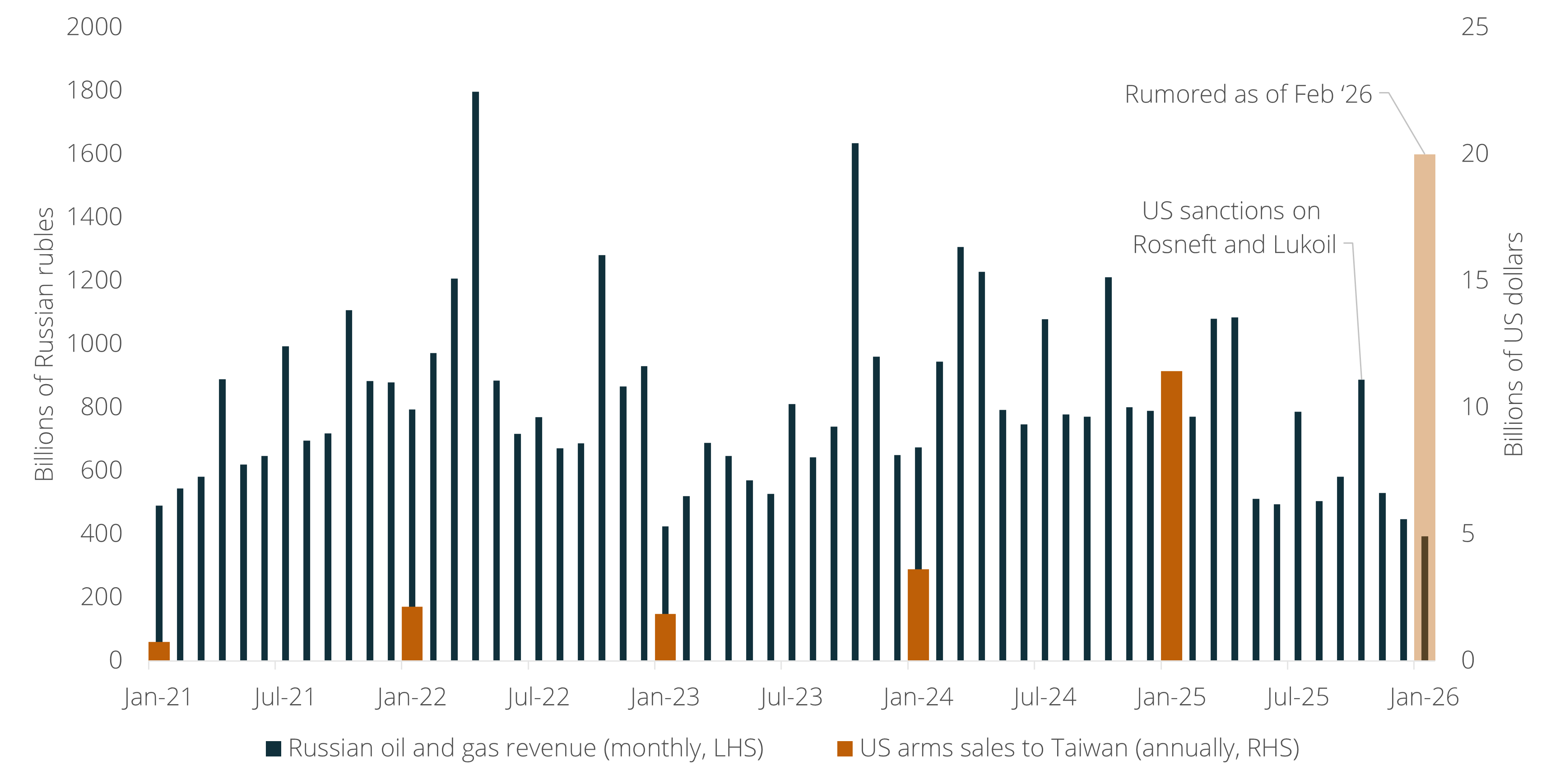

The second Trump presidency has fueled a widespread belief in Europe that Washington has gone soft on China and Russia. But the data tells a different story. US arms sales to Taiwan have accelerated dramatically from a record $11 billion in 2025 to a rumored $20 billion package for 2026. Meanwhile, US sanctions on Russia's two largest oil companies, Rosneft and Lukoil, triggered in October 2025 a collapse in Russian energy revenue to its lowest point in five years, directly threatening the stability of Moscow's war economy.

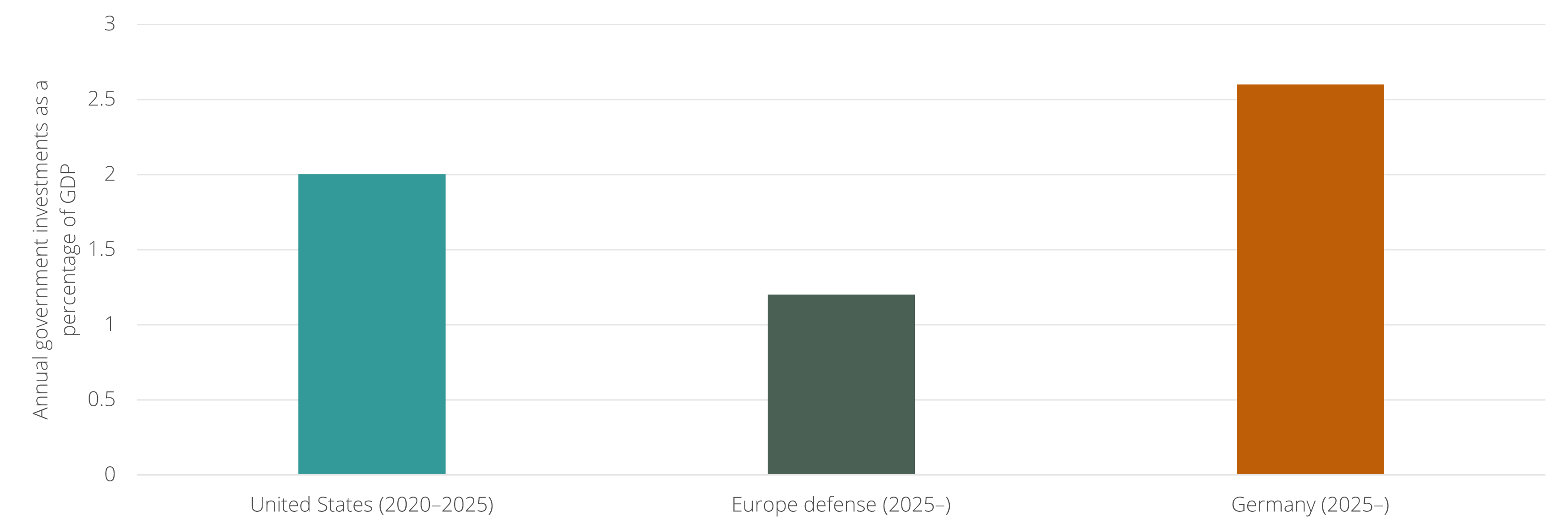

After many years of mainly talk, the EU has grown more ambitious in the past two years, and this trend is accelerating in 2026. Last year, Europe's ambition was driven by an 800 billion euro defense investment plan, in addition to Germany rewriting its constitution to enable bigger government investments. But Europe's two most ambitious projects in 2026 are more structural than these spending programs. First, a trade deal with India - now the world's fourth-largest economy but trading little with Europe - that could open a massive market for European industry. Second, the Industrial Accelerator Act, which will introduce "Buy European" legislation directing EU procurement toward EU suppliers. The biggest challenge remains that some member states oppose projects that lower trade barriers (such as France), whereas others oppose projects that raise them (such as the Netherlands). However, given the current momentum in Europe and the highly uncertain geopolitical situation, the probability that both projects advance is significant. If they do, this could contribute to European stock markets' continued outperformance versus the US, as in 2025.

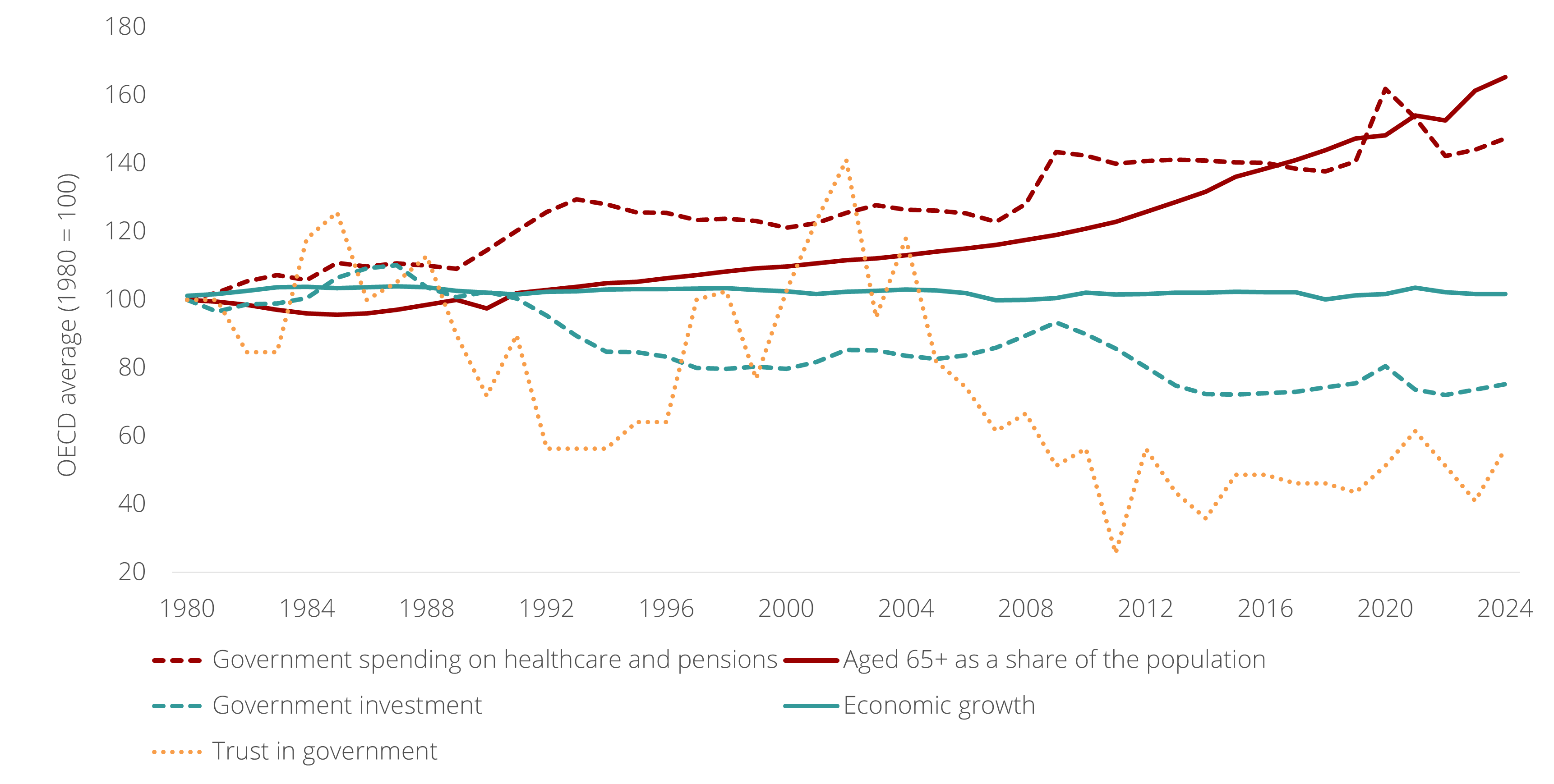

The extreme volatility in metals markets (in recent days, the price of silver has fallen by nearly 30%) reflects a deep structural problem in Western societies. In recent years, investors have increasingly allocated capital to gold and silver as hedges against the inflation of government-issued currencies – commonly referred to as the “debasement trade.” Behind this investment strategy lies the demographic reality of aging populations. Over the past 50 years, governments have steadily redirected spending toward healthcare and pensions for a growing elderly population, crowding out long-term investment and pushing down economic growth. This has led to record levels of government debt and a greater reliance on inflation as the means of reducing the burden of debt over time. This precarious economy of rising prices, particularly in basic needs such as housing and groceries, has produced a fragile political system defined by the rise of populism.

Because all of this is rooted in demographics, it is likely to persist. Recent policy shifts in the United States and Europe signal an attempt to confront this reality by cutting healthcare and pension commitments, but such measures do not address the underlying problem and are likely to intensify political unrest.

The deeper issue is that governments lack a strategy capable of offsetting the reality of aging populations. One possible exception is China. With a limited tax base to finance its own demographic decline, Beijing has been forced into a more radical response: restructuring its economy toward innovation, including in healthcare itself.

At the start of 2026, just as the United States’ confrontation with other countries threatens global stability, its withdrawal from other regions is also fueling conflict, particularly in the Middle East. The region’s dynamics have shifted fundamentally in the past few years: as the United States retreats, the most powerful country in the region, Iran, has been weakened by its war with Israel following the Hamas attack of October 7, 2023. The result is an open contest for control of the region among five countries: Israel, Turkey, Saudi Arabia, the United Arab Emirates, and Qatar. In April 2025, Israel bombed designated sites for three Turkish military bases in Syria, while Saudi Arabia and the United Arab Emirates - until recently longstanding allies - have engaged in proxy conflicts in Yemen, Sudan, Libya, and Somaliland. Looking ahead, it is Saudi Arabia that appears most at risk of triggering a destabilizing scenario, as its future is increasingly threatened by shifting dynamics in the global oil market on which it so heavily depends, driven by rising US production and the prospect of Venezuela, and possibly Iran, regaining access to global oil markets.

As the Western world awaits United States President Trump’s speech in Davos amid an escalating conflict between the US and Europe over the status of Greenland, the prime minister of Canada has returned from China after announcing a “new world order” in which Canada will deepen its relationship with Beijing. This Canadian vision is part of a broader shift across the West: in 2025, Spain joined Hungary in welcoming Chinese producers of batteries and electric vehicles to the European continent, and in the coming weeks the leaders of both the United Kingdom and Germany will visit China in what will likely crystallize into a shared narrative.

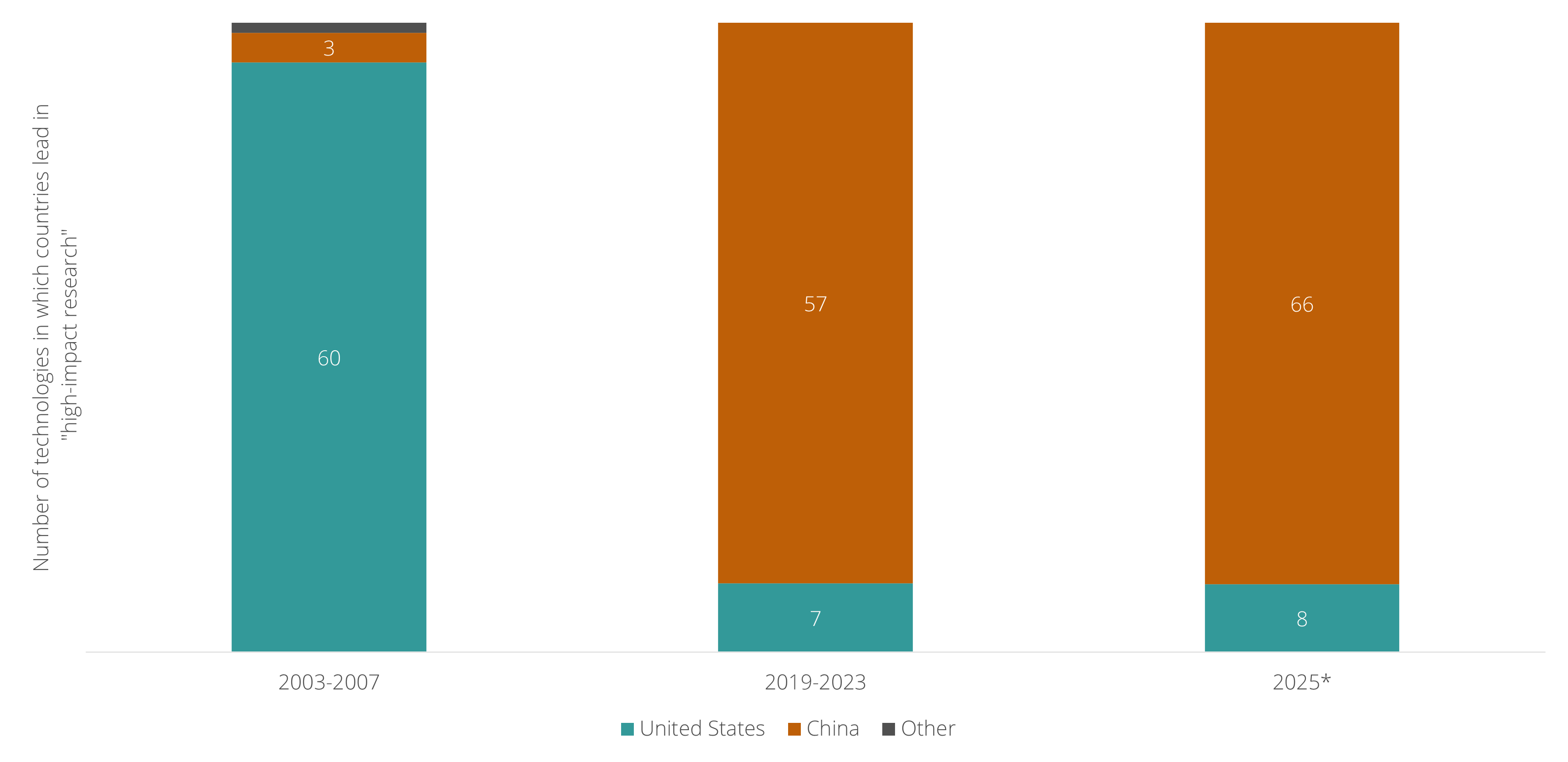

As China is increasingly seen as a more reliable partner than the United States by many nations, it is also overtaking the US in technological innovation. In the latest update of the Australian Strategic Policy Institute’s (ASPI) tracker of 74 “critical technologies,” the US leads in just 8, while China leads in 66. Notably, China has recently surpassed the US in the global share of downloads for open-source artificial intelligence models, which are released for free and can run on local cloud providers rather than US- or China-based ones. China’s growing lead in AI is underpinned by its massive advantage in electricity generation: by 2030, its surplus power is projected to be three times larger than the entire world’s electricity demand for data centers. This is also giving rise to entire industries that remain largely unknown in the Western world, such as the “low-altitude economy” (Chinese food-delivery firm Meituan has completed more than 600,000 orders via drones in China).

In 2026, this global shift could shock US financial markets, much as the launch of an AI model by the Chinese firm DeepSeek triggered a panic in January 2025.

What is currently being underestimated is the likelihood that US president Trump, after several high-risk strategic successes (Iran, Venezuela), overplays his hand and makes a mistake similar to Putin’s invasion of Ukraine, which was intended as a quick operation but has turned into a four-year war. If the US were to force Denmark to relinquish control of Greenland, this could become the catalyst for what Europe is currently trying to talk into existence: a new European defense architecture that would effectively replace NATO. If the US were to target Canada, most likely by supporting a secessionist movement in provinces such as Alberta or Quebec, this could spark a nationalist movement to defend Canada, similar to Ukraine’s response to Russian aggression. Besides this, in both scenarios, pressure on the US dollar could intensify, as many Western investors would be incentivized to reduce their dollar holdings. Since 2020, the US dollar has already experienced declining exposure among central banks. If this trend were to accelerate, it could destabilize the US economy through upward pressure on interest rates.

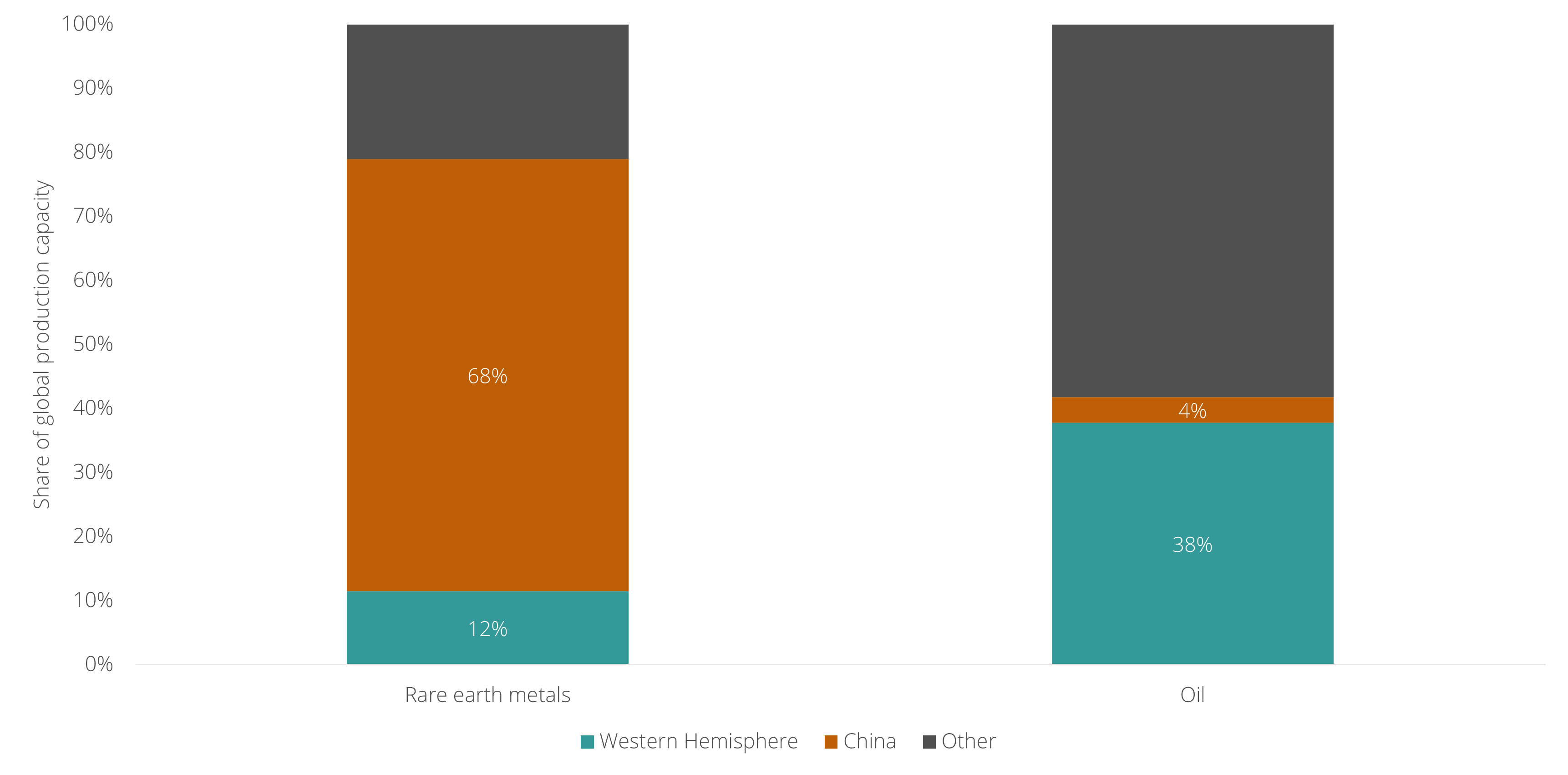

The capture of Venezuelan president Nicolás Maduro by the United States military has shown that Washington is moving decisively to consolidate control over the Western Hemisphere. What remains underappreciated, however, is that by asserting control over these countries, the US would effectively control around 40% of global oil production capacity. This would give the US, for the first time in history, a high degree of influence on global oil prices. Whereas the 1973 oil crisis, driven by Arab producers, once destabilized the US economy, Washington could soon wield comparable leverage over others while keeping energy prices relatively low at home. This strategy thus functions as a structural counterweight to China, which imports roughly 75% of its oil needs but dominates global rare earth metals production capacity. In effect, the US and China are dividing control of the world’s key inputs of economic and military power.

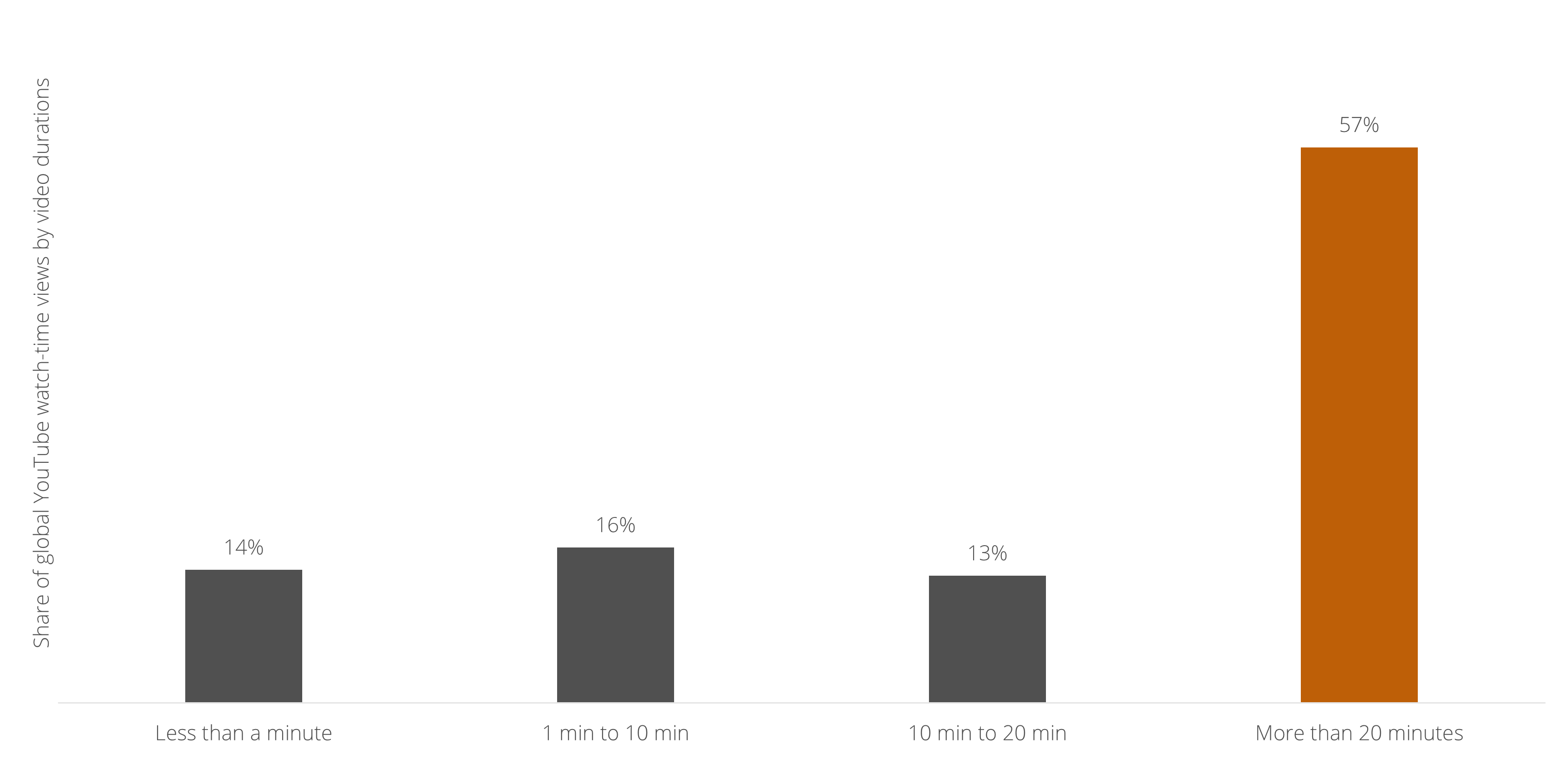

The popularity of media platforms like TikTok, Instagram, and YouTube gave rise to the phenomenon of “doomscrolling,” an activity in which users spend excessive amounts of time ‘mindlessly’ scrolling through short videos, reinforcing the widespread belief that especially young people are addicted to this form of entertainment. Yet the data tells a different story. Although YouTube Shorts of up to three minutes account for around 75% of total views on the platform, more than half of the time spent on YouTube is devoted to videos longer than 20 minutes. At the same time, short-form content is becoming longer: Instagram now allows videos of up to three minutes, and TikTok even permits uploads of up to one hour. The rebirth of long-form video content suggests that young people are not excessively distracted by or addicted to short videos, but are increasingly pushing back against them and seeking longer, more immersive media experiences.

In 2020-21, a wave of unexpected regulations by the Chinese government targeting several sectors, including real estate, private education, and fintech, combined with rising international tensions surrounding the COVID pandemic, led Western financial markets to label China as “uninvestable.” Less than five years later, that consensus has already collapsed. In 2025, Chinese equities rank among the world’s best performing markets. More specifically, China’s power companies are emerging as global leaders underpinning AI investment, with CATL’s batteries becoming the standard even for American data centers. Finally, just weeks ago, China issued government bonds in both US dollars and euros, and demand from Western investors exceeded supply by a factor of 25 to 30, highlighting the growing willingness of Western investors to increase their exposure to Chinese assets.

The uproar in Europe over the United States’ new national security strategy, which pledges support for European parties resisting the EU’s supranational power, misses a simple fact: these parties, such as Germany’s AfD and France’s National Rally, are already at the height of their influence, shaping the EU’s agenda from within. Just last month, a united front of right-wing parties in the European Parliament, from "extreme" to moderate, voted to weaken environmental regulations, exempting 80% of companies from the EU’s corporate sustainability reporting rules. More recently, the EU agreed to allow member states to establish asylum processing centers in non-EU countries. In short, even without US meddling, Europe is already drifting away from supranational rulemaking by the EU and toward greater national sovereignty.

When Bitcoin launched in 2009, it was designed as a form of money that could not be devalued by governments through inflation – unlike dollars and euros that can be created by central banks. Gold has historically served a similar role as a hedge against the eroding value of government-backed currencies, which is why bitcoin enthusiasts have long called it "digital gold". Yet comparing the price development of gold and bitcoin shows a stark contrast: while gold's value is relatively stable, bitcoin has become an extremely volatile asset over the past 17 years, suggesting it does not function as originally intended. A new study indicates that bitcoin also plays a different role. For a growing number of people, cryptocurrency has become a lottery ticket to homeownership. The research shows that among homeowners, crypto ownership rises gradually with wealth, but among renters it is highest among those with the lowest wealth – pointing to a "gambling for redemption" motive: risk-taking as a last resort to become a homeowner.

In today’s great-power conflict, many observers cast China as almost a mirror image of the Soviet Union, shaping the narrative that we are living through a “Second Cold War.” Yet one crucial difference between the Soviet Union then and China now is almost never acknowledged: China enjoys a far more favorable image among Western publics than the Soviet Union ever did. Throughout the Cold War, positive views of the USSR rarely exceeded 20% in Europe, whereas in 2025 favorability toward China in some European countries is approaching 50%. A shift is especially pronounced among younger generations, with major social media influencers such as Hasan Piker and IShowSpeed traveling to China in 2025 and telling a positive story about China to their tens of millions of followers – despite accusations of propaganda – focused on China's cutting-edge innovation in robotics and vehicles.

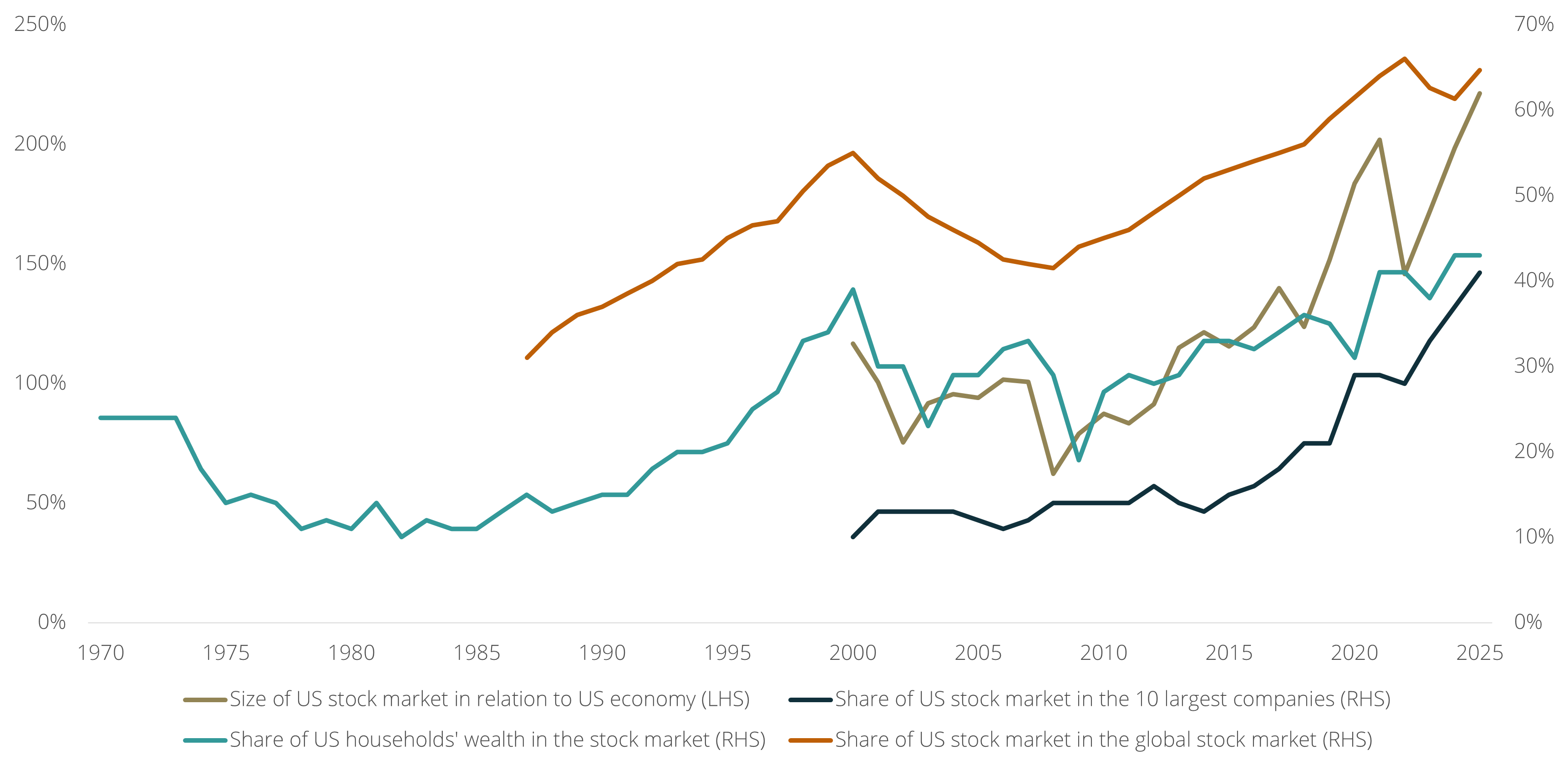

There has been a lot of discussion in recent weeks about the financial markets’ concentration in AI-related companies, with the question whether AI can fulfill its promise at the center of the debate. However, the concentration in AI is only one of five elements in a much bigger and more extreme concentration in the global financial system, reflecting how vulnerable the system has become in the past few years. First, the share of the US stock market as a percentage of the global stock market is at a record high (65%), making many investors, including pension funds, extremely sensitive to a correction in the US stock market. Second, the size of the US stock market relative to the size of the US economy is also at a record high (221%), suggesting that much of the recent growth is based on financial speculation rather than ‘real’ economic value. Third, the share of the top 10 companies in the US stock market is at a record high (41%), indicating that the rest of the economy is growing at a much slower pace (without investments by AI-related companies, the US economy was in recession in 2025). Fourth, US households have never been more invested in the stock market (43% of their wealth), implying that a correction would hit households’ finances relatively hard. Finally, the top 10% of US households (measured by income) own around 90% of the US stock market (a record high) and account for 34% of US consumption (also a record high), suggesting that a market downturn could slow consumer spending and trigger a recession—an unprecedented scenario, as historically it is usually the recession that triggers the market downturn, not the other way around.

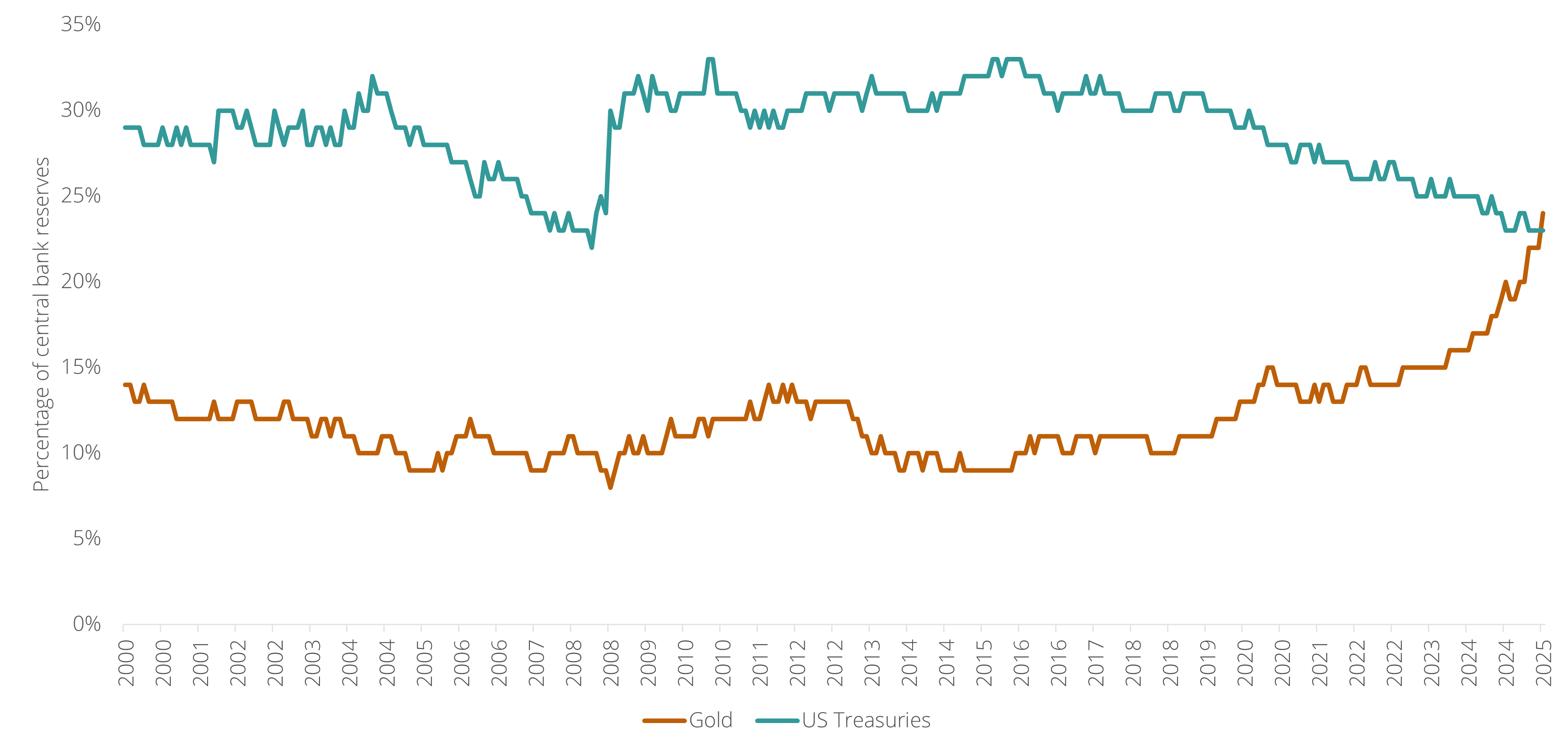

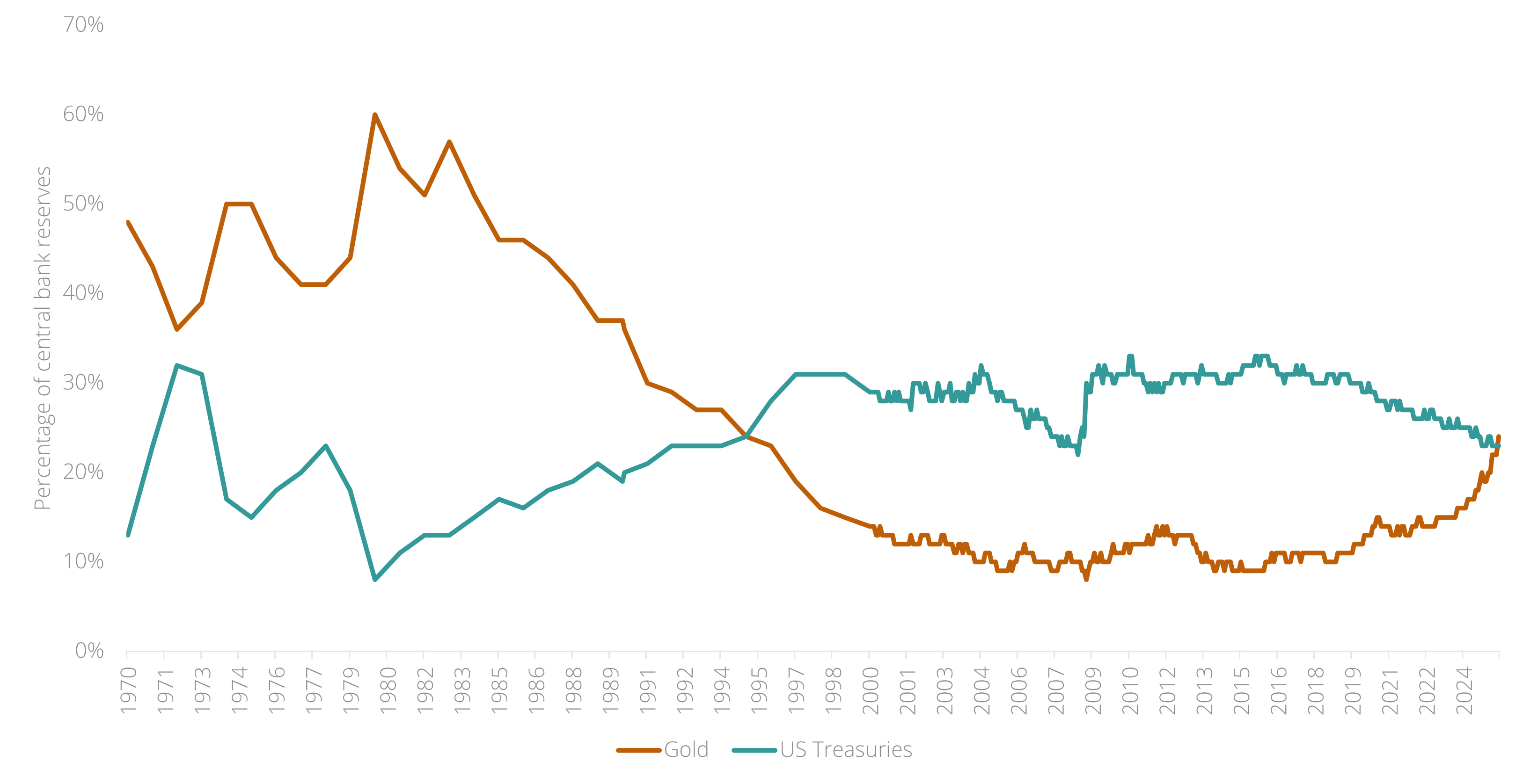

Since this year, central banks hold more gold than US Treasury bonds for the first time since 1996. This trend is driven by two mechanisms. The first is a new type of US foreign policy: as the US seeks to reshape the world order through escalating international conflicts, gold serves as a safer asset compared to US dollars, especially for foreign central banks. Last week, The Financial Times reported that the Chinese central bank may have purchased up to ten times more gold in recent years than official figures suggest. The second mechanism is the fear of a “debasement” of the US dollar, a scenario in which the United States tolerates a higher level of inflation to deflate its large government debt. This fear grows as long as the US president pressures the Federal Reserve to cut interest rates while inflation remains unstable. In the period after 1945, such monetary debasement accounted for at least half of the reduction in government debt in many Western countries, particularly the United States, the United Kingdom, and France.

Amid the focus on Europe’s new defense projects, Germany’s own investment plans have received surprisingly little attention. By removing its budget deficit limit in March of this year, Germany opened the door for government spending that rivals some of history’s largest investment projects. It is set to far exceed the Marshall Plan to rebuild Europe after 1945 and come close to the spending for Germany’s reunification after 1990. It is also expected to surpass US government spending since 2020 (relative to their domestic GDP), which significantly boosted the American stock market over the past five years. Recent reports suggest that nearly 90% of Germany’s investments will flow directly to German companies—a move that could put Berlin at odds with the EU.

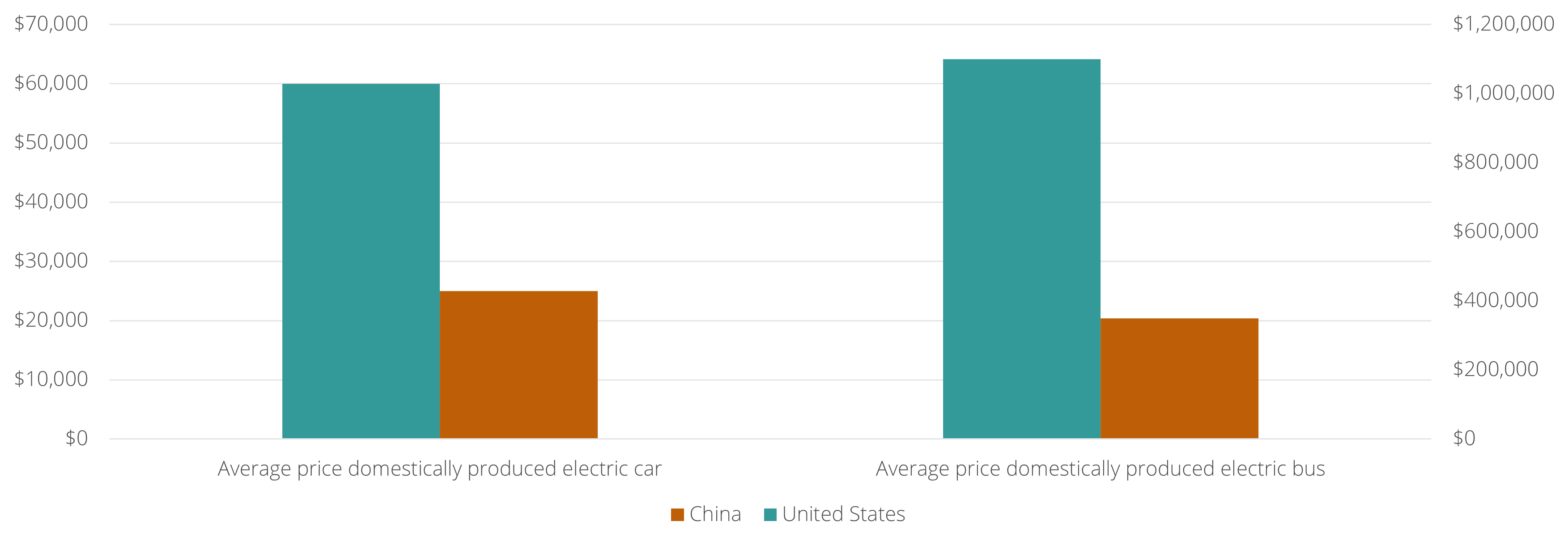

The debate around import tariffs often centers on their short-term impact on inflation. But the long-term impact receives far less attention. As the United States and Europe raise trade barriers against Chinese technology, their populations miss out on large cost advantages. Today, domestically-produced electric cars and -buses from the United States can cost up to three times more than their Chinese equivalents. Given the political unrest over the cost of living across the Western world, it is possible that public opinion will turn against these protectionist policies.

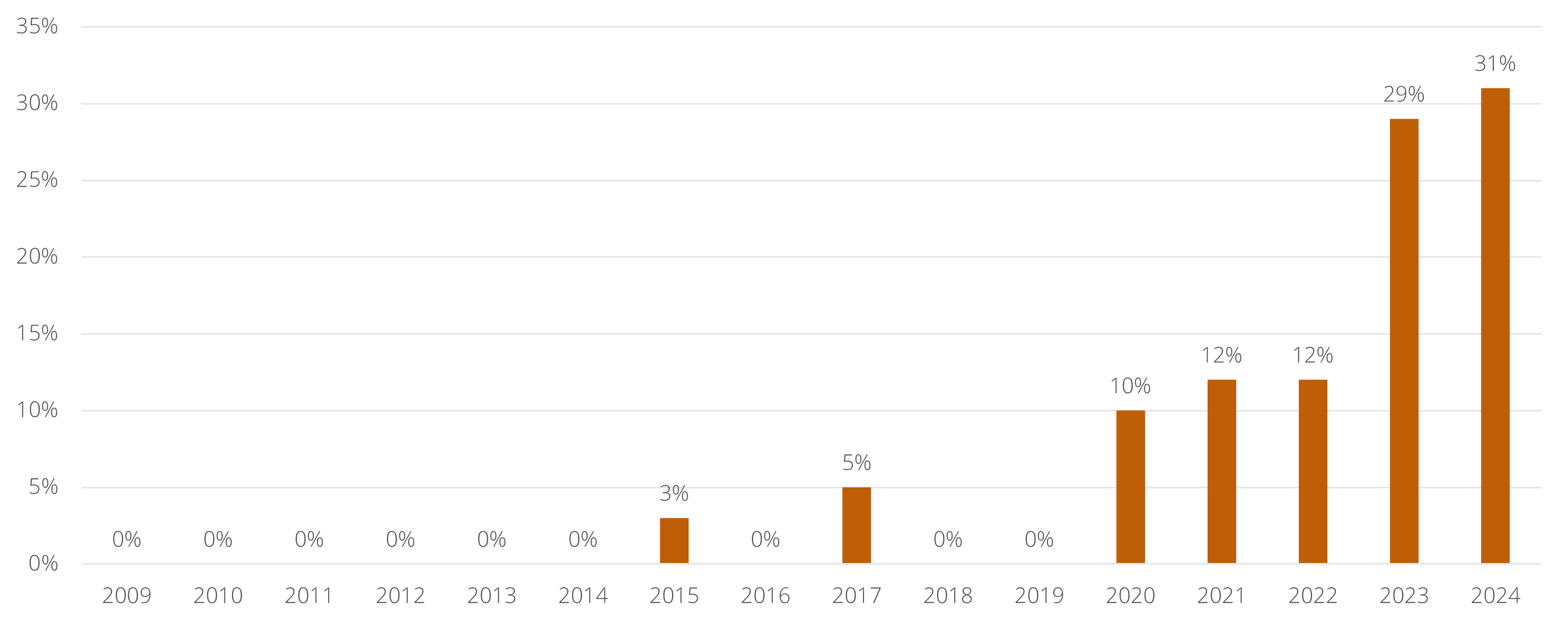

The Western image of China as merely the world’s factory for cheap goods has been dismantled step by step, but the final realization has yet to sink in. In 2020 the pandemic exposed China’s dominance in pharmaceutical ingredients, and in 2025 the West has discovered its control over rare earth metals. In the meantime, China became a global leader in producing high-end batteries and electric vehicles. Still, one shift remains underestimated: China’s ability to push the frontier of innovation. A clear example is biotechnology, where China has emerged as a world leader in developing new medicines — capturing 31% of the global market after starting from zero just a few years ago.

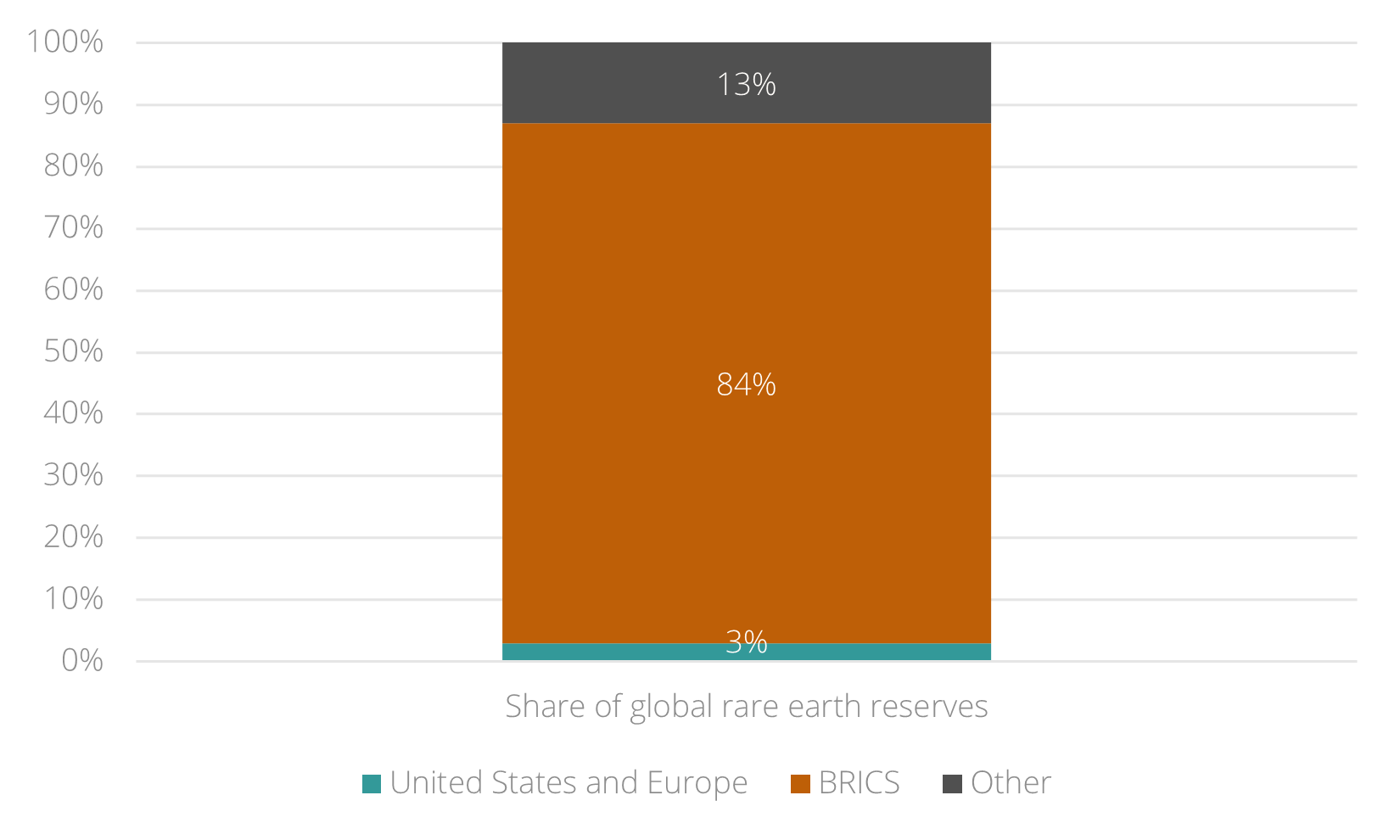

China’s export controls on rare earth metals are part of a broader strategy. Since 2024 the BRICS-countries (Brazil, Russia, India, China and South-Africa) have reportedly been working toward the launch of a new metals trading platform - covering everything from gold and silver to rare earths - that will operate independently of Western exchanges in Chicago and London, as well as Western payment systems like SWIFT. Together, the BRICS control roughly 84% of the world’s rare earth reserves. Much like the Arab OPEC countries during the 1973 oil crisis, the BRICS could use their dominance in critical resources to exert pressure on the United States and Europe.